As I was writing this, the Reserve Bank’s latest set of regulatory interventions and controls were announced. I haven’t yet read that document but from the press release I would make just three observations:

- The flip-flops continue. After easing the LVR restrictions for non-investors outside Auckland last year, they now plan to totally reverse that change. As a reminder, when these controls were first introduced three years ago, they were all supposed to be “temporary”. So, I suppose, were the exchange controls, introduced in 1938 and lifted in 1984,

- The consultation process is a joke. Not long ago, as part of their regulatory stocktake, the Bank indicated that it intended to put in place materially longer consultative periods for its proposed regulatory initiatives (typically six to ten weeks). But in today’s announcement they are allowing only three weeks for submissions on the new “proposals” to be made, and then plan to implement the changes three weeks after that. Only 10 days ago they were talking languidly of “a measure that could potentially be introduced by the end of the year”. There is no real consultation going on, simply jumping through what they must regard as the bare minimum of legal hoops they must be seen to comply with. And they will, no doubt, continue to refuse to publish most of the submissions. It is, frankly, a travesty of democracy – and the nature of what is going on is well-illustrated by the Governor’s statement that “We expect banks to observe the spirit of the new restrictions in the lead-up to the new policy taking effect.” Citizens – even banks – are required to obey the law, not the wishes and whims of officials, elected or otherwise. None will do so of course – they are all too scared to challenge the Reserve Bank in public – but it would be interesting if a bank were to seek a judicial review of what is going on here.

- The policy remains as incoherent as ever, in that the LVR restrictions will not apply to loans for new house building, even though the risks of losses are materially higher on new buildings – often on the peripheries of towns/cities – than on existing ones.

I was away when Grant Spencer’s 7 July speech on housing was released, and although I glanced through it then on my phone, last night was the first time I had sat down and read it carefully. It was really quite disappointing.

I say that not primarily because I disagree with Spencer on many points – although I do. But reasonable people can interpret the same data and experiences in different ways. What concerns me is that the Reserve Bank still doesn’t seem to have a disciplined framework for thinking about housing markets here or abroad, or about its role in respect of the efficiency of the financial system, and simply doesn’t back up its claims with much analysis or research at all.

Grant Spencer gave a speech on housing in April 2015, shortly after I started this blog. At the time I was quite critical of that speech (here and here), and rereading those comments this morning I could easily simply repeat most of them now. They apply as much to the latest speech as to the one given 15 months ago. Back then I concluded:

Without more detailed and extensive analysis, it is still difficult to escape the conclusion that the Reserve Bank’s approach to housing is being shaped more by impressions of the US last decade than by robust in-depth analysis of the sorts of specific risks the New Zealand economy and, in particular, New Zealand banks and the New Zealand financial system face.

That still seems to be the case.

Of course, not everything can be covered in a single speech. But good speeches by authoritative senior central bankers typically draw on analysis and research undertaken in their own institution and elsewhere. But Spencer’s speech has no references to any other Reserve Bank research and analysis (other than his own April 2015 speech) and in fact no significant references to anyone else’s research or analysis either – whether to support his case, or respond to alternative perspectives.

And even though Spencer is the Deputy Governor with explicit responsibility for the Bank’s financial stability functions, nowhere does he even mention the Bank’s stress tests. Perhaps he disagrees with the assumptions that were used in doing the stress tests – but if so, he should have had them changed – or perhaps the results are simply uncomfortable given that he knew his boss was champing at the bit to impose yet more controls. But it should be seen as simply unacceptable for a major speech on housing from the central bank’s financial stability Deputy Governor to not even engage with the stress test results.

There is also nothing in the speech on how the Bank thinks about the implications of its ever-growing web of controls for the efficiency of the financial system – an explicit (and equal) part of the Bank’s financial regulatory responsibilities. In his latest letter of expectation to the Bank, released a few days ago, the Minister of Finance indicated to the Governor that he expected the Bank to produce analysis on how the stability and efficiency goals were being balanced. Four months on from when that letter was written, there is nothing at all in Spencer’s speech.

The Reserve Bank has explicit statutory responsibility for monetary policy, and for financial regulation to promote the soundness and efficiency of the financial system. It has no statutory responsibility for the housing market, or house prices per se. And it certainly has no responsibility for tax policy, immigration policy, land use regulatory policy, fiscal policy, policy around Urban Development Authorities, and so on. And yet in the speech, Spencer weighs in on all of them.

