In my post yesterday, buried well down amid long and fairly geeky material, I showed this chart.

Using official SNZ data, it suggests that over the last 15 years or so nominal wage rates in New Zealand have risen materially faster than the income-generating capacity of the New Zealand economy (nominal GDP per hour worked – a measure that takes account of the terms of trade). Since a big part of what New Zealand firms are selling when they try to compete internationally is (the fruits of) New Zealand labour, it probably shouldn’t be too surprising that our tradables sector producers have been struggling. As a reminder, we’ve had no growth in (a proxy measures of) real tradables sector GDP since around 2000 – two whole governments ago.

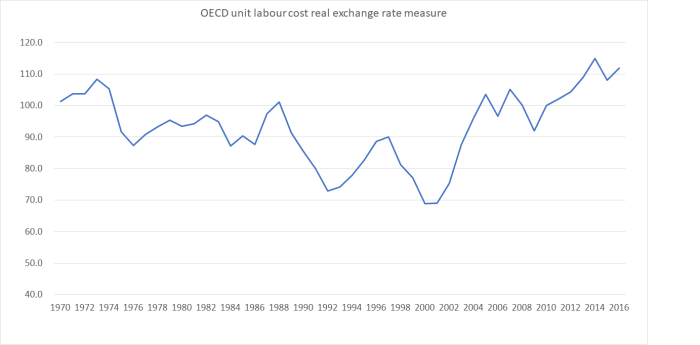

The OECD publishes a real exchange series, all the way back to 1970, using real unit labour cost data. Unit labour costs are, in effect, wages adjusted for productivity growth. The real exchange rate measures compares how our economy has done on this competitiveness measure.

(There are other real exchange rate measures in which the fine details are less stark, but the picture is very similar.)

Broadly speaking, our real exchange rate was trending gradually downwards for the first 30 years of the series. And each trough was a bit lower than the one before it. That was, more or less, what one might have expected. New Zealand’s productivity performance had been lousy relative to those of other OECD countries, and countries with weak relative productivity performance should expect to experience a depreciating real exchange rate. On one telling, the weaker exchange rate helps offset the disadvantage of the lagging productivity. On another, given that tradables prices are set internationally, a country with a weak productivity growth performance will tend to have weaker (than other countries) non-tradables inflation. Another way of expressing the real exchange rate is the price of non-tradables relative to the (internationally set) price of tradables.

But over the last 15 years or so, we’ve seen something quite different. The real exchange rate isn’t trending downwards any longer. In fact, there has been a really sharp increase. Competitiveness, on this measure, has been severely impaired.

It is not as if, after all, productivity growth has suddenly accelerated in New Zealand relative to other advanced countries. We’ve done no better than hold our own against the median of the older advanced economies, and we’ve been achieving much less productivity growth than, say, the former communist eastern and central European OECD countries. But on this measure, the real exchange rate recently has been 40 per cent above the average level in the 1990s, and even higher than it was in the early 1970s.

But aren’t the terms of trade extraordinarily high too? Well, in fact, no. They’ve increased quite a lot in the last 15 years or so, but here is a chart showing the terms of trade back to 1914 (using the long-term historical research series on the SNZ website and, since 1987, official SNZ data).

Current levels aren’t much different from the average level for the quarter-century after World War Two.

On this OECD measure, the real exchange rate is higher than it was in the early 1970s (the previous peak in the terms of trade). But since then, productivity growth (real GDP per hour worked) is estimated to have been far less than the median advanced economy experienced over that period. In other words, the median OECD country (those 22 for which the OECD has data for the whole period) managed productivity growth of around 150 per cent over 1970 to 2015 (the most recent year for which there is data for all countries) and New Zealand managed productivity growth of only 75 per cent. It would take almost a 50 per cent increase in New Zealand’s productivity – all other countries showing no growth – to recover the relative position we had in 1970.

Competitiveness is a really major issue for the New Zealand economy. It isn’t so much of an issue for the firms that operate here now – they’ve survived and adapted. It is more about the firms that never started-up, or which started up and couldn’t make it, or which started, flourished and found that they could prosper rather better abroad. As trade shares (of GDP) shrink, in many respects this is a de-globalising economy.

Which made it rather odd to hear the (economist purporting to be the) “acting Governor” of the Reserve Bank declare that he, and the Bank, were comfortable with the level of the real exchange rate after the recent 5 per cent fall. He declared that the exchange rate was now close to “sustainable, fair value”. Taking a real economic perspective, it is anything but.

Such imbalances don’t have anything much to do with monetary policy, but they are symptoms of policy failures that need addressing urgently if we are to finally begin to turn around many decades – stretching back even 20 years before 1970 – of sustained economic underperformance.