I’ve run various posts over the last few years urging the authorities (Reserve Bank, Treasury, and the Minister of Finance) to get better prepared for the next serious recession (and lamenting the relative inaction on this front in other countries too, many of whom are worse-positioned than New Zealand is).

As a reminder, we went into the last recession with the OCR at 8.25 per cent, while the OCR now – years into a growth phase, with resources (on official assessments) fairly full-employed – is 1.75 per cent. In that last recession, the Reserve Bank cut interest rates a long way, the exchange rate fell a long way, there was really large fiscal stimulus cutting in as the recession deepened, and there were lots of other interventions (guarantee scheme, special liquidity provisions) and it was still as severe as any New Zealand recession for decades, and took years to fully recover from (on official output and unemployment gap estimates perhaps seven or eight years). Lives were blighted, in some cases permanently, in an event where there were no material constraints on the freedom of action of the New Zealand authorities. In fact, our Reserve Bank cut the OCR (over 2008/09) by more than any other advanced country central bank.

Next time, whenever it is, it seems very unlikely that the Reserve Bank will have that degree of freedom, particularly around monetary policy. On current policies and practices around bank notes, it seems unlikely that the OCR could be usefully cut below about -0.75 per cent. Beyond that point, most of the action would be in the form of people shifting from bank deposits etc to physical currency, rather than buffering the economic downturn.

Our Reserve Bank has long appeared disconcertingly complacent about this issue/risk. The latest example was comments by the new Governor and his longserving chief economist following the latest Monetary Policy Statement. They talk blithely about the unconventional policy options other countries have used, but never confront the fact that almost no advanced country could have been comfortable with the speed of the bounceback from the last recession. Output and unemployment gaps of eight or nine years (the OECD’s estimate for advanced countries as a whole) aren’t normal and shouldn’t be acceptable.

Quite why the Reserve Bank is so complacent is something one can debate. My hypothesis is that it is some mix of assuming we will never face the problem (recall that they have spent years hankering to get the OCR back up again) and of noting that other people/countries will most likely face the problem before New Zealand does. They also like to remind us that New Zealand has a floating exchange rate as if this somehow differentiates us (as a reminder so do Australia, Canada, Norway, Sweden, the US, the UK, Japan, Korea, Israel, and even the euro-area as a whole). Whatever the explanation, robust contingency planning, and building resilience into the system, is what we should be expecting from the Reserve Bank (and Treasury). There is no sign of it happening. Meanwhile, the Governor plays politics in areas (eg here and here) that really aren’t his responsibility.

In my post on Saturday, I touched again on the desirability of doing something – specific and early, consulted on and well-signalled – about removing the effective lower bound on nominal interest rates. That would tackle the issue at source. Monetary policy has been the primary stabilisation tool for decades for good reasons. Among other things, it is well-understood and there is a fair degree of (political and economic) consensus around the use of the tool. And confidence that the tool is at hand in turn proves (somewhat) self-stabilising, because people expect – and typically get – a strong monetary policy response.

Perhaps the other reason why authorities – perhaps especially in New Zealand – have been so complacent is the view that “never mind, if monetary policy is hamstrung there is always fiscal policy”. After all, by international standards, public debt here is low (on an internationally comparable measure from the OECD, general government net financial liabilities, about 1 per cent of GDP, which puts us in the lower quartile – less indebted – among OECD countries.)

The implicit view appears to be that, with such modest levels of debt, if and when there is another serious recession, New Zealand governments can simply spend (or cut taxes) “whatever it takes” to get economic activity back on course again. After all, the upper quartile of OECD countries have net general government liabilities in excess of 80 per cent of GDP.

I’m sceptical for a variety of reasons.

