In my post yesterday, buried well down amid long and fairly geeky material, I showed this chart.

Using official SNZ data, it suggests that over the last 15 years or so nominal wage rates in New Zealand have risen materially faster than the income-generating capacity of the New Zealand economy (nominal GDP per hour worked – a measure that takes account of the terms of trade). Since a big part of what New Zealand firms are selling when they try to compete internationally is (the fruits of) New Zealand labour, it probably shouldn’t be too surprising that our tradables sector producers have been struggling. As a reminder, we’ve had no growth in (a proxy measures of) real tradables sector GDP since around 2000 – two whole governments ago.

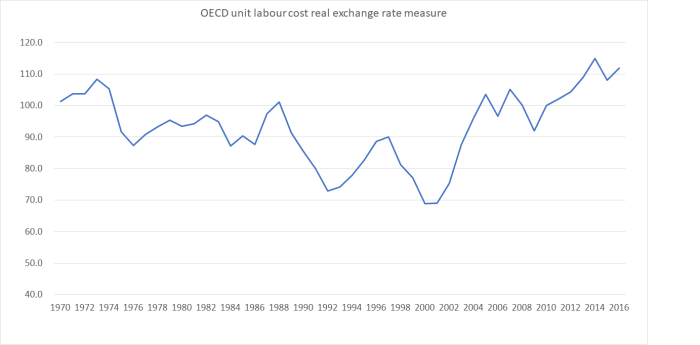

The OECD publishes a real exchange series, all the way back to 1970, using real unit labour cost data. Unit labour costs are, in effect, wages adjusted for productivity growth. The real exchange rate measures compares how our economy has done on this competitiveness measure.

(There are other real exchange rate measures in which the fine details are less stark, but the picture is very similar.)

Broadly speaking, our real exchange rate was trending gradually downwards for the first 30 years of the series. And each trough was a bit lower than the one before it. That was, more or less, what one might have expected. New Zealand’s productivity performance had been lousy relative to those of other OECD countries, and countries with weak relative productivity performance should expect to experience a depreciating real exchange rate. On one telling, the weaker exchange rate helps offset the disadvantage of the lagging productivity. On another, given that tradables prices are set internationally, a country with a weak productivity growth performance will tend to have weaker (than other countries) non-tradables inflation. Another way of expressing the real exchange rate is the price of non-tradables relative to the (internationally set) price of tradables.

But over the last 15 years or so, we’ve seen something quite different. The real exchange rate isn’t trending downwards any longer. In fact, there has been a really sharp increase. Competitiveness, on this measure, has been severely impaired.

It is not as if, after all, productivity growth has suddenly accelerated in New Zealand relative to other advanced countries. We’ve done no better than hold our own against the median of the older advanced economies, and we’ve been achieving much less productivity growth than, say, the former communist eastern and central European OECD countries. But on this measure, the real exchange rate recently has been 40 per cent above the average level in the 1990s, and even higher than it was in the early 1970s.

But aren’t the terms of trade extraordinarily high too? Well, in fact, no. They’ve increased quite a lot in the last 15 years or so, but here is a chart showing the terms of trade back to 1914 (using the long-term historical research series on the SNZ website and, since 1987, official SNZ data).

Current levels aren’t much different from the average level for the quarter-century after World War Two.

On this OECD measure, the real exchange rate is higher than it was in the early 1970s (the previous peak in the terms of trade). But since then, productivity growth (real GDP per hour worked) is estimated to have been far less than the median advanced economy experienced over that period. In other words, the median OECD country (those 22 for which the OECD has data for the whole period) managed productivity growth of around 150 per cent over 1970 to 2015 (the most recent year for which there is data for all countries) and New Zealand managed productivity growth of only 75 per cent. It would take almost a 50 per cent increase in New Zealand’s productivity – all other countries showing no growth – to recover the relative position we had in 1970.

Competitiveness is a really major issue for the New Zealand economy. It isn’t so much of an issue for the firms that operate here now – they’ve survived and adapted. It is more about the firms that never started-up, or which started up and couldn’t make it, or which started, flourished and found that they could prosper rather better abroad. As trade shares (of GDP) shrink, in many respects this is a de-globalising economy.

