But first a correction. As I noted on Twitter and very briefly on the post itself on Saturday, it seems that the gist of my post on Friday was wrong. The repeal of Labour’s tobacco de-nicotinisation legislation – whatever motivated the parties that championed the change – will leave the flow of tobacco excise revenue largely as it was, providing the government an extra flow of revenue – relative to what was allowed for in PREFU – that will, if anything, more than compensate for what National had told us they expected the foreign buyers’ tax would have raised. With the various other bits in the various coalition agreements they are probably back to being in roughly the – very demanding – fiscal situation National thought it would be facing before the election: large deficits, very demanding indicative operating allowances, and an aversion to cutting programmes/”entitlements”,

As for the impact of fiscal policy on aggregate demand, and thus the pressure on monetary policy, they’ve ended up – without really consciously trying, or so it seems, with a somewhat helpful policy switch; dumping the foreign buyers’ tax which was supposed to raise money from wealthy foreigners who mostly would not have been earning or otherwise spending that money in New Zealand (which revenue therefore would not have dampened demand) and replacing it with the reinstatement of the tobacco tax revenue scheme, mostly raising money from relatively low income New Zealanders who will, on average, have a very high marginal propensity to consume in New Zealand. Whatever the substantive merits (or otherwise) of either policy, all else equal the switch is slightly helpful for monetary policy.

A few days after the election I wrote a post “What should be done about the Reserve Bank?” itself if (as I put it in that post) a new government is at all serious about a much better, and better governed and run, institution in future. Perhaps unsurprisingly I stand by all the points in that post, around both individuals (Orr, Quigley, external MPC members, and so on) and the institution.

That post ended this way

That final paragraph was about the fact that unless he leaves more or less voluntarily it would be hard to get rid of Orr (judicial review risks etc and attendant market uncertainty) and yet it would be highly beneficial were he to be replaced well before March 2028.

Anyway, with the release on Friday of the two coalition agreements we know a little more re the options for the monetary policy functions of the Bank.

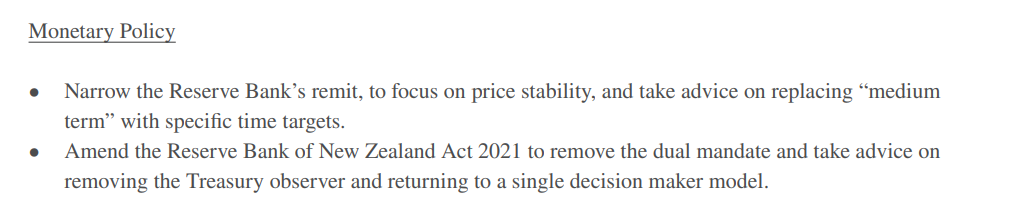

At a high level, both agreements commit the parties to make decisions that are “focused” to “drive meaningful improvements in core areas including

One might have briefly hoped that this might have resulted in the government lowering the inflation target to something actually consistent with price stability – eg, allowing for index biases, 0 to 2 per cent annual inflation – but it probably only means the abolition of the so-called dual mandate (something both National and ACT had campaigned). The specific material on monetary policy is from the ACT agreement

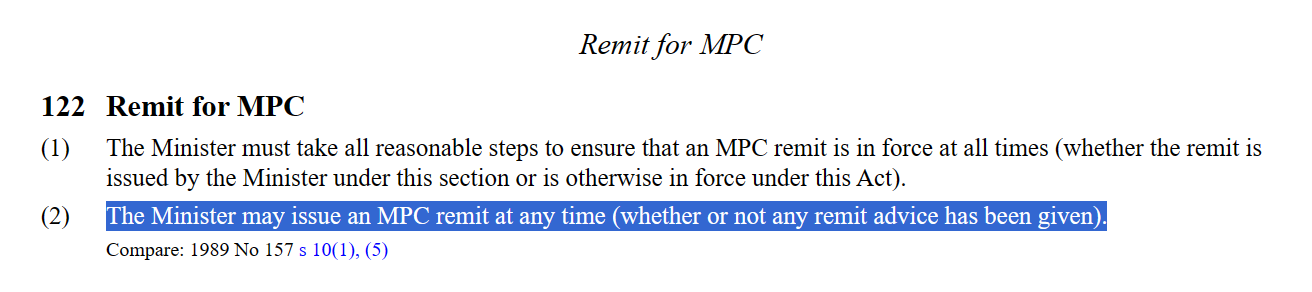

In National’s own 100 day plan the legislation to amend the statutory goal of monetary policy was to have been introduced – not passed – within the first 100 days, but in the coalition agreement there is no indication of the legislative priority. However, the Act makes it clear that the Minister of Finance could issue a new Remit – the actual targets the MPC is supposed to work to – at any time