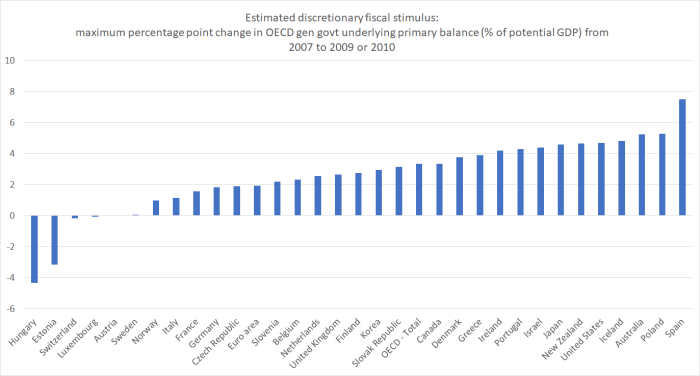

One of them is the experience of the last recession. For this, I had a look at the OECD data on the underlying general government primary balance as a per cent of potential GDP:

- general government = all levels of government

- underlying = cyclically-adjusted (ie removing the impact of the fluctuating business cycle on revenue (mostly), and adjusted for identified one-offs (eg recapitalisations of banking systems)

- primary balance = excluding financing costs, so that comparisons aren’t affected by changes in interest rates themselves

- as a per cent of potential GDP = so that a temporary collapse in actual GDP doesn’t muddy the comparison

The numbers aren’t perfect, and there are inevitable approximations, but they are the best cross-country data we have. Changes in this balance measure are a reasonable measure of discretionary fiscal policy.

Here is how those underlying primary balances changed from 2007 (just prior to the recession) over the following two or three years. I’ve taken the largest change I could find, and in every case that was over either two years to 2009, or over three years to 2010.

Some countries (Hungary, Estonia) were engaged in severe fiscal consolidation from the start. Several others experienced almost no change in their structural fiscal balances.

Quite a few countries saw 5 percentage point shifts in their underlying fiscal balances. Spain – a country with no control over its domestic interest rates – is recorded as having gone well beyond that. I don’t know much about the specifics of Spain, but for those who are upbeat about the potential scope of discretionary fiscal policy I’d take it with at least a pinch of salt – on the OECD numbers, the Spanish primary deficit dropped again quite sharply the next year (and Spanish unemployment didn’t peak until several years later).

Note that both Australia and New Zealand are towards the right-hand end of that chart. In Australia’s case, most of the movement resulted from deliberate counter-cyclical use of fiscal policy (the Kevin Rudd stimulus plans). In New Zealand, by contrast, the change in the underlying fiscal position was almost entirely the result of discretionary fiscal commitments made by Labour government at a time when Treasury official forecasts did not envisage a recession at all. From a narrow counter-cyclical perspective, those measure might have been fortuitous, but they were not deliberate discretionary counter-cyclical fiscal policy measures. In fact, at the time they were seen in some quarters as exacerbating pressure on the exchange rate, and limiting the scope of any interest rate reductions.

Perhaps it is worth stressing again that in not one of the OECD countries did the reduction in structural fiscal surpluses (expansion in deficits) last more than two years. In every single country, by 2011 structural fiscal policy (on this measure) had moved – sometimes modestly, sometimes quite sharply – into consolidation phase. In most countries, either conventional monetary policy limits had been reached or (as in individual euro area countries) there was no scope for conventional monetary policy. And it was to be years before output and unemployment gaps closed in most of these countries.

What is my point? Simply, that it looks as though the political limits of discretionary fiscal stimulus were reached quite quickly, even in countries where there was no market pressure (any of the established floating exchange rate countries other than Iceland), and even though the economic rebound in most was anaemic at best. That is why so many countries needed more conventional monetary capacity than in fact they had (and QE in various forms was not much of a substitute).

The OECD table on underlying primary balances only has data going back a few decades. No doubt experiences in wartime were rather different – in those circumstances huge shares of the nation’s resources can be marshalled and deployed in ways which (incidentially) stimuluate demand and activity. But looking across the OECD countries over several decades, I couldn’t any examples of discretionary fiscal policy being used as a counter-cyclical tool materially more aggressively than happened over 2008 to 2010. In Japan, for example, the structural fiscal balance worsened by about 6 percentage points over seven years after 1989.

