By international standards that is. And that gap, between our interest rates and those abroad, is nothing much to do with monetary policy.

If the new government is serious about addressing New Zealand’s dismal long-term productivity growth record – which has been particularly poor in the last five years – it needs get serious about recognising that one of the key symptoms of our structurally unbalanced economy is that persistent gap between real interest rates in New Zealand and those almost anywhere else in the world.

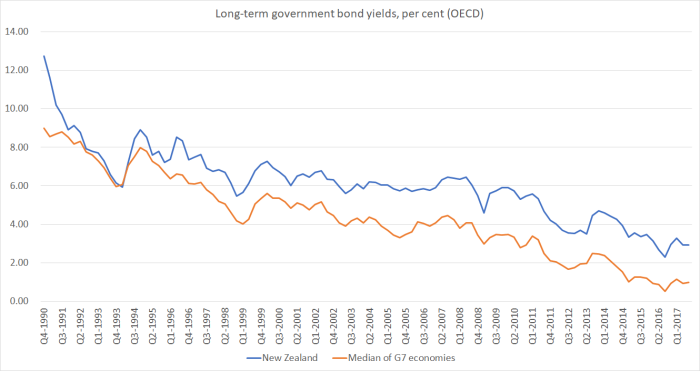

Of course, the big story about interest rates over the last 25 years or more has been the persistent downward trend in the level of nominal and real interest rates. In this chart, I’ve illustrated that for New Zealand and the median of the G7 advanced economies, using the OECD’s series of long-term interest rates (usually a 10 year government bond). To stress, these aren’t central bank policy rates, but market-determined long-term yields.

Once upon a time, very briefly, our long-term interest rates actually touched those (median) foreign rates. But the dominant story in both series is the downward trend. In fact, there is no real sign that the trend has yet ended – each peak, for example, still looks a little lower than the previous one.

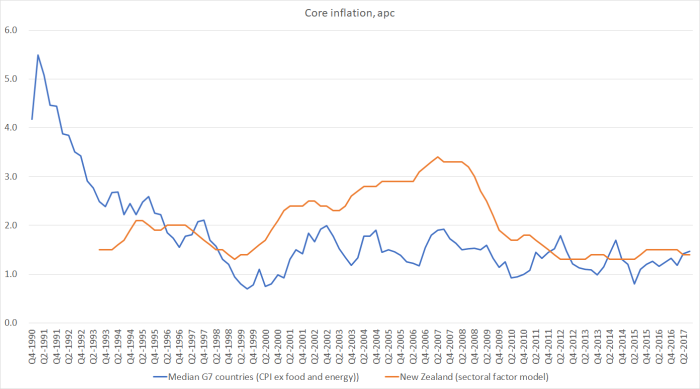

Inflation was falling a lot in many countries in the 80s and early 90s, but for the last 20 years or so core inflation has been pretty low and stable in the core advanced economies. In other words, the falls in international interest rates in the last 20 years or so have almost entirely been falls in real interest rates too.

What about the gap between New Zealand and world interest rates? Here is the gap between the two series shown in the first chart above.

The gap collapsed, briefly, in the early 1990s as we got on top of inflation, actual and expected short-term interest rates came down, and NZD assets became very attractive globally. But the compression didn’t last. Since around 2004 the gap between New Zealand bond yields and this measure of global rates has fluctuated around 200 basis points, with no obvious trend. (The gap is smaller than that, typically, relative to the United States, and much larger relative to Japan and Germany.)

(I should stress that there is no single right way to summarily aggregate the various overseas long-term interest rates. Whichever median of some of all OECD countries I used, the broad pattern was much the same, although the absolute size of the gap differs.)

