In last Friday’s Herald there was a weighty supplement headed “Dyanamic Business”, reporting/celebrating the results of the annual Deloitte Top 200 (companies that is) business awards. It seemed to be an opportunity for mutual self-congratulation, bonhomie, and a bit of virtue-signalling thrown in as well (eg the MBIE-sponsored award for “diversity and inclusion”). And a few oddities as well: the award for “excellence in governance” went to a company that is majority state-owned and subject to quite real moral hazard risks (see 2001), and I don’t suppose the Reserve Bank will have been best-pleased to see the chair of Westpac New Zealand Limited – the subsidiary just last week subject to Reserve Bank sanctions for failures of governance – as a runner-up the “Chairperson of the Year” stakes.

But what caught my eye flicking through the supplement was this table for the top 200 (non-financial) companies in New Zealand.

| Annual % growth 2016/17 | |

| Revenue | 4.3 |

| Pre-tax profits | -6.4 |

| Tax paid | 22.7 |

| EBITDA | 2.9 |

| Assets | -5.7 |

| Equity | 2.9 |

(Tax aside) those numbers didn’t look very impressive. Total revenue was up 4.3 per cent (and the accompanying article says that in the previous year revenue actually fell). Profits and total assets actually fell, and both EBITDA and total equity were up by 2.9 per cent.

And what happened to the whole economy? The Top 200 numbers use the latest audited accounts of each company, so there is a mix of balance dates. But in the year to June 2017 (the latest quarterly data we have), nominal GDP rose by 5.9 per cent. The last annual national accounts came out late last week: on those numbers, nominal GDP has risen 6.2 per cent in the year to March 2017, and 5.1 per cent in the year to March 2016. Against that backdrop, the performance of the top 200 companies was, if anything, surprisingly weak.

Big companies, in aggregate, doing less well than the economy as a whole needn’t be a concern. It could, after all, be a sign of thrusting new companies surging ahead and displacing the tired old giants. But there isn’t really much sign of that sort of process in at work in New Zealand – see, for example, the tech sector. And, of course, our overall per capita growth in real GDP (let alone productivity growth) has been pretty deeply underwhelming.

In a way, a simple list of the top 10 most profitable companies (dollar value of profits) is quite revealing:

| Fonterra |

| Spark |

| Air NZ |

| Ryman Health |

| Kaingaroa Forest |

| Auckland Airport |

| Transpower |

| Z Energy |

| Meridian Energy |

| Mercury |

Of those 10, we have four majority state-owned companies (one a natural monopoly), a chain of petrol stations, a property-boom play, and a co-op whose profits are largely driven by swings in global commodity prices. There wasn’t much new or very dynamic about it. In a way, the list of top 10 money-losing companies looks more interesting – in addition to Tasman Steel (No 1) and Kiwirail (No 2), it does feature Xero and Orion Health.

It is a very different list than, say, one of the top most profitable non-financials in the US, which does feature (relative) newcomers like Apple and Alphabet (Google) and where almost all the companies have a strong international focus.

I mentioned those new annual national accounts numbers. No doubt I’ll be using the numbers in various posts in the next couple of months, but for now just a couple of charts.

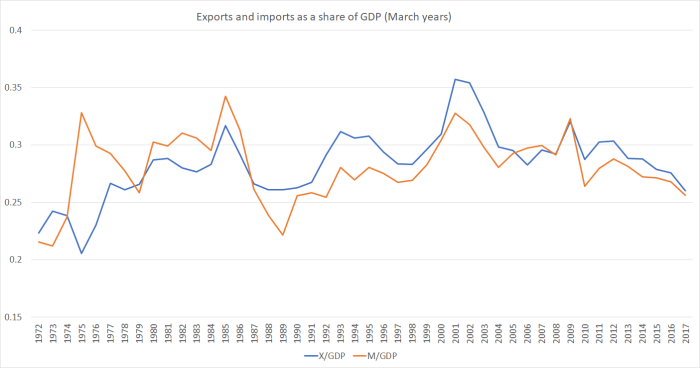

I’ve noted in various recent posts the fall in the export share of GDP over recent years. There was always the hope that some of that might have been revised away when the annual numbers were published. But no.

As a share of GDP, imports haven’t been lower since the depths of the recession in the year to March 1992. Exports haven’t been lower, as a share of GDP, since the year to March 1976 – more than 40 years ago. There was, so it was claimed, a policy focus on increasing the outward orientation of the New Zealand economy. If so, it failed.

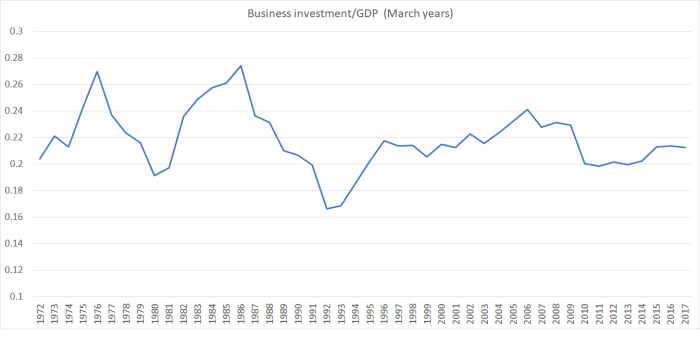

And what of business investment as a share of GDP (as previously, this is total gross fixed capital formation less government and residential investment)?

It picked up a couple of years ago from recession-era lows, but has gone sideways since, and is nowhere the rates reached in the previous expansion.

When profit growth in our top 200 companies has been relatively subdued perhaps it shouldn’t be surprising that not very much business investment is occurring. And those export/import numbers shown earlier strongly suggest that what business investment is occurring will have been disproportionately concentrated in the non-tradables bits of the economy, those that don’t (be definition) face much international competition.

Deloittes and the Herald might think this is a “dynamic economy” – and I’m sure there are plenty of small exciting firms in it – but once we stand back and look at the aggregate numbers the picture isn’t very encouraging at all. If change is constant, the change here seems – in aggregate – to more akin to drifting slowly backwards.

That was the legacy of the now-departed National-led government. That government’s policies were not, in relevant areas, materially different than those of the previous Labour-led government. The worry now is whether there is any realistic basis for expecting something different, and better, from the new centre-left government. At present, it isn’t obvious why the future should be any better than the performance over the last 20 years or so.