So from revealed behaviour patterns, I’m sceptical as to just how much practical capacity there is for fiscal policy to do much, and for long, in the next serious recession, even in modestly-indebted New Zealand. The limits aren’t technical – they mostly weren’t last time – but political. Perhaps people will push back and run some argument along the lines of “oh, but we’ve learnt the lessons of unnecessary premature austerity last time round”. To which my response would be along the lines of “show me some evidence, or reason to believe that things would, or even should, be much different next time”. When – outside wartime – has it ever happened? And what about our political systems makes you comfortable that it is likely to happen next time? We could probably run large structural deficits for a year or two, but pretty quickly the pressure is likely to mount to begin reining things back in again (especially if, for example, the next recession is accompanied by heavy mark-to-market losses on government investments – eg NZSF).

And recall that here in New Zealand we had almost as much fiscal stimulus last time as any country, and even supported by huge cuts in interest rates (and without a home-grown financial crisis), we had a nasty recession (even a double-dip in 2010) from which it took ages to recover.

And all of this is without even examining how effective realistic fiscal policy is likely to be. The easiest fiscal stimulus is a tax cut (or even a lump sum cash handout). You can do clever ones, like the UK temporary cut in GST, which not only put more money in people’s pockets, but actively encouraged them to shift consumption forward – only to then create problems as the deadline for raising the value-added tax rate loomed. But putting money in people’s pocket – in a recession, and often explicitly temporarily – doesn’t guarantee they spend much of it. The most effective demand-stimulating fiscal policy (supply side measures are another issue – but lets just agree that deep cuts in company tax and related rates will not happen in the depths of a recession) is direct government purchases of goods and services. Most talked of is government capital expenditure, infrastructure and all that.

But, approve or otherwise, no government has a reserve list of projects, designed and consented, just waiting to get starting the moment it is apparent the next deep recession in upon us (that moment usually being several months after the recession has begun). It is almost certainly politically untenable for them to do so – if the project is so good, so the argument will run, why not do it when times are good? And so realistic government fiscal stimulus through the capital expenditure side will take months and years (more probably the latter) to even begin to get underway. Faced with the actual physical destruction in Christchurch, look how long it took for major reconstruction to get underway.

What of income tax cuts? Either the cuts are focused on those who pay the most taxes (in which case there is quickly one form of political pushback) or perhaps they take the form of a tax credit paid as a lump sum to everyone (in which case there is likely to be pushback of another political type – ideas around “everyone becoming a welfare beneficiary). I’m not attempting to defend either type of response, just to anticipate the risks.

By contrast, monetary policy – the OCR – can be adjusted almost immediately, and often begins to have an effect before the central bank even announces its formal decision (market expectations and all that). And if monetary policy changes don’t affect everyone equally, they affect the entire country – a borrower/saver/exporter in Invercargill just as their counterparts in Auckland. In the line from a US Fed governor, monetary policy gets in “all the cracks” (although he was contrasting it with regulatory interventions). Government capital expenditure is, by its nature, very specific in location. There probably isn’t a natural backlog of major (useful) capital projects in Invercargill or Dunedin.

I’m not saying fiscal policy has no useful place in the stabilisation toolkit – although my prior is that it is better-oriented towards the medium-term, with the automatic stabilisers allowed to work fully – but that we should be very cautious about expecting that it is any sort of adequate substitute for monetary policy in the real world of politics, distrust of governments and so on, in which we actually dwell. It is well past time for the Reserve Bank and the Treasury, led by the Minister of Finance, to be taking open steps towards ensuring that New Zealand has the conventional monetary policy capacity it would need in any new serious recession.

“” no government has a reserve list of projects, designed and consented, just waiting to get starting “”. Why not?

