I’m a bit tied up for the next couple of days, and so posting might be light and insubstantial My share in the stewardship of a financial entity that has now operated for decades without appropriate authorisations and approvals is somewhat time-consuming (thank goodness we have a Reserve Bank to deal with cases where major commercial banks don’t follow the rules).

But for today, I’m just going to leave you with a simple chart. presumably constructed by Moody’s from BIS data, that I found in a newsletter last night. It shows the change in the ratio of business and household debt to GDP between 2007 (just prior to the recession and financial crisis) and 2017 for 41 advanced and emerging countries.

In some quarters you hear a lot about high and rising debt in New Zealand. I’ve pointed out previously that the “rising” bit is mostly wrong – and that levels comparison across countries are difficult to do meaningfully, because of issues such as the tax treatment of debt. Despite the surge in house prices in the last few years, household debt as a share of GDP isn’t much higher now than it was in 2007.

What this chart highlights is that New Zealand is towards the end of the spectrum with the least increases in private debt as a share of GDP. Of these 41 countries, only five advanced economies and two emerging ones had less of an increase (more of a fall) than New Zealand.

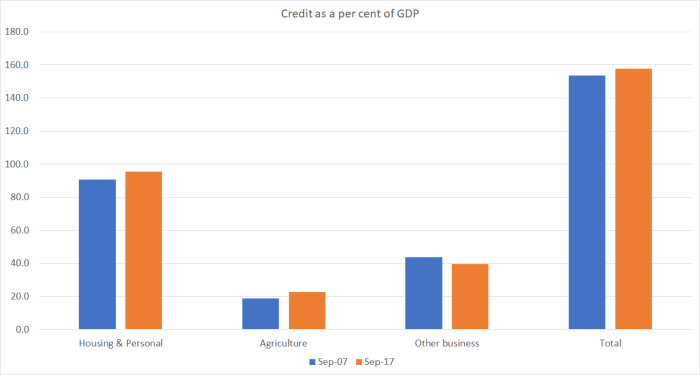

And here is a slightly more detailed chart on the specific New Zealand data, showing credit for each of the three sectors the Reserve Bank reports, as a share of GDP.

In the years leading up to 2007 we did, indeed, see a big increase in private sector indebtedness (as a share of GDP), across households, farms, and non-farm business. In the crisis-prediction literature it was a classic warning sign – taking on lots of new loans very quickly is often associated with a serious deterioration in credit standards. But it didn’t come to anything much, at least outside the (small) finance company sector.

Sure, we had a serious recession in 2008/09 – as most other countries did (it was largely a global phenomenon, with roots in the US in particular) – but our core financial sector came through the recession unscathed. Banks weren’t perfect by any means (they are run by humans in a world of imperfect information so that is hardly surprising) and of course there was some increase in loan losses and provisions. But nothing to threaten the soundness of any major institution or the system as a whole.

There probably are some serious questions to ask about what has gone on, and what might yet happen, in some of the countries in the chart that have had big recent increases in debt to GDP ratios – China most notably – but as was the case pre-2007, a big increase in debt is unlikely to be any sort of safe predictor of future financial sector problems.

And whatever the situation abroad, New Zealand at present doesn’t look like one of those places where anyone should be concerned about financial system risks. Yes, our house prices are cruelly high, but the structural policy failings that took them there don’t show any sign of being sustainably fixed. And there just hasn’t been much new debt taken out for other purposes.

All this is, of course, backed up by successive waves of stress tests undertaken by the Reserve Bank. Which does leave you wondering why we now have such a regulatorily-distorted and suppressed market in housing credit.