It would be a simple matter of deleting one short paragraph from the Remit, which would then also have the appeal (to the government) of being clear that the MPC was working to this government’s Remit not the last government’s one. That doesn’t need to await the other advice, it could be done today or tomorrow (perhaps after the first Cabinet of the new government), and before the MPS on Wednesday. If the Minister moved that fast it would no doubt prompt specific questions at the MPS press conference, but…..they are going to be asked anyway. (UPDATE: The Minister is required to consult (but not necessarily have regard to the views of) the MPC before issuing a new Remit, so the next day or two probably isn’t an option, but it need not be an elongated process when the government has a clear electoral mandate for change.)

(To be clear, I am not a big fan of this change. I largely supported the 2018 legislative change. But……from the then-government’s perspective the change then was mostly about political product differentiation (essentially cosmetic) and so will the reversal be. Few serious observers think either change has made, or will make, any material difference to monetary policy decisions (and the Governor has repeatedly stated that it has not done so to now), but the change is – I guess – a way of signalling that the government recognises the public’s visceral distaste of high inflation and that it expects the Reserve Bank MPC to do so too (for the last two years there has been no sign of that).)

What about those other points on which advice is to be sought (presumably things ACT championed that National refused to agree to upfront, and may be disinclined to support at all)?

There are three of them:

- replacing the “over the medium-term” time horizon for meeting the inflation target with some specific time targets (eg “over a rolling 18-24 month horizon” or somesuch),

- removing the Secretary to the Treasury as an non-voting member of the MPC, and

- returning to a single decisionmaker model for model (given the heading and context, presumably only for monetary policy, but perhaps more broadly).

I would not favour any of those changes.