Just one example: NZ should have several towns just waiting for instant building. It would cater for drastic government expenditure during an serious recession but also for housing population displaced by tsunami or volcano or influx of inhabitants from Pacific Islands suddenly uninhabitable after climate warming event. ‘Just waiting’ means land reserved, access roads prepared, raw materials accessible (quarries and wharves prepared), kitset houses & tents stockpiled for the first builders, all building consents prepared, etc. For the cost of just a few million in planning a major project could be started within minutes and be well underway within weeks.

LikeLike

Why not? Well, to take your specific example:

In recessions house prices tend to fall (as they did in 08/09) and population growth also often slows (fewer NZers go to Aus, but fewer foreigners – esp on short-term visas – come here), The pushback against the govt starting a big housebuilding project as house prices are falling would be considerable. And, on the other hand, if the project was just sitting shovel-ready in the boom years, as house prices doubled, irresistible pressure would come on to just get on and do it.

You could multiple examples? How about a four-lane highway from Akld to Wgtn? It could all be consented etc and how would the pressure to proceed in an extended boom be resisted (after all that is when traffic volumes will be rising strongly) and on the other hand, the pressure of “why we are we doing this boondoggle when the economy is down the drain, traffic volumes are dropping etc?”

I’m not defending any of those reactions, just anticipating them.

More generally, govt capital spending decisions are typically of rather poor quality. Better to remove the lower bounds on interest rates to allow the private sector (bearing the risk) to make the choices about the next projects to proceed. Bridges to nowhere really do make us poorer in the long-term, even if building them sucks up resources in a recession.

LikeLike

….you think the public won’t back an acceleration of the ‘Kiwibuild’ pipeline if there are idle resources? (post: OCR cut, forward guidance, liquidity/funding support, negative OCR, some sort of QE…all of which fail to get people spending)

LikeLike

not if their house prices are falling materially

of course, if a recession were to happen in the next year, Kiwibuild might (to the extent it wasn’t just displacing private building) play a stabilising role, as a programme already getting underway, but that is different than the specific question you posed.

Recall that one of the global risks next cycle is a drift into deflation. In that climate debt to GDP ratios can start climbing, potentially alarmingly, really quite quickly.

Publics prove to have endured an awful lot of output loss/unemployment without embracing with enthusiasm big rises in public debt.

(The other point I didn’t touch on in the post at all is the likelihood of private sector offsets. No one knows how strong those effects would be, but they would surely become more powerful the more aggressively politicians look to use fiscal policy.

My bottom line: fiscal policy isn’t necessarily terrible, but it is in practice highly constrained, inevitably quite specifically distributional, and we could (and should) just get on and fix mon pol, as a first best option.)

LikeLike

The last NZ recession had nothing to do with the GFC. It was engineered by the RBNZ and house prices fell because people did not have jobs and left for greener pastures overseas. Australia economy was still bouyant when the RBNZ decimated the NZ economy on purpose.

LikeLike

The current slowdown has also been engineered by the RBNZ when Wheeler pushed up the equity to LVR to 40% and the subsequent loosening to 35% was accompanied at the same time as a 15% tightening directly with the local banks via their banking licencing covenants.

Of course assisted by a Labour governments Ban Foreign Buyers rhetoric and upcoming legislation. But the primary slowdown is the RBNZ engineered lack of credit liquidity in the marketplace.

LikeLike

Explain how that works and what you mean

How did the RBNZ engineer the recession?

NZ was officially in recession in September 2008

RBNZ cut OCR as follows

July 2008 -25 bps

Sept 2008 -50 bps

Oct. 2008 -100 bps

Dec. 2008 -150 bps

LikeLike

The OCR hit a peak at 8.25% from 26 July 2007 till 5 June 2008. Real floating interest rates were above 10% and for development finance it was around 15%. The OCR started its upward track from as early as Jan 2004 from around 5.25% only 2 years into the green shoots of a bull market from 2002. The RBNZ was quick and rather trigger happy to try and stamp out any bouyant economy partying.

