I’m a bit tied up for the next couple of days, and so posting might be light and insubstantial My share in the stewardship of a financial entity that has now operated for decades without appropriate authorisations and approvals is somewhat time-consuming (thank goodness we have a Reserve Bank to deal with cases where major commercial banks don’t follow the rules).

But for today, I’m just going to leave you with a simple chart. presumably constructed by Moody’s from BIS data, that I found in a newsletter last night. It shows the change in the ratio of business and household debt to GDP between 2007 (just prior to the recession and financial crisis) and 2017 for 41 advanced and emerging countries.

In some quarters you hear a lot about high and rising debt in New Zealand. I’ve pointed out previously that the “rising” bit is mostly wrong – and that levels comparison across countries are difficult to do meaningfully, because of issues such as the tax treatment of debt. Despite the surge in house prices in the last few years, household debt as a share of GDP isn’t much higher now than it was in 2007.

What this chart highlights is that New Zealand is towards the end of the spectrum with the least increases in private debt as a share of GDP. Of these 41 countries, only five advanced economies and two emerging ones had less of an increase (more of a fall) than New Zealand.

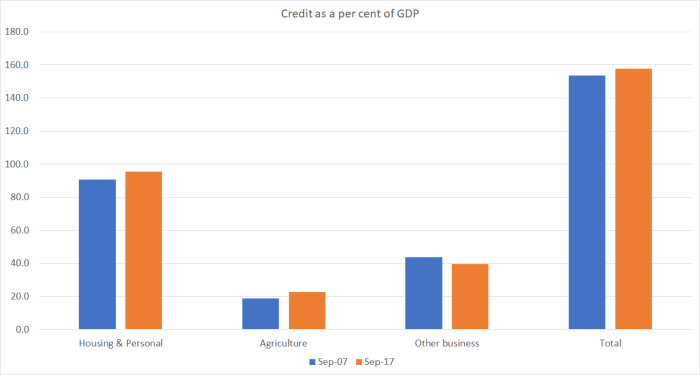

And here is a slightly more detailed chart on the specific New Zealand data, showing credit for each of the three sectors the Reserve Bank reports, as a share of GDP.

In the years leading up to 2007 we did, indeed, see a big increase in private sector indebtedness (as a share of GDP), across households, farms, and non-farm business. In the crisis-prediction literature it was a classic warning sign – taking on lots of new loans very quickly is often associated with a serious deterioration in credit standards. But it didn’t come to anything much, at least outside the (small) finance company sector.

Sure, we had a serious recession in 2008/09 – as most other countries did (it was largely a global phenomenon, with roots in the US in particular) – but our core financial sector came through the recession unscathed. Banks weren’t perfect by any means (they are run by humans in a world of imperfect information so that is hardly surprising) and of course there was some increase in loan losses and provisions. But nothing to threaten the soundness of any major institution or the system as a whole.

There probably are some serious questions to ask about what has gone on, and what might yet happen, in some of the countries in the chart that have had big recent increases in debt to GDP ratios – China most notably – but as was the case pre-2007, a big increase in debt is unlikely to be any sort of safe predictor of future financial sector problems.

And whatever the situation abroad, New Zealand at present doesn’t look like one of those places where anyone should be concerned about financial system risks. Yes, our house prices are cruelly high, but the structural policy failings that took them there don’t show any sign of being sustainably fixed. And there just hasn’t been much new debt taken out for other purposes.

All this is, of course, backed up by successive waves of stress tests undertaken by the Reserve Bank. Which does leave you wondering why we now have such a regulatorily-distorted and suppressed market in housing credit.

Pardon the ignorant laymen question but doesn’t household debt vary with some more concerning to the house owner and the economist than others? My lawyer explained with great relish the derivation of ‘mortgage’ as death grip as he clenched his fist.

My son has a 25 year mortgage on his home in France; he says his interest rate is about 2.5% and I expressed concern that interest rates could in the next 25 years return to what one of my bosses experienced with a house in Melbourne: 19%. He assured me that his loan had a fixed maximum of 4% over the entire 25 years. That sounds safe for him and assuming the French finance organisation is doing its job properly safe for France.

It is not the same for first time buyers in Auckland. If the housing asset declines in value sufficiently or the mortgage rate increases sufficiently the owners can just walk away and look for work in another country. The problem being house prices are linked; a severe price correction in Sydney and Melbourne would leave me concerned that my Aussie bank may crash – so my quiet life with safely small mortgage depends on the competence of the Australian bank regulators and their stress tests.

Interesting that household debt seems synonymous with mortgage; that has been my lifestyle choice but presumably many households have loans for cars, TV and credit card debt. But these debts are easier to resolve by belt tightening for a few months so should be less of a concern to economists and of course a sudden drop of say 50% in TV prices would not cause the dismay if/when the same occurs to house prices.