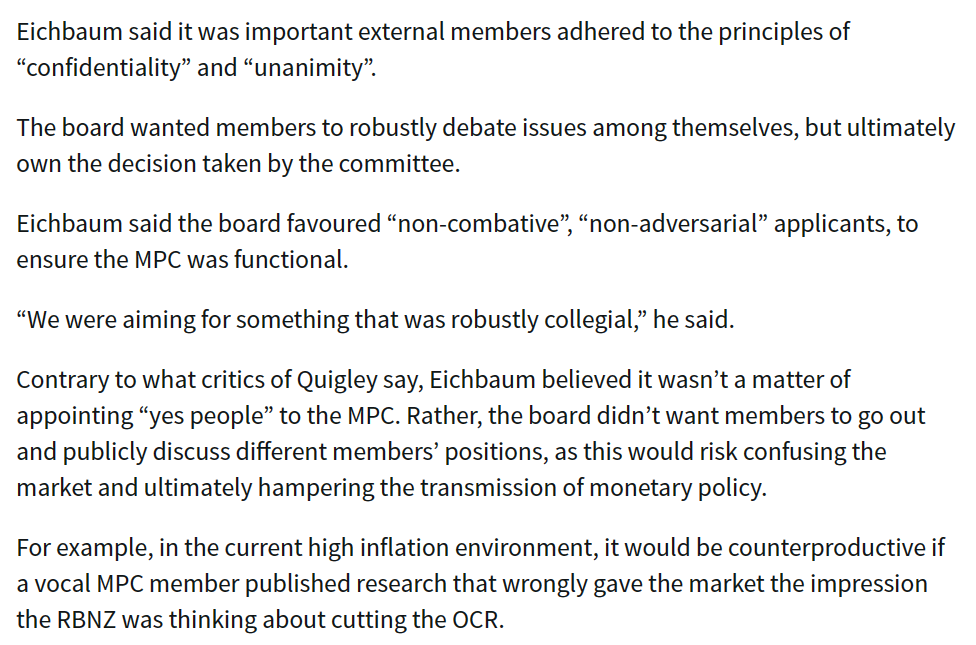

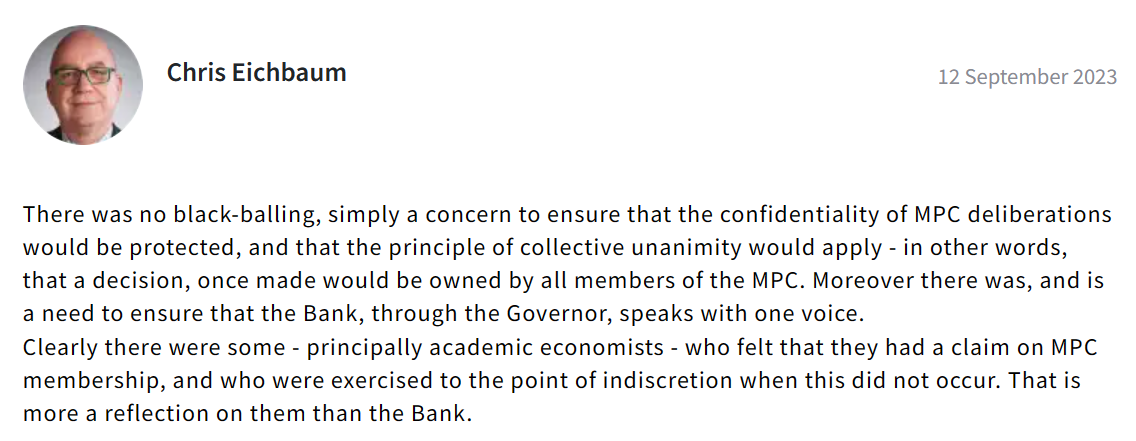

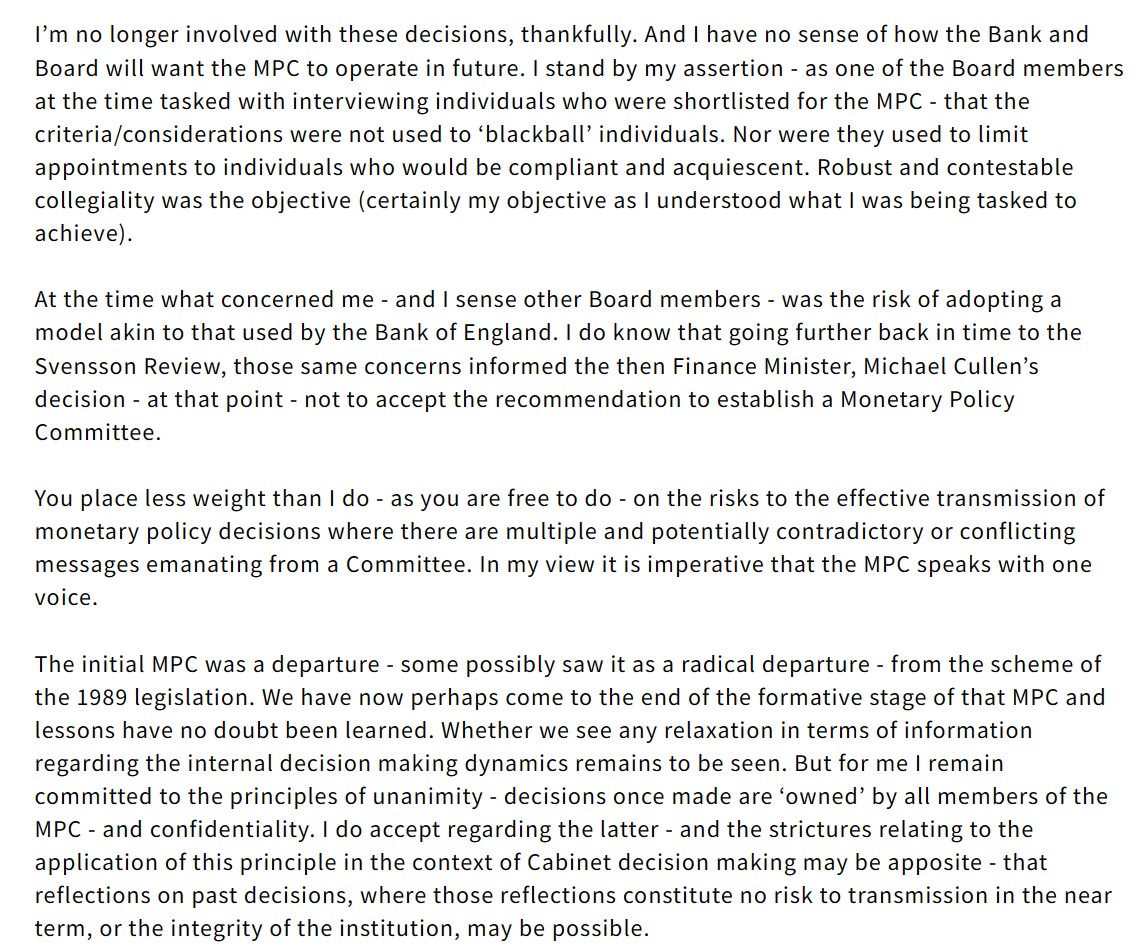

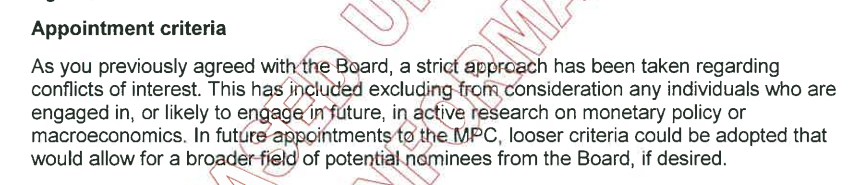

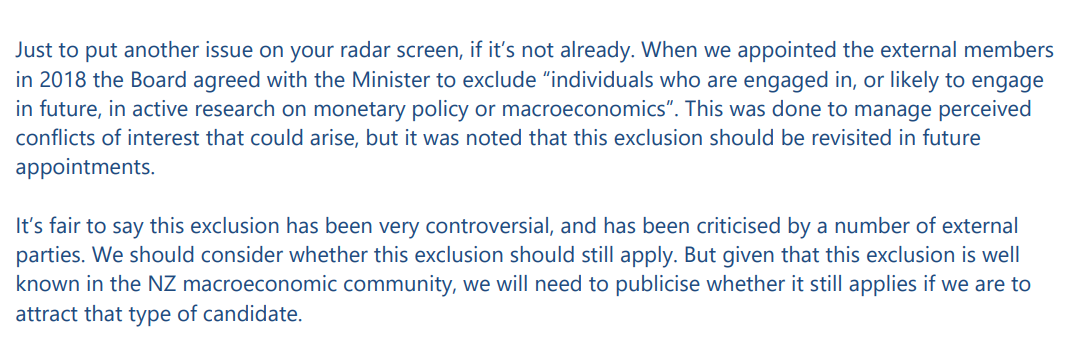

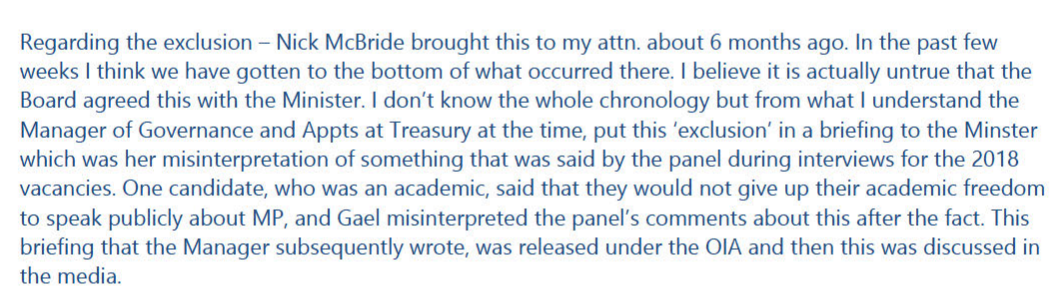

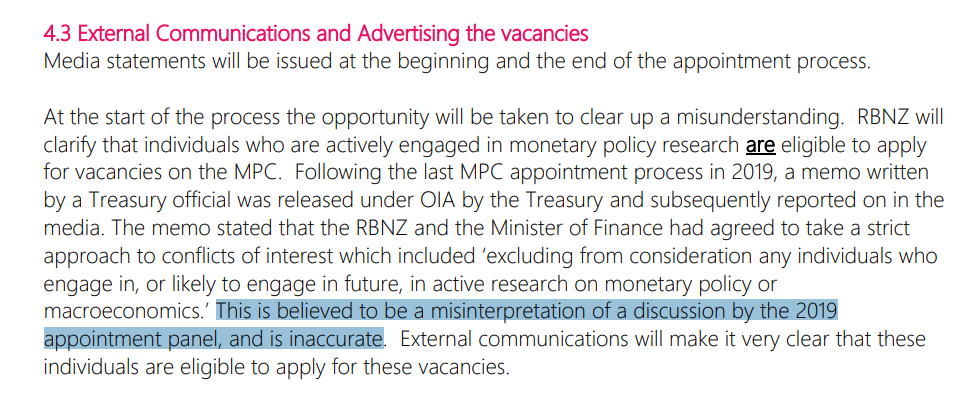

The most marginal call – which wouldn’t excite me if it went the other way – is the position of the Secretary to the Treasury. I favoured the non-voting member provision in 2018 (it is a not-uncommon arrangement in other countries, and in Australia the Secretary to the Treasury is still a voting member), but there is no evidence from the four years of the MPC’s existence that the Secretary to the Treasury (or her alternate) has added any value (most often one of her deputies attends), whether around substance or process. The evidence we have also suggests a risk that the Bank and the Treasury are too close to each other, undermining the likelihood that the Treasury does its job – as the Minister’s adviser monitoring and holding to account the Bank – at all rigorously or well. How likely was