That is not good practice generally, and particularly not in this case where the Bank’s comments seem to be based on no supporting analysis at all. Central banks are given quite considerable power in specific and limited areas, but continued support for central bank independence (whether in monetary policy or financial regulatory policy) depends in part on a sense that (a) the central bank is a technocratic, limited, institution that doesn’t involve itself in other partisan or politically contentious issues, and (b) that when on very rare occasions the central bank might weigh in on matters outside its direct ambit, it does so backed by very sound research and analysis. Since central banks often have considerable research capacity, at times such research might be able to shed useful light on some of these wider issues. But neither of those criteria are met with the material in this speech.

I happen to agree with the Deputy Governor that the government should be reviewing immigration policy – which is itself quite a change of stance from the Governor’s view on immigration only a few months ago – but I don’t think it is a matter on which the Reserve Bank should be expressing a view. And in particular, it should not be expressing such views without the supporting research and analysis. There appears to be none behind these comments.

Much the same might be said for the government’s recent announcement of a Housing Infrastructure Fund – the $1000m fund under which the government on behalf of the rest of us will lend interest-free to councils in high population growth areas. The Deputy Governor opines that this will “help to relieve an important constraint”, except that (a) he references no analysis in support of this claim, which is perhaps not surprising as (b) no one has yet seen the details of the fund, which appeared to many to be more about getting a weekend’s headlines rather than making a very material difference to the housing situation (recall that it is a $25m per annum interest subsidy, which doesn’t seem likely to make very difference to anything that matters to a macro-focused agency).

Similar comments could be made about the Deputy Governor’s views on taxes or Urban Development Authorities (compulsory acquisition wasn’t explicitly mentioned, but I assume he is probably sympathetic). It is tempting to lodge an OIA request asking for copies of the analysis the Bank used in support of each of these policy preferences, but it is easy enough to guess how little there would be. After all, Spencer has form. In his speech last year, he advocated introducing a capital gains tax. When I asked for the analysis etc in support of that proposal – and was pretty sure there was none, as I’d left the Bank only a couple of weeks earlier and had previously written any material the Bank had on CGTs – it boiled down to a single brief email. It really isn’t good enough.

I could go on. The Bank has still produced no analysis that looks carefully at the international experience of the last decade, including considering the countries where house prices did fall sharply and, as importantly, those where they did not. Instead, they cherry-pick a couple of countries with bad experiences, and don’t ever stop to analyse the similarities and differences between those countries and their policy interventions and the New Zealand situation. They have still produced nothing explaining why they think the risks are now so much greater than in 2007, even though the banks’ buffers are bigger, and any mood of exuberant optimism is much more attenuated. While I was still at the Bank I used to pose that latter question to Grant, and never got a serious attempt at a response.

The Bank also continues to anguish about the low level of global interest rates – the same attitude that has continued to leave them (and the Governor specifically) too reluctant to simply do their main job and keep inflation near-target. But even there, what they have to offer is unconvincing. We are told that low real interest rates are “a worldwide phenomenon linked to post-GFC caution”, with no mention of the weak underlying productivity growth and demographics pressures that are at play. In other words, they treat low interest rates as some exogenous event, rather than something that is an endogenous response to the apparently poor fundamentals, here and abroad. Partly as a result we get anguishing about low interest rates driving up house prices, rather than a considered reflection on what it is that means interest rates in New Zealand need to be as low – or lower – than they are. For example, real per capita income growth is much less than it was.

Related to this, they simply ignore how not-very-widespread any serious housing market stresses really are. If low real interest rates were a major factor in the overall house price story we might reasonably have expected to see real house prices well above where they were at the end of the last boom. After all, at the end of that boom the OCR was 8.25 per cent, and today it is 2.25 per cent. Inflation expectations have fallen of course, but real interest rates are a lot lower than they were.

House prices not so much. I downloaded the QV house price index data. On the QV numbers, house prices nationwide have risen 18.5 per cent since the peak in 2007. But the CPI has risen 18.1 per cent over that period. In other words, in real terms nationwide house prices are barely changed from where they were in 2007, despite the sharp fall in real interest rates – and the boom that peaked in 2007 was much bigger credit event than what we have seen so far, and didn’t end in banking system stresses.