Thank you for the post; worrying about NZ indebtedness will never keep me awake again.

LikeLike

Back prior to 1990s, when interest rates hit the high 19%, land prices was part of the inflation index which then resulted in very high inflation and higher wages and of course higher consumption. Thats when Central Bankers decided around the world in their various G20 meetings since then to exclude land prices from the inflation index. Note that you cannot compare interest rates from that era prior to the 1990s because the fundamental drivers of inflation ie land prices are different today than back then.

LikeLike

I can and do compare interest rates – I had to make mortgage repayments in the 70’s and I am still doing so. When payment is due the under-lying economic factors driving interest rates are of no importance.

LikeLike

you have your history substantially wrong, altho it is true that land prices were in the NZ CPI. but remember that the systematic sustained upward pressure on real land prices really only dates back to the early-mid 1990s.

but real interest rate comparisons over long periods of time are certainly difficult to do with much confidence, for all sorts of measurement reasons (the US made changes a couple of decades ago that materially reduced the annual upward bias in the US CPI). nonetheless, i will say with confidence that real interest rates today are lower than those in 2007.

LikeLike

Not too sure why you would suggest my account of history is wrong because land prices as a component of house prices have been rising but from a low base the changes have not so very apparent once you try and chart a longer period of time as the doubling every 10 years rule of thumb, is a exponential curve and not a straight line. Of course there would be period of stagnant land prices and periods of high price inflation during that 10 years. David Chaston of Interest .co.nz did a study in May 2017 of the last 50 years house prices.

“Some readers have been looking for data on the ‘real’ change in house prices over a long time frame. Their thought is that this will show how different the current sharp run-up in nominal prices the recent data is from historical precedents.

But it doesn’t look like that is the case. Applying the inflation deflator and recalculating all prices to 2016 levels does smooth out some of the rise. But when you look at the annual change in real house prices, you find that current increases in fact seem quite ‘normal’ in New Zealand’s history.”

https://www.interest.co.nz/property/87961/adjusting-inflation-gains-house-prices-past-four-years-are-actually-nothing-special

LikeLike

Personal debt is quite small in NZ – about 6% of total household debt.

But, yes, the distributional issues are quite real and when the next recession comes – a more real threat than a large increase in interest rates, since the latter will happen only if the economy is doing well or inflating a lot – some will be very hard hit. But, of course, if you lose your job and can’t find another one, a mortgage of $150000 could tip you over the edge almost as surely as one of $600000.

Peace of mind doesn’t just depend on regulators and stress tests, but on banks. In Aus and NZ – with the exception a few torrid years post-deregulation in the late 80s – banks have been pretty prudently run (haven’t failed) since the crashes of the 1890s.

LikeLike

My instinct has always been and remains to distrust banks. I can trust a regulator – or at least I can go and punch him on the nose but banks seem to be uniquely impregnable.

The longer the time since the last failure the greater the chance they will be ignoring risks. I chose old boring reliable financial institutions and ended up with: Equitable Life and the Bank of Scotland. The former cost me and the latter was fortunately for me but not the UK taxpayer ‘too big to fail’.

What would happen in NZ if the big Australian banks crash? Are the NZ subsidiaries of the big Australian banks sufficiently independent? Maybe the first question implies a catastrophic failure in the Australian economy and could NZ survive that?

LikeLike

I have argued for some time now that our regulator, the RBNZ has been far too hawkish for at least the last 30 years. Its not about our distance or that we are only good enough to be farmers and shop attendants for the tourist industries as Michael persistently indicates.

It is about the lack of depth of our capital markets and the highly engineered and highly regulated financial credit industries that we have.

Our economists wrongly attribute the 61 Finance companies in 2007 to 2009 as due to mismanagement but those collapses has been more due to the engineered recession caused by the a very hawkish RB governor. As a result we now have the FMA who are even more draconian in regulating our access to credit even more so. The recent challenge by the RBNZ on Westpac is just another sign that our RBNZ regulator continue to act very aggressively on credit availability.

LikeLike

I’m sceptical that regulators can add much value when it is really needed. they didn’t help with HBOS or RBS, the irish banks and so on. They are well-intentioned (as most bankers are) but face many of the same knowledge problems bankers do.

And there are few punishments when they get thimgs wrong: Hector Sants, eg, was head of the FSA in 2007, and went on to be knighted and do stuff the great and the good do. Mervyn King retired with a peerage. And so on.

On your final paragraph, i went to an interesting seminar on exactly that sort of issue, which i will write about here next week.

LikeLike

…hmm; sector debt vs. sector income i.e. households pay debt with household income – a better metric?; per the May FSR: “…the household debt-to-disposable income ratio has increased to 167 percent, above its peak of 159 percent in 2009”; would seem credit remains both the oil and grit within the wheels of the NZ economic machine…

LikeLike

The problem with that metric is that it does not factor in overseas income. That makes that metric total nonsense. Garbage metrics equates to garbage outcomes.