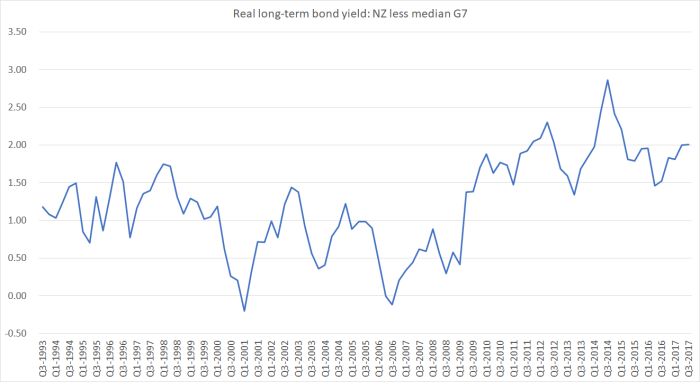

What about real interest rates. In this chart, I’ve adjusted the median G7 nominal interest rates using the median CPI inflation ex food and energy (the core inflation measure the OECD reports) for the G7 countries, and adjusted the New Zealand interest rates by the Reserve Bank’s preferred sectoral factor model measure. The sectoral factor model data starts only in September 1993, so that is when I start this chart. In principle, one might want to do the adjustment using measures of inflation expectations, but there are no consistent long-term measures available across countries. Core inflation can be thought of as a proxy for inflation expectations.

Not only has there been no sign of the gap between New Zealand and “world” real interest rates closing, but if anything the gap has been wider since around 2009/10 than we’d seen previously. On this measure, the gap has averaged 190 basis points over the past 8 years.

These are really large gaps. On this measure, over the life of a 10 year bond they make for a 20 per cent difference in total returns. That makes it a lot harder for a potential investment project evaluated in New Zealand to stack up than it would be for an equivalent project in other countries.

It is also tends to be reflected in big differences in exchange rates. Those higher yields in New Zealand, if expected to persist, will look very attractive to overseas investors. It might even look like a “free lunch”. What takes away the “free lunch” dimension is an appreciation in the real exchange rate now, such that over the following 10 years the exchange rate is expected to depreciate just enough to leave the investor indifferent between holding NZD assets and those in other currencies. That isn’t a mechanical relationship, but it is a pretty strong tendency. It is the bigger-picture of the sort of modest jump (fall) in the exchange rate we often see when a Reserve Bank OCR announcement is surprisingly hawkish (dovish). Comparing 10 year rates, it could account for a 20 per cent ‘overvaluation’ of the exchange rate. On even longer-term rates the cumulative differences are even larger. No wonder we don’t see much new investment in the tradables sector in New Zealand.

Perhaps you still doubt that the real interest rates gaps can really be as large as these summary series suggest. We can check the sotry by looking directly at yields on inflation-indexed bonds issued by governments in various advanced countries. Getting time series data for some of these countries can be a pain (unless one is setting in front of a Bloomberg terminal), but these are some of the current interest rates I tracked down a few days ago.

Our longest maturity inflation indexed bond matures in September 2040 (23 years away). On Monday the Reserve Bank was reporting a real yield of 2.22 per cent on that bond.

The Australian government issues an indexed bond maturing on exactly the same date. The real interest rate on that bond, again on Monday, was (so the RBA reports) 1.18 per cent.

So even relative to Australia – which also has quite high interest rates by advanced standards – our very long-term real interest rates are very high.

What about some other countries?

The United States has an inflation indexed bond maturing in February 2040. According to the Wall St Journal tables that bond opened the week yielding 0.89 per cent, roughly 130 basis points lower than the New Zealand 2040 bond.

Canada has a 2044 indexed bond, which was yielding about 0.75 per cent.

I could only find data for a 10 year Japanese inflation indexed bond, which appeared to be yielding about -0.4 per cent.

And Germany offers a range of maturities for its government inflation indexed bonds. A few days ago, the 2030 bond was yielding -0.67 per cent, and the 2046 bond – almost 30 years to maturity – was yielding -0.34 per cent.

(UK indexed bond yields are not directly comparable because the tax treatment of the inflation adjustment is materially different).

There is certainly a range of real long-term yields across countries. But ours are extremely high relative to those in other core advanced economies.

A year ago, I wrote a post along similar lines (although looking at the data in slightly different ways). In that post I concluded

…our interest rates (a) are and have been higher than those abroad, (b) this is so for short and long term interest rates, (c) is true even if we look just at small countries, and (d) is true in nominal or real interest rate terms. And the gap(s) shows no sign of closing.

All that is as true today as it was then. It should be worrying anyone seriously interested in lifting New Zealand productivity and long-term per capita income performance. On Monday, I will review some of the possible explanations for the gap – partly to back the claim that it is a symptom that we should be worrying about, and partly to point in the direction of possible, and sensible, remedies.