By international standards that is. And that gap, between our interest rates and those abroad, is nothing much to do with monetary policy.

If the new government is serious about addressing New Zealand’s dismal long-term productivity growth record – which has been particularly poor in the last five years – it needs get serious about recognising that one of the key symptoms of our structurally unbalanced economy is that persistent gap between real interest rates in New Zealand and those almost anywhere else in the world.

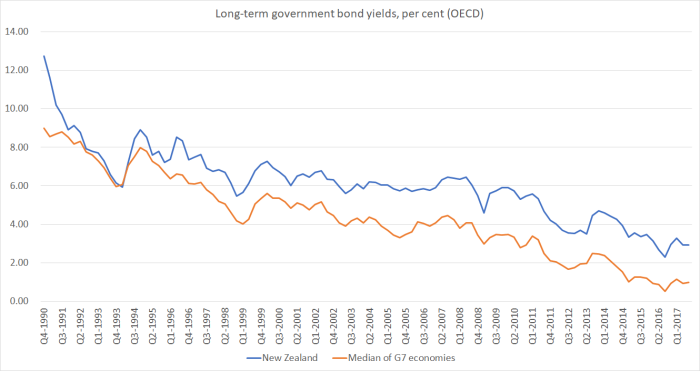

Of course, the big story about interest rates over the last 25 years or more has been the persistent downward trend in the level of nominal and real interest rates. In this chart, I’ve illustrated that for New Zealand and the median of the G7 advanced economies, using the OECD’s series of long-term interest rates (usually a 10 year government bond). To stress, these aren’t central bank policy rates, but market-determined long-term yields.

Once upon a time, very briefly, our long-term interest rates actually touched those (median) foreign rates. But the dominant story in both series is the downward trend. In fact, there is no real sign that the trend has yet ended – each peak, for example, still looks a little lower than the previous one.

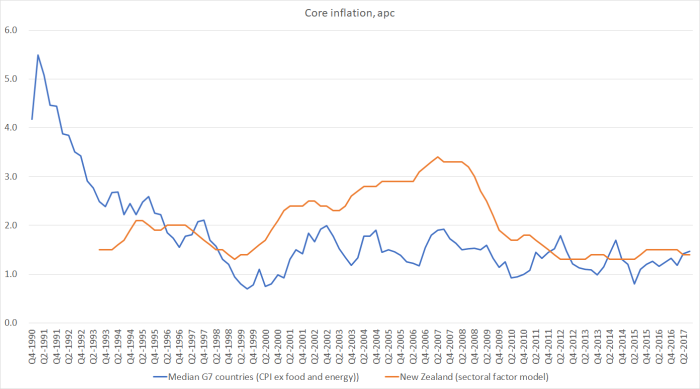

Inflation was falling a lot in many countries in the 80s and early 90s, but for the last 20 years or so core inflation has been pretty low and stable in the core advanced economies. In other words, the falls in international interest rates in the last 20 years or so have almost entirely been falls in real interest rates too.

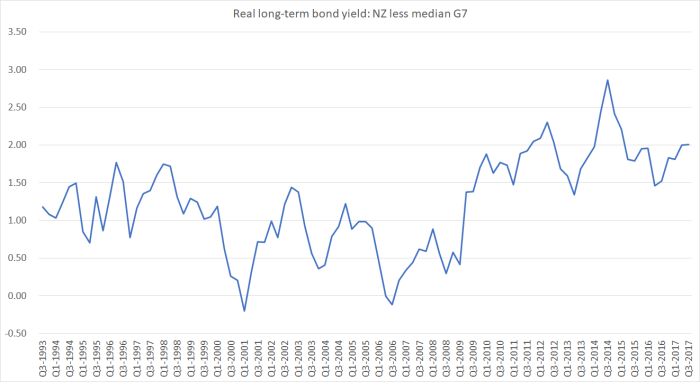

What about the gap between New Zealand and world interest rates? Here is the gap between the two series shown in the first chart above.