In fact, plenty of places in New Zealand have real house prices today materially lower in real terms (and sometimes in nominal terms) than they were in 2007. Here is an illustrative chart from the QV data

Of course, the overall level of house (and urban land) prices in New Zealand remains far too high – far higher, relative to incomes, than in the vast swathes of the US with well-functioning housing supply markets – but in terms of the last decade or so, what we have had in mostly an Auckland boom. It is a very big boom in Auckland – as one might expect when unexpectedly rapid population growth collides with land use restrictions – and Auckland is a big place in a New Zealand context, but it is hardly a nationwide phenomenon. There is some spillover from Auckland to places like Hamilton, and the earthquake related pressures put, probably temporary, pressures on prices in Christchurch and surrounds. But vast swathes of the country – including our now second largest city – have seen no real house price inflation over almost a decade, or in some cases really quite substantial falls. There are plenty of smaller TLAs that I haven’t shown individually – and almost all of them have had falling real prices – but they are included in the overall New Zealand number.

One would know nothing of this from reading the Spencer speech. And quite why the Bank considers it appropriate to have tight controls on access to housing finance in Gisborne, Wanganui and Invercargill remains a mystery – perhaps the new consultative document will shed some light, but I rather doubt it.

The citizens of New Zealand deserve (a lot) better from the Reserve Bank – and frankly, from those charged with holding it to account. Of course – since the housing problems are primarily a responsibility of the government – we also deserve a lot better from the government. Sadly, the Reserve Bank continues to take responsibility on itself for something it is not charged with, and then does not back up its claims with the standard of analysis and research that we have a right to expect. Far-reaching reforms are needed – different governance structures, reformed legislation, and different people across the top ranks of the Bank.

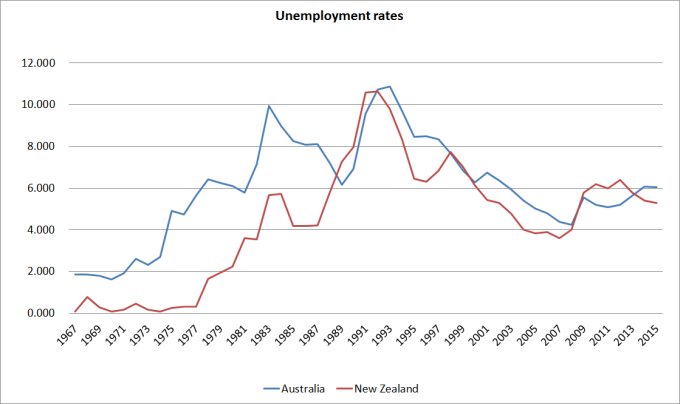

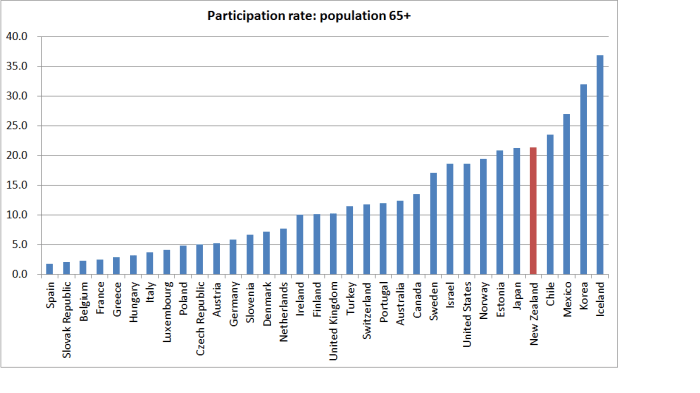

And the unemployment rate among older people is very low indeed – before the recession and now both around 1.5 per cent. That makes sense – older people have New Zealand Superannuation to fall back on, with no work test, so there is typically no urgency to find another job (to be “actively seeking”). But it is a very different – and less cyclical – unemployment rate than that for the rest of the workforce.

And the unemployment rate among older people is very low indeed – before the recession and now both around 1.5 per cent. That makes sense – older people have New Zealand Superannuation to fall back on, with no work test, so there is typically no urgency to find another job (to be “actively seeking”). But it is a very different – and less cyclical – unemployment rate than that for the rest of the workforce.