First principle is that a bank will not lend you any money unless you can demonstrate an ability to repay interest and principle over a defined period. For Commercial debt that repayment period is usually 10 years. For Residential debt that repayment can be completed over a 30 year period.

LikeLike

…tend to think the first principle is a bank will lend you money when you least need it….

LikeLiked by 1 person

For example when a migrant comes from say the UK, usually they have existing assets ie their house in the UK. To sell that house would attract a CGT and are therefore discouraged from selling their UK property and instead rent it out. They then use the income from the rent of a fully paid up house as part of their income to borrow and buy another home in NZ. The UK rental income is not factored in the Disposable Income numbers as the migrant has a 4 year exemption as a new migrant. After 4 years who remembers to declare their UK incomes to IRD?

Another example would be say for example a chinese migrant like Deyi Shi who purchased Hotchkins mansion for $40 million. His NZ income is only $400k but the local banks have loaned him $20 million to purchase the house. Income to Debt metric already skewed badly by a single migrant. Why would a local bank loan Deyi Shi $20 million on a $400k local income? Because he has a billion dollar company in China with overseas income. What about the rest of the 1 million migrants we have in NZ?

LikeLike

QC, that comment “…tend to think the first principle is a bank will lend you money when you least need it….” is the problem with the NZ mental attitude towards growing opportunities. It has been drummed into us that debt is bad and that New Zealanders have too much debt. This same brainwashing occurs time and time again with our very hawkish RBNZ.

Second Principle is that Third party Equity is actually more expensive than debt.

There is nothing wrong with debt if used correctly. Without debt you would not see Graeme Hart building $200 million 116 metre yachts after successfully using $1.7 billion of debt and generating multiple billions of income and assets.

LikeLike

Of course if you borrow $3 million of Taxpayer money(ie our money and not hers to freely give away) and gift it to Manus island refugees of doubtful repute and I continue to walk past the same number of starving homeless people in Auckland sleeping on pavements each day, after all, Jacinda Ardern promised to take them off the streets before the election. It sort of disgusts me of her abusive waste of taxpayer money.

LikeLike

Peter Dutton, Minister for Immigration and Border Protection since 2014 during an interview yesterday said that if Ardern persists in her persistence then Australia will withdraw ALL privileges New Zealanders enjoy, and upgrade the requirement arrivals from NZ must apply for a Special Category Visa (subclass 444) (SCV) on arrival in Australia, subject to meeting certain health and character requirements. So to provide the humanitarian outreach to 150 people will cause great inconvenience to 500,000 New Zealanders each year, every year. This is a repeat of Helen Clark’s amnesty for 9000 overstayers which precipitated the withdrawal of welfare and support services to kiwis arriving in Australia post 2001

LikeLike

Not just irritating the Australia government but also every Papua New Guinean I know. It is the casual assumption that the people of Manus are uncivilised and are living in some kind of hell whereas it really is as close to the garden of Eden as you will find on this earth.

Our PM is acting like Queen Victoria’s Imperial Office deciding what is right and wrong for dark skinned foreigners in a distant land without consulting them first.

LikeLike

even those comparisons (household debt to HDI) have problems. among the many, when the govt is running surpluses the household sector has ultimate claim to those surpluses (which will be distributed in downturns.

for the whole economy, all debt is serviced by all income (for which GDP is a proxy). and since 2007 the ratio of GDP/GNI has fallen materially (as interest rates have fallen) so if I’d done the chart of debt to GNI we would have seen even less of an increase in the last decade.

LikeLike

Michael: more disingenuousness from RNZ

“Tourism has become the country’s top export earner, surpassing dairy and employing 7.5 percent of the New Zealand workforce. While the industry is booming, research into employment paints a less than rosy picture, with questions about whether the industry is doing enough to develop a work force for its future.”

[Pharoah: “it’s our largest pyramid!”]. The focus being on “the industry”

A tourism professor from AUT says his research shows real wages in tourism and hospitality have fallen 24.5% between 1976 and 2006.

http://www.radionz.co.nz/national/programmes/insight/audio/2018621157/insight-nz-s-tourism-workforce-imported-or-homegrown

LikeLike

17:20 “David Williamsonson says decisions made in the 1980’s to reduce the role of unions and changes in employment law have had long-term impacts.

…….

Ill go with Ian Harrison’s [simple] explanation

Click to access TheSuperdiversityMyth.pdf

Bob Jones says mass tourism destroyed travel. We have seen the “rich Americans” in the MtCookline bus and Japanese flying into or out of Mt Cook but those days have gone.

LikeLike

Amazing thoughts! I learned a lot from this article. Thanks for sharing and keep it up.

LikeLike