There has been some silly nonsense published in various overseas publications about the change of government – all that on top of things like the Wall St Journal‘s weird pre-election suggestion that Jacinda Ardern was some sort of Trump-like figure.

I’ve written about some egregious examples of ill-informed commentary here. There was, for example, Nick Cater’s piece in The Australian praising the reformist nature of the previous government, the outperformance of the New Zealand economy, and specifically John Key and Bill English who “stand as inspiration to the rest of the developed world in these anxious and volatile time”. And then, more recently, there was the Washington Post column by an Auckland-based American lifestyle journalist who sought to convince his readers that the new government was controlled by the far-right. It was a case, we were told, of “Ardern may be the public face, it’s the far right pulling the strings and continuing to hold the nation hostage”.

Sure we are small and remote and not of that much objective significance to the rest of the world. But the scope for really badly-informed commentary is still a bit of a surprise: in both cases, it seemed, involving the authors projecting onto New Zealand what they wanted to see, and causes they themselves wanted to champion (in Cater’s case, genuine reform from the centre-right government in Australia, and in Ben Mack’s case probably a desire for something well to the radical-left of what any party in Parliament stands for).

Another example of detached-from-reality commentary turned up yesterday on Forbes magazine’s website, by an American investment adviser/commentator named Jared Dillian. I’d never heard of him before, but apparently he has a following in some circles, and is clearly willing to speak his mind. By the look of his new article on New Zealand, doing a little basic research first might help though.

His article has a moderate enough headline, New Zealand, An Economic Success Story, Loses its Way. In fact as a headline in 1960 it would have been spot-on. Without the constraints of magazine editors, his message was then amped-up when he tweeted out the link to the article, under the heading “New Zealand commits pointless economic suicide”.

I probably wouldn’t have bothered writing about it, but TVNZ asked me to go on this morning and comment on it, and preparing for that involved reflecting a bit more (than the piece really deserved) on where he was wrong and why.

I suspect the author must have been raised on some mythology about the 1980s reforms, which (rightly) got a fair amount of attention internationally then and for a decade or more afterwards.

There is the gross caricature of the pre-1980s New Zealand economy for a start (“most of industry was nationalized”, “extraordinary levels of government debt” [well, not much more than half – as a share of GDP – current debt levels in the US]). And then the claims about the subsequent period that are utterly detached from any sort of data: “New Zealand is a supply-side economic miracle”, “New Zealand enjoyed unprecedented economic growth”, “it became one of the richest countries in the world”.

All this in a country which over the last 30 years has had one of the lowest rates of productivity growth of any advanced country – none at all in the last five years – and which looks set to be overtaken by Turkey and such former communist states as the Czech Republic, Slovakia and Slovenia. We’ve just drifted slowly further behind most of the rest of the advanced world. Numbers of those leaving fluctuate cyclically, but over the post-reform decades we’ve had one of the largest cumulative outflows of our own people of any advanced country in modern times.

But what of the suicide note that Dillian appears to believe the new government’s policy agenda represents?

Top of his list is any changes to the Reserve Bank Act. He is, clearly, a big fan of the Reserve Bank and of New Zealand’s lead role in introducing inflation targeting. That’s fine, and reasonable people can differ on whether there is a strong case for change, and the extent to which possible changes (details yet unseen) might change substance (as distinct from appearance/style). But Dillian apparently knows already.

At 4.6%, unemployment is already low, but she wants to take it well below four percent, for starters. She would rather that the central bank tolerate higher levels of inflation in order to get unemployment lower, risking all that the RBNZ has achieved over the years.

A bit of basic research would have told him that the government has repeatedly indicated that they will not be seeking to give the Reserve Bank a numerical unemployment target, and that they recognise that other structural measures are needed if unemployment is going to be sustainably lowered very much further. And in his press conference a couple of weeks ago. Grant Spencer “acting Governor” of the Reserve Bank didn’t exactly seem to think the baby was about to get thrown out with the bathwater. If he did think so he could easily have said; after all he is retiring in four months’ time. And the Bank had one of their friendly foreign academics, on a retainer from the Bank, out making pretty reassuring noises the other day too. As he points out, the rhetoric from the government talks of modelling the Reserve Bank’s goals on those used in Australia and the United States – central banks which, mostly, behave much the same way our Reserve Bank does when it is following its current mandate.

It isn’t just goal changes that worry Mr Dillian.

She also wants to include an external committee in the RBNZ’s monetary policy decisions, which will certainly give the bank a more dovish tilt.

When central banks as diverse as those of the UK, Australia, Sweden, the United States, Israel and Norway include external members on their monetary policy decisionmaking committee, it is difficult to take seriously the suggestion that moving to such a committee will “certainly” make New Zealand monetary policy more “dovish”. What it may, perhaps, do is reduce the risk of the sort of false starts we’ve twice had to put up with from successive Governors this decade.

Then there is the forthcoming legislative ban on non-resident non-citizens buying existing residential properties.

New Zealand has, by anyone’s measure, one of the biggest housing bubbles in the world. Banning foreign ownership of property sets the country up for a possible real estate crash.