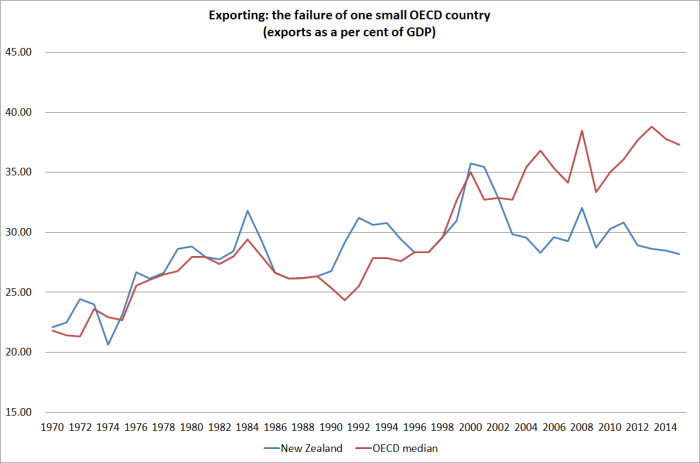

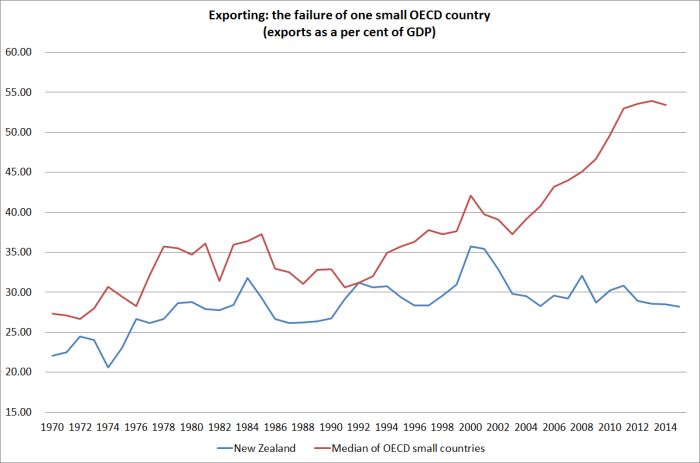

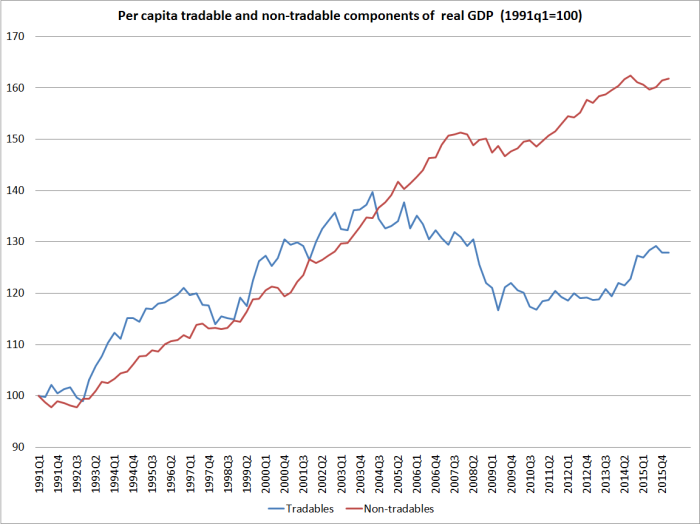

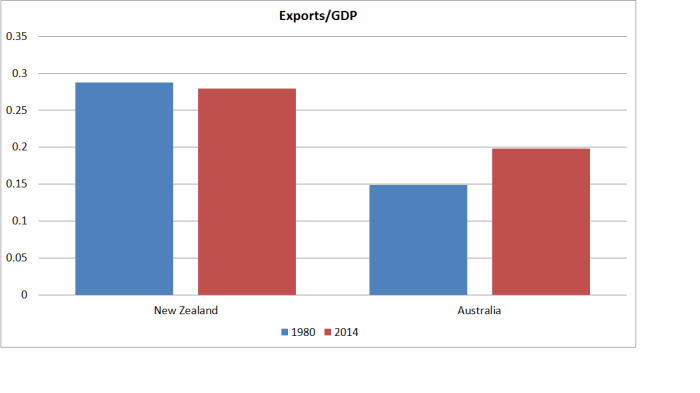

New Zealand’s export share of GDP hasn’t changed in 35 years.

New Zealand’s export share of GDP hasn’t changed in 35 years.