The gap collapsed, briefly, in the early 1990s as we got on top of inflation, actual and expected short-term interest rates came down, and NZD assets became very attractive globally. But the compression didn’t last. Since around 2004 the gap between New Zealand bond yields and this measure of global rates has fluctuated around 200 basis points, with no obvious trend. (The gap is smaller than that, typically, relative to the United States, and much larger relative to Japan and Germany.)

(I should stress that there is no single right way to summarily aggregate the various overseas long-term interest rates. Whichever median of some of all OECD countries I used, the broad pattern was much the same, although the absolute size of the gap differs.)

What about real interest rates. In this chart, I’ve adjusted the median G7 nominal interest rates using the median CPI inflation ex food and energy (the core inflation measure the OECD reports) for the G7 countries, and adjusted the New Zealand interest rates by the Reserve Bank’s preferred sectoral factor model measure. The sectoral factor model data starts only in September 1993, so that is when I start this chart. In principle, one might want to do the adjustment using measures of inflation expectations, but there are no consistent long-term measures available across countries. Core inflation can be thought of as a proxy for inflation expectations.

Not only has there been no sign of the gap between New Zealand and “world” real interest rates closing, but if anything the gap has been wider since around 2009/10 than we’d seen previously. On this measure, the gap has averaged 190 basis points over the past 8 years.

These are really large gaps. On this measure, over the life of a 10 year bond they make for a 20 per cent difference in total returns. That makes it a lot harder for a potential investment project evaluated in New Zealand to stack up than it would be for an equivalent project in other countries.

It is also tends to be reflected in big differences in exchange rates. Those higher yields in New Zealand, if expected to persist, will look very attractive to overseas investors. It might even look like a “free lunch”. What takes away the “free lunch” dimension is an appreciation in the real exchange rate now, such that over the following 10 years the exchange rate is expected to depreciate just enough to leave the investor indifferent between holding NZD assets and those in other currencies. That isn’t a mechanical relationship, but it is a pretty strong tendency. It is the bigger-picture of the sort of modest jump (fall) in the exchange rate we often see when a Reserve Bank OCR announcement is surprisingly hawkish (dovish). Comparing 10 year rates, it could account for a 20 per cent ‘overvaluation’ of the exchange rate. On even longer-term rates the cumulative differences are even larger. No wonder we don’t see much new investment in the tradables sector in New Zealand.

Perhaps you still doubt that the real interest rates gaps can really be as large as these summary series suggest. We can check the sotry by looking directly at yields on inflation-indexed bonds issued by governments in various advanced countries. Getting time series data for some of these countries can be a pain (unless one is setting in front of a Bloomberg terminal), but these are some of the current interest rates I tracked down a few days ago.

Our longest maturity inflation indexed bond matures in September 2040 (23 years away). On Monday the Reserve Bank was reporting a real yield of 2.22 per cent on that bond.

The Australian government issues an indexed bond maturing on exactly the same date. The real interest rate on that bond, again on Monday, was (so the RBA reports) 1.18 per cent.

So even relative to Australia – which also has quite high interest rates by advanced standards – our very long-term real interest rates are very high.

What about some other countries?

The United States has an inflation indexed bond maturing in February 2040. According to the Wall St Journal tables that bond opened the week yielding 0.89 per cent, roughly 130 basis points lower than the New Zealand 2040 bond.

Canada has a 2044 indexed bond, which was yielding about 0.75 per cent.

I could only find data for a 10 year Japanese inflation indexed bond, which appeared to be yielding about -0.4 per cent.

And Germany offers a range of maturities for its government inflation indexed bonds. A few days ago, the 2030 bond was yielding -0.67 per cent, and the 2046 bond – almost 30 years to maturity – was yielding -0.34 per cent.

(UK indexed bond yields are not directly comparable because the tax treatment of the inflation adjustment is materially different).

There is certainly a range of real long-term yields across countries. But ours are extremely high relative to those in other core advanced economies.