When the recession started officially in 2008 businesses have already burned their equity reserves and profitablility was in decline in the 2 years leading up to 2008.

The problem with interest rate intervention is that it does not affect the average NZ household in total as savers start spending the higher income they receive from higher interest rates. NZ households have savings that almost equal household debt which means that higher interest rates have to reach a high enough point to actually damage savers employment and jobs decimated before higher OCR can dampen consumer and spending inflation.

LikeLike

I am in agreement with Simon Wren-Lewis on the use of fiscal policy when needed i.e a liquidity trap which occurred during the GFC on a number of levels.

I agree with Bob. Every government should have shovel ready infrastructure projects ready to go if needed.

Tax cuts means a permanent increase in the structural deficit. spending on Infrastructure means a temporary increase.

LikeLike

I’m not disagreeing with you (or Wren-Lewis )that (for example) in those circumstances fiscal multipliers would be larger than in normal times. My argument is that for political economy reasons, among others, the fiscal policy option is not a good, let alone ideal, substitute for fixing the lower bound problem at source (it is, after all, wholly a regulatory constraint). And when Wren-Lewis criticises the Cameron/Osborne austerity, I don’t even necessarily disagree with him prescriptively, but descriptively he has to deal with revealed real world political behavioural constraints.

LikeLike

Hi Michael

When I was in Treasury a few years ago I wrote a short note advocating Bob’s idea: that the government be prepared to hire private sector builders to build houses in Auckland if NZ goes into a recession. In addition to the counter cyclical nature of this type of government spending,

(i) building permits are a leading indicating of construction activity and are particularly well measured, making it relatively straightforward to act in a timely fashion

(ii) a feature of NZ’s stop-go approach to construction over the last four decades is that construction workers migrate to Australia when we have recessions, and it is rather difficult to get them back in time for the next upturn, leading to a shortage of experienced construction workers in NZ (and who can blame them; higher wages, better weather and colder beer, even if the grass isn’t greener over there as they don’t have so much rain);

(iii) there appears to be a shortage of housing in Auckland, at least in comparison with the construction that has being taking place in the rest of the country.

All that is needed is the government being prepared to take ownership of said houses during the downturn, with a view to selling them in a subsequent upturn; in essence it needs to work out the criteria, in advance, of when it would be prepared to act, and be prepared to store houses, possibly at a loss, until they are wanted.

The building-migration cycle has been a central feature of NZ’s economic landscape since 1968 – migration and building downturns in 1968,1978,1988,1998, 2008, and possibly 2019. In most of these cases there has been large inward migration in the middle years of the decade, followed by less inward migration in the latter years (and a reverse outflow of some of the immigrants, those with visa restrictions or those who found out that the milk and honey was being at above world prices) inward , plus a backlog-outflow of NZers to the less-green but otherwise better pastures offshore.

The bonus is less unemployment, although this is more of a bonus for men and may not count for so much.

Part of the issue with construction downturns could be a lack of supply finance on the part of developers, not just a lack of demand by prospective owners. Liquidity can dry up in a recession. Relative to the private sector, the government is scarcely ever affected by liquidity crises, as the Nobel prize-winning economists Holmstrom and Tirole have reminded us for the 20 years. One one of the key insights of Keynes was that governments have the liquidity to borrow and pick up the slack when illiquid businesses reduce their demand.

Andrew

LikeLiked by 1 person

Thanks. Sounds like an option for a left-wing government.

One downside, if envisaged as a material part of an overall stabilisation policy, is that it would generate direct activity in places like Akld, but not in much of the rest of the country.

LikeLike

Better a left wing government than a extreme right wing RB governor. As an accountant on the ground dealing with the human face of real overdraft interest rates floating above 10% which most businesses rely on especially in the building and construction industry it was a like watching a horror movie of business after business falling into bankruptcy and homes in mortgagee sales and the associated toll in broken families and lost futures.