Which made it rather odd to hear the (economist purporting to be the) “acting Governor” of the Reserve Bank declare that he, and the Bank, were comfortable with the level of the real exchange rate after the recent 5 per cent fall. He declared that the exchange rate was now close to “sustainable, fair value”. Taking a real economic perspective, it is anything but.

Such imbalances don’t have anything much to do with monetary policy, but they are symptoms of policy failures that need addressing urgently if we are to finally begin to turn around many decades – stretching back even 20 years before 1970 – of sustained economic underperformance.

The NZ Herald now calls Grant Spencer the Governor of the RBNZ!

LikeLike

Channelling his own press statement no doubt. In a way it is a small thing, but even if the appointment was lawful it would still be inappropriate. I’m pretty sure Kelvin Davis is only ever referred to as “acting Prime Minister”.

When Rod Carr was (lawfully) acting Governor in 2002, he was always and only ever referred to as “acting Governor”, including in his own press statements.

LikeLike

Surely the continued arrival of cash from new residents and foreign buyers of real estate is keeping the exchange rate much higher than is justified on tradeables. What happens when that capital decides to flee to a new home?

LikeLike

The NZD is the 10th most traded currency in the world after China and really nothing to do with new residents and foreign buyers. Global speculation of the NZD drives the upwards and downwards sentiment. Interest Yields and a stable store of value provides fundamental support for the NZD.

LikeLiked by 1 person

New Zealand’s annual GDP is around $350 billion

Turnover in the $NZD is $105 billion per day – 80% of that is conducted overnight in the City of London

LikeLike

Actually, our annual GDP is around NZ$250 bn

LikeLike

By comparison in NZ Traded interest rate swaps (inverse bond prices) the notional value of the bonds

daily value is NZD 5,891,990,000

weekly value is NZD38,038,982,400

YTD value is NZD 1,231,285,857,397

LikeLike

I suspect those particular numbers aren’t very large (most immigrants don’t have much to bring, and the foreign purchases – unknown magnitude – were probably only a big issue for a couple of years). My argument is that it is the people themselves (or rather the policy that solicits them) that give rise to the pressure: each new person puts a lot of pressure on domestic resources, because the new (physical) capital requirements of each new person are so much greater than a year’s output. And we have new big waves of arrivals every year, so the pressures never ease for long.

LikeLike

An argument that has zero correlation studies. $500 million gets traded every single day. The GDP of New Zealand is only a tiny $250 billion a year. There is nothing our entire population can do to influence the NZD iin any of its upwards or downwards momentum. It is purely global speculators in the NZD.

LikeLiked by 1 person

Actually, there is plenty of correlation – the exch rate tends to be high when net inward migration is strong – but correlation isn’t causation, and my argument doesn’t rest on those cyclical effects.

When you argue that it is “purely global speculators”, you need to think about what drives their interest in NZ. as you noted in an earlier comment, much of that is NZ interest rates. Those are set, over time, by NZ real economic forces, and population/immigration is one of those. How large an impact that particularly variable has is, of course, debated.

LikeLike

Nz interest rates are driven by the RBNZ and the monopoly that our banks have. RBNZ I believe sets a. Requirement for banks to have a percentage of loans against local savings. As a result credit becomes limited by the RBNZ as they adjust those settings to curb lending. Any scarce resource like limited savings puts upward pressure on interest rates.

The banks also use their monopoly position to maximise profits. Australian bankhave a massive installed client base which means most of their profits come from grooming their large installed client base. Interest rates need to sit higher in order to manage the lag time between when interest rates should fall for their installed client base and when they have to compete for new business.

Interest rates have been falling as immigration has been rising in the last several decades as your 700 years interest rates charts show that the general interest rates trend has been downwards. Therefore it is not population growth that drives interest rates around the world and in NZ.

LikeLike

…that first chart begs the question: why are mangers/shareholders handing out pay rises despite evidence that productivity is lacking?

LikeLike

Managers and shareholders are guided by profitability and ultimately dividend returns to shareholders determine performance. Frankly no one looks at productivity in business. If manual labour is cheaper then a business will use manual labour. If it gets too expensive they will then look at investment in technology. I have been into the May road New World supermarket since it opened 4 years ago. It was fully staffed by people at the checkout counters. In fact they had pretty much 2 people a checkout station. As the minimum wage rose, the 2nd person that packed disappeared and a we started to see self checkout counters introduced. As the push for the next round of pay increases. The supermarket in the last few weeks have increased self checkout counters and reduced the number of staff checkout.