A year ago, I wrote a post along similar lines (although looking at the data in slightly different ways). In that post I concluded

…our interest rates (a) are and have been higher than those abroad, (b) this is so for short and long term interest rates, (c) is true even if we look just at small countries, and (d) is true in nominal or real interest rate terms. And the gap(s) shows no sign of closing.

All that is as true today as it was then. It should be worrying anyone seriously interested in lifting New Zealand productivity and long-term per capita income performance. On Monday, I will review some of the possible explanations for the gap – partly to back the claim that it is a symptom that we should be worrying about, and partly to point in the direction of possible, and sensible, remedies.

So far the only remedy you have suggested has been to drop the migrant residency to 15k a year from 50k a year. That is just playing with numbers because a target can either be exceeded or be below which currently occurs regularly with our 50k residency target anyway. But there most of these are actually foreign workers and international students that are already here therefore changing the target does not change the actual physical numbers.

Your alternative remedy is to wish that population was back to around 2 million people. That is also not exactly a remedy. More like wishful thinking of the British Empire days of how great we were with 70 million sheep and selling our wool to the ends of the British Empire with our laid back farmers that sat in their mansions sipping wine and beating up Maori to tend to the sheep and of course still considered a high productive economy because Maori was not actually counted as people and sheep just needed well trained sheep dogs.

LikeLike

your second (rather caricatured to say the least) para is not relevant to the interest rate question, but to a different issue about the resource-dependency of the NZ economy, and whether we can ever hope to gravivate away from that while still being among the richer countries on earth.

LikeLiked by 1 person

Time and time again, you have made the immigration driven population growth strategy as one of the reasons for our high interest rates regime. You need to be more consistent in your hypothesis.

High Immigration = high population = high interest rates = high NZD

LikeLike

I think it is good to remind people of this chart occasionally.

LikeLike

I think, given we’ve abandoned the idea of free markets via central banking, anyway, and thus price discovery of every asset class by a free market, then RBNZ should carry the mandate to ‘control’ – or at least try to, because it is a forlorn goal – the inflation in asset prices it has created, not just consumer inflation, plus, put a moral mandate – again, given this is now all artifice – to protect the savings incomes of the prudent elderly whom have been, unfortunately, forced to speculate and herded into risky assets that are bound for correction – and I think sharply – due to RBNZ (and every Western central bank) stimulunacy. Elderly savers have seen their incomes shredded, and are the one group in society that don’t have time to change their circumstances. Those that have desperately chased yield in bond funds, or gone onto (way)over-valued sharemarkets, will be worse off. Those that have stuck to a prudent level of risk have seen large a deterioration in their standard of living.

Reducing interest rates, in this artificial environment, so sacrificing, again, again, again, savers to unproductive speculators and dairy shit-ponds is deeply immoral, because setting the OCR is, also, a moral exercise, as is everything once you leave spontaneous order for command driven allocation. I couldn’t disagree with you more, Michael.

Regarding the notion long term yields are free market based, not down to central bank policy, I don’t agree, because a central bank is a command distorter of a free market by its ability to affect asset prices: proof – the West’s current asset bubbles in every class from housing to stocks, etc, that, to repeat myself, have distorted (destroyed) price discovery (and hence long term yields).

Signed: long-lost free-marketer living in the ruins of the West.

Addendum: my quality of life is dependent, in some big part, from imports, from food, to tech, to books, to cars, etc, so I would rather have a strong currency (believing that exports are merely the cost of our imports). Yay for an over-valued currency (all other things being command-economy artifice).

You will not agree on any point 🙂

LikeLike

You are mostly right about me disagreeing, although I am pretty deeply sympathetic to the old savers (and not just because I’m also the trustee of a super fund that relied on assumptions about materially higher fixed interest returns than we are now experiencing). Our difference is probably over what can be done about it. I’ve love to be in a world where higher real interest rates were going hand in hand with an acceleration of productivity growth. But over the last decade or more, global productivity growth has been poor, and global population growth has been slowing. In a totally free market, both of those trends would show up in a fall in real interest rates (less demand for real resources for investment purposes).