LikeLike

“All that is needed is the government being prepared to take ownership”

That is comparable to Bernanke’s TARP – was Bernanke considered a left-wing agent?

LikeLike

Having the government act as a countercyclical demand sink for housing seems like a perfectly sensible idea. But how to interpret the current rash of bankruptcies in a housing shortage environment? It seems to be many of these companies are inadequately capitalised. If they have strong order books, they can go and raise capital on the public market if they need to.

LikeLike

It looks quite good on paper. But the politics is another matter (after all, in an Aus context look at the alarmist/optimist commentators suggesting that the current house price adjustment is a foretaste of a major crash). To repeat, I’m not saying it couldn’t play a part, but I wouldn’t want to count on it, especially as mon pol could be fixed at source.

As for the bankruptcies, bad (overly aggressive) tendering, rising construction costs, ruinous land prices, and an existing house price market that – in least in Akld – has gone sideways, perhaps eliminating margins developers/builders might have expected?

LikeLike

….a drift into deflation? think the pre GFC/GFC showed that a government with its own currency/central bank will do what is required to ensure ‘it’ doesn’t happen; what’s the alternative? Greece provides an idea I guess and the alternative of extensive debt restructuring / clean up is less appealing than more public debt across the tax base…

LikeLiked by 1 person

To my mind the main reason why there is political pressure on governments to limit deficits is that appropriate, functional deficit spending and traditional Keynesian responses have been demonised by the mainstream economics profession for decades. Millions have been spent by various right-wing “foundations” educating people about the danger of the “national debt burden” and the need for austerity otherwise doom will ensue.

Scaremongering about public debt levels has been the constant refrain – Reinhart and Rogoff, Alessina etc. Despite the fact that there appears to be no particular public debt/gdp level that spells doom in a sovereign currency issuing state with a floating exchange rate. Japan anyone? Japanese government going to default? Massive inflation in Japan? Gonna bet against JGBs? Didn’t think so. All I see there is a decent welfare state with amazing public services.

My question about negative OCR is if I am charged negative rates on my savings do you think I am going to spend, or save even more because my money is reducin? I’ve lost my job, my savings are being depleted anyway and now I am facing negative interest rates reducing my money even more. So I’m going rush out and refurbish my kitchen? I don’t think so.

LikeLike

“Nurses in Japan caring for patients with dementia in acute care settings often lack specialized education in geriatric nursing.The problematic situations described sometimes led to abuse and neglect of these patients.” https://www.ncbi.nlm.nih.gov/pubmed/11985753/

Japan is at the forefront of a dementia crisis that experts warn will affect other societies with burgeoning elderly populations in decades to come. According to the health ministry, 4.6 million people are suffering from some form of dementia, with the total expected to soar to about 7.3 million people

The type of abuse of dementia patients in Japan involve tying them up immobile on their beds with sedative drugs liberally administered. Roughly 10,000 dementia patients go missing in Japan every year and hundreds turn up dead, or not at all. Those who stroll into the path of a speeding train can suffer a posthumous indignity: a bill for the cost of the accident.

As a result of a severely limited immigration policy, Japan is now suffering from a lack of low-skilled workers, especially within its health services. Employers are also struggling to fill jobs in convenience stores and fast-food chains. https://www.newsweek.com/japan-ageing-dementia-caregivers-shortage-621431

LikeLike

Just on your final point, the logic is the same for a reduction in positive interest rates. There is a negative income effect for savers when rates are cut, but a positive one for borrowers. Conventional monetary policy rests on the assumption that the net of those two income effects is smaller than the substitution effects (shifting consumption and investment forward in response to the lower cost of borrowing/return on savings).

But the idea of a negative return on deposits is one of the political obstacles to seriously negative interest rates. It is one reason why the issue should be more broadly socialised now by those in authority, to help appreciate the choices/tradeoffs.