it, for example, that there would be any serious accountability around the LSAP losses when the Secretary to the Treasury sat through all the meetings and there is no record of any ex ante concern being expressed? We also now know – from a recent OIA – that Treasury did nothing at all about the way they were lied to by the Reserve Bank Board chair as regards the earlier blackball on experts serving as external MPC members.

(More generally, if the new government is serious about a much better public sector they should be looking to replace the Secretary when her term expires next year, but this post is about the RB not the Treasury per se.)

I would not favour specific time targets for monetary policy. These were used in the early days of inflation targeting (when the first target was 0 to 2 per cent inflation by 1992), but once the target was achieved things reverted (sensibly in my view) to a model in which it was expected that inflation should (a) be kept within the target range, and (b) if there were deviations (headline or core), the Bank was expected to explain the deviation and explain how quickly it expected to get inflation back to target (either inside the band, or the target midpoint the MPC has been required to focus on since 2012).

It would not be advisable to put ex ante specific imposed timeframes on the MPC, mostly because shocks and deviations from target will differ. They may include, on the one hand, essentially mechanical things like GST changes (or other indirect tax or subsidy changes) which will appear in annual CPI inflation and, all else equal, automatically drop out 12 months later. But they will also include things like big – and perhaps sustained – supply shocks. You could think of a sequence of years in which – unexpectedly – the price of oil kept moving sharply higher (this happened in the 00s). A surge in petrol prices might take inflation above target. It is fine to require the MPC to bring inflation back 12 or 18 months hence, but if there is another surge six months on, you’ll end up with another overlapping target (the first having been deemed essentially redundant). And nine months later there might be a third surge.