Similarly, I would much rather we could close the interest rate gap between us and the rest of the advanced world through global rates rising (supported by changing fundamentals) and ours rising just a bit less. But whichever direction the closure comes from, closing the gap is a vital part of getting the exchange rate down. I’m an (import) consumer too, but in the medium-term consumption is supported only by income growth, and income growth is hard to secure in NZ at anything like the sort of exchange rate we’ve had for the last decade or more. Really successful economies tend to have rising real exchange rates, but the current “command economy” imbalances – led from immigration policy – result in the cart (exchange rate) going before the horse (stronger productivity). And that isn’t a path that works.

LikeLiked by 1 person

….and in which sector does productivity mainly take place? the private sector where risk taking is rewarded with a judgement based risk premium: sitting on cash and expecting a positive real return after tax is a historical aberration (i.e. no risk = zero return)…..in my unfounded opinion…!

LikeLike

1) Would it be possible to use inflation indexed bonds in some way as a proxy for inflation and redo the interest rate differential graphs?

2) I wondered how a graph of the real long term bond differential and the GDP differential would look? Negative correlation?

LikeLike

I certainly couldn’t do 1. – data requirements are too much (and the UK IIBs are taxed differently, and not all G7 countries have had them on issue for the whole period).

On 2, not sure about real GDP itself, but certainly our real GDP per hour worked growth over this period will have been weaker than the G7 or OECD median.

LikeLike

Michael,

Thinking through the real interest rate gap (follow the money flow) can we summarize it as?:

1) Savings levels in NZ are low (from the point of view of it not being locked up in an ever increasing housing supply to meet the high % population growth)

2) That means that for both government and private borrowing (the latter is mainly housing) that most of the funding is coming from overseas

3) Overseas lenders have the option of lending in their domestic market or lending to NZ. If they lend in their domestic market they don’t have to worry about exchange rate fluctuations.

4) For them to lend to NZ they will take out swaps etc to cover the exchange rate risk. There is a cost to this which has to be covered by a premium in the real rate of return the lenders demand. There may be additional risk premium as NZ is small and the amount of lending relatively small – so we are also closer to the fixed cost of a lending transaction.

We would seem to be on the long path of removing some of this distortion:

– reducing the immigration rate (reduced need for infrastructure spending for growth) – maybe not enough

– increasing kiwisaver funds – the savings are more flexible capital than housing mortgage funding & can go towards productive growth assets

– increasing term deposits – along with kiwisaver provide an increasing local capital base

– ACC & Superfund increasing- yes, but a lot of it is invested overseas

– Savings = Investment. The more domestic savings we have the lower the cost of capital (lower lending premium vs international lending) & more efficiency for businesses. (yes housing is an asset that can be used to back a business but they generally back small businesses which don’t have economies of scale)

LikeLike

I’ll cover much of this is my post today. Do recall that there is no sign that the national savings rate is increasing, and altho immigration net inflows will fluctuate, there is nothing in current policy promises that will reduce average future immigrant numbers.

LikeLike

I suspect with Auntie Helen back at the helm behind the scenes and one of Helen’s top aides back within Labour’s closest advisers, immigration as an issue is off Labours agenda.

“Former Prime Minister Helen Clark’s top advisor, Heather Simpson, has returned to advise the new Labour Government.

Ms Simpson has a three-decade working relationship with Ms Clark, working as chief of staff to the Labour Party before spending eight years advising Ms Clark at the UN.”

http://www.newshub.co.nz/home/politics/2017/10/h2-helen-clark-s-top-advisor-returns-to-labour-party.html

LikeLike

I wonder when Dr Michael Cullen would be back advising Labour’s Finance team. At the moment with Grant Robertson as Finance Minister, Labours finance team looks rather like a 2 year old trying to understand what a Statement of Financial Position or Balance Sheet actually means.

LikeLike

[…] Friday’s post, I illustrated how persistent and large the gap between New Zealand long-term interest rates and […]

LikeLike