LikeLike

NZ household savings($172billion) almost equal NZ household Housing debt($179billion) in total. Also there are numerically more savers than there are borrowers therefore again conventional wisdom poorly guided by NZ economists lead to the wrong conventional wisdom. There is therefore almost Zero impact in interest rate rises or interest rate falls on consumer spending or consumer inflation. Where it does make a difference is in business borrowers ie employers, because there is around $250 billion in business borrowings that is not matched by the equivalent savings. Conventional monetary policy damages business lending overall and as a result damages jobs. Once job losses start as a result of rising interest rates thats when savers consumer spending would be affected.

LikeLike

Finally, why do fiscal stimulus projects always need to be “shovel-ready”? Implying that they will provide big, masculine infrastructure spends for construction workers and steady profits for Fletchers. Ribbons for politicians to cut and hard-hat flouro vest photo ops. What about increasing public services that will employ the women who will lose their jobs in a recession? God knows our kids need more teachers and teacher aids. Our elderly and youth require more social workers and care support. Our obese kids on the way to metabolic disease need serious lifestyle interventions to avoid a healthcare blow out in the future. Our poor communities need more access to the arts and subsidized sport and leisure activities. Is it really better to build a bigger hospital? Or would it be better to train and employ more community care nurses working on prevention? The investment in services might deliver far better outcomes in terms of a healthy, well-educated more stable community than a new motorway.

LikeLike

My use of the cliched expression “shovel ready” was in the context of a discussion around infrastructure/housebuilding. But in a “ready to go quickly” sense it could, as you note, apply more broadly.

Note though that there are material lead times on some of the options you mention – eg people with those particular skills, who typically won’t have been the people losing jobs in a downturn (actually, construction is one of the most cyclical sectors globally).

Recall that my original main point wasn’t about the type of goods and services govts could purchase, as that I expect the political resistance to large sustained fiscal stimulus to quickly prove quite binding. Some of that might be the influence, for good or ill, of economists, but it won’t be all of it by any means (as it wasn’t in 2010/11).

LikeLike

Sanders and other Democrats are supporting the MMT proposal for a universal job guarantee at a minimum wage. This could be the automatic stabiliser par excellence and should be planned for now in my opinion. The long term negative effects of being on the Dole are clear. Much better to get people working on socially and environmentally useful projects that languishing in despair on the pittance of a dole developing long term disabilities. Employed buffer stock to discipline inflation rather than unemployed buffer stock. That should be the ‘shovel ready’ project. I know my husband and I would much rather work for a minimum wage on community projects in a recession than be unemployed. When things pick up, move back to private sector.

LikeLike

[All items | LSE Public lectures and events | Audio] Crashed: how a decade of financial crises changed the world [Audio]

http://podplayer.net/?id=54675780 is apposite.

LikeLike

Thanks

I’ve almost finished reading the book and will aim to write about it at some point soon.

LikeLike

It’s interesting what, in that admittedly reduced format of a lecture, the author chooses to hammer home. In this case, he repeatedly stresses that there is no reason to think that the next recession should be of the same order of magnitude of severity as the 2008 incident, which could have been (perhaps) once-in-three-generations except for the radical response. Instead we should expect a more standard cyclical downturn. Of course, it doesn’t follow that wise people wouldn’t have well-planned and well-understood monetary measures equivalent to a 6% cash rate cut in their locked drawer. And of course, with some asset prices at high water marks, there is a long way to fall.

LikeLike

And on this issue, I’ve always stressed that – particularly for NZ – the issue is the next serious recession (not some mild downturn with a slight fall in GDP over a couple of quarters). In much of the world the issue is more serious: the average cut in the Fed Funds rate, across recessions large and small, has been about 500 basis points. In almost all of Europe there is barely any capacity to cut interest rates at all.

LikeLike