I suspect when that $20 minimum wage comes in there will not be any more staff checkout counters. I don’t think the Labour Party is doing labourers any favours. Productivity is increasing but at a cost to the rest of the domestic economy. Self checkout counters do not eat, do not spend and do not need entertainment.

LikeLike

As I believe in human labour rather than economists utopian robotic productivity, I am one of those people that would refuse to clean up after a meal at MacDonalds or Burgerking. I won’t use the self checkout counters and will queue up longer if necessary. I also refuse to shop at Kmart that is pretty much 98% self checkout counters and I will also queue up at the banks teller to bank a cheque.

LikeLike

because the demand for often quite labour-intensive activity in the non-tradables sector is there. firms in the non-tradables sectors (in aggregate) have pricing power that tradables firms don’t have. And tradables firms then just have to “meet the market”, and as a result their relative significance is our economy has been shrinking.

(the relationship between wage growth and productivity growth is an equilibrating tendency across the whole economy, not something any employer can do much about. the public service is the extreme example – there aren’t many productivity gains in policy analysis/advice, but if an employer in the public sector wants decent staff, they have to meet what the market would pay those sorts of people in alternative roles/firms. [and, to be clear, as the data in yesterday’s post shows, wage inflation has been led from the private sector in the last decade, not the public sector])

LikeLike

….hmm; it seems odd that demand is “there” in part due to a material number of domestic facing firms effectively generating said deman via wage settlements that contribute to higher unit costs; in many ways, the description of NZ wage history, REER trend and sectoral imbalances rings a bell located in Southern Europe before the crisis – and that is a tad perplexing…!

LikeLike

I think Michael & Getgreatstuff both have valid points.

1) The fundamental underlying cause is the high demand for capital due to NZ high immigration rate

2) NZ economy is small so speculation in the NZD/interest rates/swaps etc reinforces the trend & also we, as a small economy, pay a premium over (mainly) Aussie rates for transactions (with Aussie dictated by US rates)

Further lesser effects

3) If I remember correctly government in NZ is a large part of the economy. One could argue this is dead weight cost to productivity. We need the income redistribution vis government but do we need the 1st world regulations and bureaucracy when NZ is verging on 2nd world status.

4) We have a reasonably efficient agricultural sector already so marginal productive gains will be low (unless we adopt Netherlands style farming). Agriculture provides the majority of the products NZ makes.

5) The tax wedge on savings (eg tax on term deposits) increases the real interest rate demanded

6) High demand via immigration drives domestic demand for non tradable services. With high demand and near monopoly positions for some of these services the non tradable inflation runs much higher than tradable inflation. RBNZ has to respond to the combination of both leaving short term interest rates higher than ideal.

LikeLike

There is correlation between high immigration and NZ misallocation of capital. The misallocation is mainly due to misallocation to primary production ie farming. For example. It takes an investment in 10 million cows, significant land resources, food resources and water resources to generate an export GDP of $15 billion. A company like Samsung heavily subsidised by the Korean government generates a sales turnover of $300 billion with 275k employees. Now that is what people can achieve versus what cows can achieve.

LikeLike

Correction: There is NO correlation between High immigration and NZ misallocation of resources.

LikeLike

What part of high immigration drives domestic demand?

The 15k gross migrant visa arrivals each year of which we do not have the numbers that depart or the 125k international students spending $4.5 billion in GDP?

Or is it the 3.7 million tourists that need to eat, sleep, be entertained and spend up big to the tune of $11 billion a year?

LikeLike

The other part of the immigration equation is of course foreign workers. Top of the list of the most highly skilled migrants last year was chefs and front desk managers which brings up Winston Peters charade of low skilled rip off. But the reality is that every one of those Visas are only issued by a business that pays wages. Of course you have the odd immigration scam but underlying that is the 3.7 million tourists and the 125,000 international students that need to eat, sleep and and be entertained spending $15 billion in the economy.

LikeLike