Set aside for the moment the question of whether the market is a “bubble” (I don’t think so, on any reasonable measure) but somehow adopting the same policy as Australia has had for years is suddenly going to fix our housing market problems. If only.

What of immigration?

Ardern also opposes high levels of immigration, along with her coalition partner, Winston Peters. It is set to drop dramatically. Immigration, especially skilled immigration, has been a big contributor to economic growth over the years.

Actually, the Labour Party policy, which will be the government’s immigration policy, does not change the number of non-citizens annually given the right to live here permanently by even one person: the target remains at 45000 per annum (or around thre times per capita the rate in the United States). Official policy supports continued high rates of immigration. On immigration, Winston Peters won nothing beyond the rather limited, one-off, changes that Labour has proposed.

But, yes, really rapid increases in the population, driven by net immigration numbers, have greatly boosted headline GDP over the last few years. Meanwhile, per capita real GDP growth – surely the metric that matters rather more – has been pretty anaemic at best. And – have I mentioned it before? – there has been no productivity growth at all in the last five years.

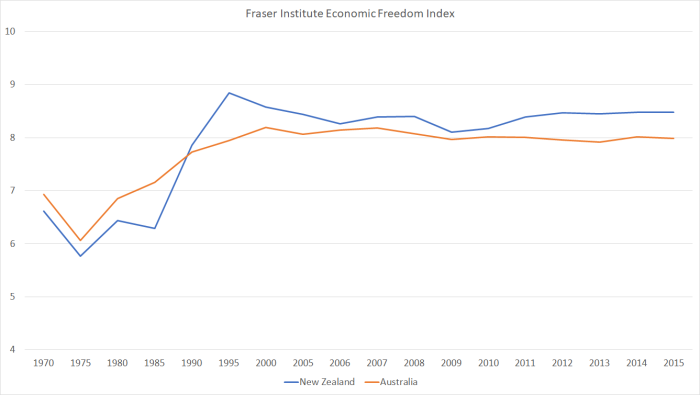

Dillian ends with two final predictions. Having heralded our high rankings on some of the economic freedom indices, he now asserts that “New Zealand will probably lose its status as one of the most open, free economies in the world”. Frankly, that seems pretty unlikely. As I’ve shown previously, on the measure he appears to cite our score has been pretty flat for 20 years now, through the ebbs and flows of the policy changes put in place by both National-led and Labour-led centrist governments.

Perhaps this government will prove different, but on the evidence to date – the published policy programmes – there isn’t much sign of it.

And what of Dillian’s final prediction?

It seems likely that New Zealand will experience a recession during Ardern’s term.

As it is now seven years (or eight, depending on how you count these things) since the end of the last recession, any detached observer would have to think there is a non-trivial chance of a recession in the next three years. Periods of expansion don’t typically die of exhaustion, but New Zealand has never gone 10 years without a recession of some sort or other (and although some Australians like to boast of their 25 year run, in fact even they have had an income recession in that time – a sharp correction in the terms of trade in 2008 for example). Our modern history is a small sample of events, but it wouldn’t be too surprising if something went wrong in the next few years.

Of course, most – but not all – of our recessions have had a significant international dimension to them. And that is still probably our greatest area of vulnerability in the next few years – some shock, or series of shocks, arising out of insufficiently-weighted (or priced) areas of vulnerability, accentuated by the fact that most other countries now have little room to use fiscal policy for counter-cyclical purposes and almost none to use monetary policy (most policy rates being very close to, or below, zero). When the next foreign recession hits it is going to be difficult for other countries’ authorities to respond effectively.

Could we mess things up ourselves? It is always possible – and monetary policy mistakes are among the possibilities – but even if you think the new government’s policy platform will reduce potential growth (or potential productivity growth) and even if there is some sort of “winter of discontent” fall in confidence next year, it is difficult to see what in the current mix of proposed domestic policies would tip New Zealand into recession. Lower headline GDP growth seems quite possible, but was also likely if the previous government had returned to office.

Dillian’s story seems to rest on the forthcoming “housing crash” and cuts to immigration. But if net migration is a lot lower in the next few years than it has been in the last few that is most likely to be because the Australian economy – our largest trading partner – is doing better. Policy itself is designed to maintain a high average net inflow of non-citizen migrants (and is the poorer for that). As for housing, unless/until land use laws are substantially liberalised, the idea of a crash in house prices is just a scary fairy tale – and were land use laws to be substantially liberalised, it would be more likely to be a force for good – including allowing some productivity gains – than one that would drag the economy down (tough as some of the redistributive consequences might be for some people). Among our good fortunes is that if demand does look like weakening materially, the Reserve Bank still has a fair amount of room to cut interest rates – not enough probably, but more than almost all other advanced countries.

All of which Mr Dillian could have found out with the slightest amount of digging. If there is a “suicide” dimension to economic policy in New Zealand, it is the wilful blindness of successive governments led by both main parties, who keep on doing much the same stuff, and either believe they’ll get a different and better (productivity) result, or who just don’t care much anymore.