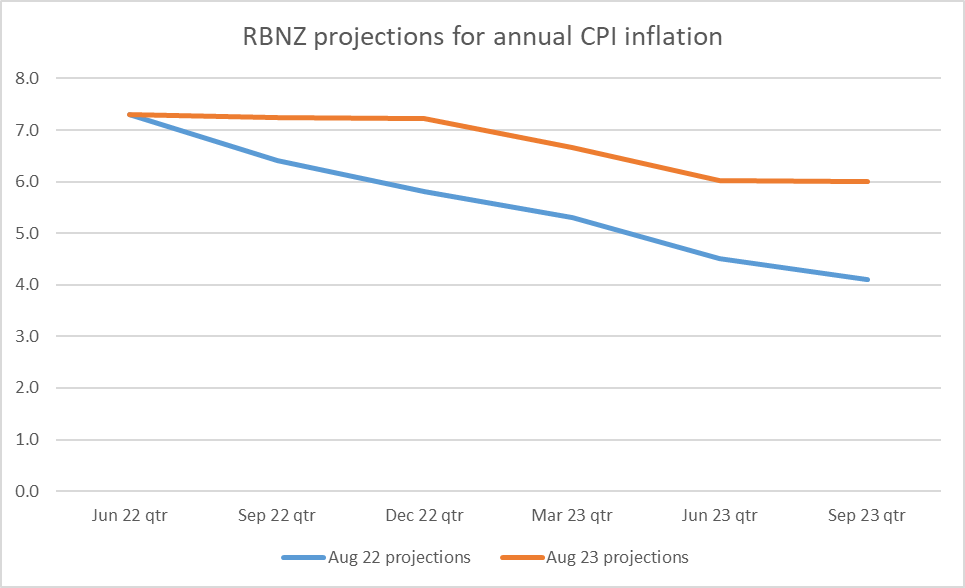

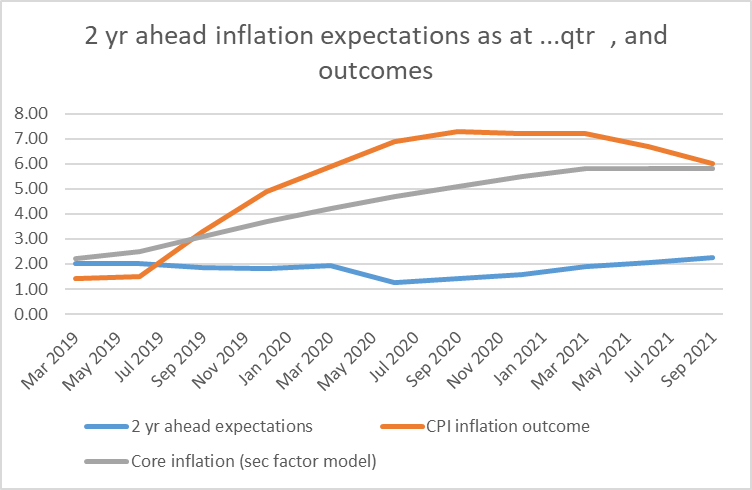

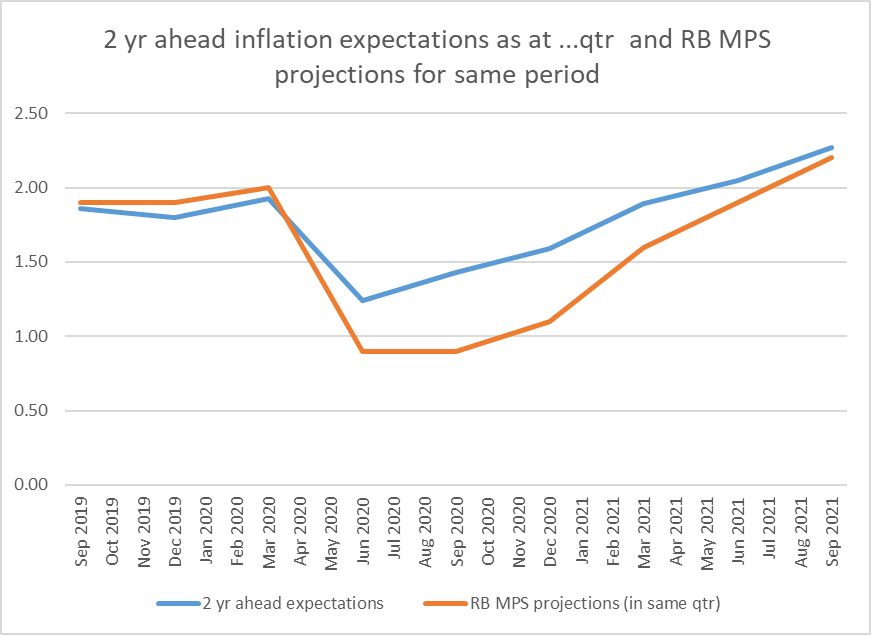

Or we could – although let us fervently hope not – have a repeat of the last few years in which most everyone – RB, Treasury, outside forecasters – misunderstand and misjudges the severity of the pressures giving rise to the inflation, and thus the seriousness of the inflation problem. Back in November 2021 the Reserve Bank’s best professional opinion (presumably) reflected in their published forecasts was that inflation would have been back within the target range by March 2023 (a mere 18 months), with the OCR never having gone above about 2.5 per cent. Given a target to get inflation back in 12-18 months they’d have thought they were on course. That was wrong, of course, but the addition of a time-bound target wouldn’t have helped greatly with what was mainly a forecasting/understanding problem by then.

I do think there is reason to amend the remit. At present it does not really deal with mistakes like the last few years at all, stating just

which tends to treat all deviations are much like those resulting from GST or indirect tax changes, and never really envisages the need to correct serious policy failures (of the sort we’ve seen in the last few years). A provision that read something like “when the inflation rate moves outside the target range, or persistently well away from the target midpoint, the MPC shall explain (a) the reasons for these actual/forecasts deviations, and (b) the timeframe over which they expect inflation to return to around the target midpoint, and the reasons for that timeframe.” would be a useful addition. If the government was unwise to go down the “specific set time targets” path it would then need to allow for resetting/renegotiating such time targets when, as is inevitable, sustained shocks/mistakes happen. It was a model used in the very first (low-trust) Policy Targets Agreement, and was sensibly dropped a few months later in favour of the emphasis on transparent accounting.

The case for moving to a Monetary Policy Committee has been pretty compelling for decades (at least since Lars Svensson first recommended the shift in his 2001 review commissioned by the then-new Labour government) and it is to the credit of the 2017 to 2020 government that they finally made a change to a committee system. Not only is there no other area of public life (or politics) in New Zealand in which we delegate so much power – without appeal or review scope – to a single individual (Luxon himself can be ousted by his caucus with no notice), but hardly any other central bank anywhere operates a single decisionmaker system (the Bank of Canada is an exception in law – a legacy of old legislation – but they are at pains to stress that their senior management Governing Council functions as a collective decisionmaking body for monetary policy).

The right path now is not to strengthen the hand of the Governor – perhaps especially the current one if they are stuck with him – but to strengthen the Committee around whoever is Governor. It was quite disquieting to see ACT pushing for a return to the pre-2019 system. The old arguments about “we can sack one person not a whole board or committee” not only aren’t right generally (look at council, hospital boards, boards of trustees who’ve been replaced) but aren’t right in the specific context of monetary policy, and not only because in the face of the biggest monetary policy failure in decades no one lost their job, not even the person who was clearly most responsible (for the outcomes and the spin and misrepresentations around them). In practical terms, even if Orr could be removed shortly, it would be quite a punt in the dark to return to a single decisionmaker model, the more so when there is no single ideal candidate around whom people have united as “the” person to replace Orr.

Much better to focus on (a) replacing Orr as and when you can, b) reopening urgently the application process for the appointment of external MPC members to ensure that really strong candidates are appointed early next year (not those who got through the Robertson/Orr/Quigley RB winnowing process, selecting for people who won’t rock the boat, and have not rocked the boat in the last 3-4 years when things went so badly wrong at the Reserve Bank), and (c) amend the MPC charter etc to (a) require individual MPC members to record votes at each meeting, b) to require those votes to be published, c) to encourage external MPC members to give speeches/interviews, and d) to require FEC hearings for all MPC members before they take up their appointments. None of that requires statutory changes. It could usefully be backed

(There is course no guarantee that a better more-open MPC would have produced a less-bad set of inflation and LSAP outcomes this time – many other countries with better central banks have done pretty much as badly – but that is not a reason to simply settle for an inadequate status quo, one in which we never hear from most of these powerful officials, there seems to be no effective accountability, all supported by little or no serious research, analysis or insight.)

UPDATE: I meant to include this (from Stuff this morning), and now include it mostly for the record. As I said in my earlier post, there is no great harm in the independent review (of monetary policy under Covid) that they are talking of, but it also isn’t clear what is to be gained (and much will depend on who is appointed to do it). The failings of the RB in recent years are pretty well-understood, and the institution commands little respect now. If change is to be made, just get on and start now.