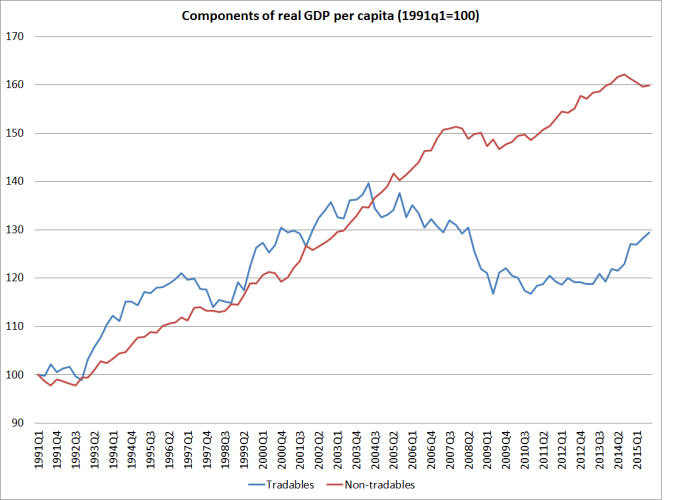

In a post on Thursday I showed this chart, a rough and ready decomposition (pioneered by the IMF) of real GDP per capita into that produced by tradables sectors (bits exposed to competition from the rest of the world) and non-tradables sectors. My proposition was that successful high-performing economies will usually be led by strong tradables sector growth.

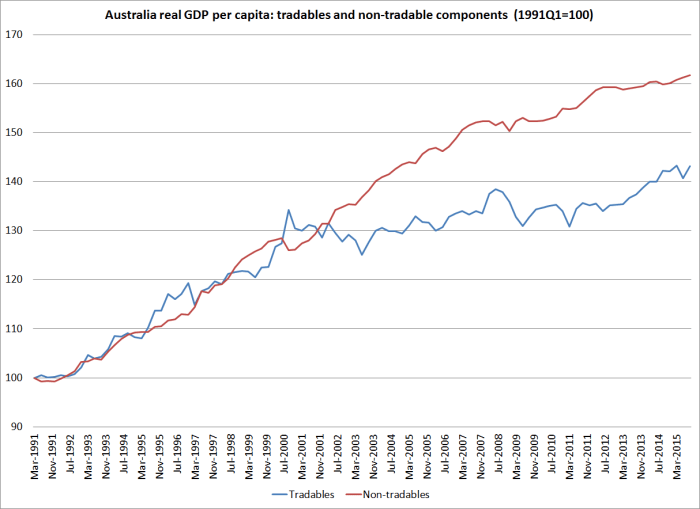

I was curious about how the comparable chart would look for Australia.

Total growth in non-tradables per capita has been almost identical in the two countries over these 25 years (around a 60 per cent increase).

But look at the differences in recent years in (this proxy for) tradables sector output, per capita.

In New Zealand, (this proxy for) tradables sector output per capita hasn’t increased over 15 years (notwithstanding the strong last few quarters). In Australia – which certainly isn’t a stellar economy – the picture is much less negative.

At a sub-sectoral level, manufacturing output in Australia (per capita) has been even weaker than in New Zealand over the full quarter century. The big difference, of course, is simply the rapid growth in mining output.

Changing tack, just briefly…

Some readers perhaps find this blog a fairly unremitting critique of the Reserve Bank of New Zealand. But today I’m sticking up for them.

Independent economist Shamubeel Eaqub has a column in today’s Dominion-Post, which in the hard copy version runs under the heading “Gorging a warm-up act for debt horror show”. And “gorging” is Eaqub’s word, not just some sub-editors hype. According to Eaqub, all New Zealand’s debt chickens are about to come home to roost – notwithstanding, apparently, the fact that debt/GDP ratios are little changed over the last eght or nine years, and that no one has any good sense of what a sustainable, optimal, or equilibrium level of such ratios might be.

But according to Eaqub

The Reserve Bank is complicit, as they regulate banks. They say that the banking sector is not at risk. Their modelling shows sufficient capital buffers – which influence banks’ risk appetite to lend and vulnerability in a recession.

Their modelling has also shown higher inflation and interest rates for the last seven years – mistakenly.

It’s time the Reserve Bank better regulated banks to stop the repeating cycle of debt gorging and economic vulnerability.

This is really just a “guilt by association” slur. Yes, the Reserve Bank has got its inflation and interest rate forecasts badly and repeatedly wrong, but what possible connection does that have to the question of whether banks hold adequate capital (whether risk weights, or required capital ratios)? Or whether the stress test results are plausible? Eaqub produces precisely no evidence to support his insinuations. It is a short column to be sure, but surely he could at least offer readers a hint.

Lets recall that the stress tests involved a 40 per cent fall in house prices across the country, and something like a 50 per cent fall in Auckland. And they involved an increase in the unemployment rate larger than any seen in any advanced economy with a floating exchange rate since World War Two. And the banks still looked pretty resilient.

And as the IMF has previously noted, when they looked at a variety of other countries, risk weights on housing lending in New Zealand were materially higher than those in other countries.

I suspect there are tough times ahead for the New Zealand and world economy. One can always argue for more capital, but to do so from the current situation – where New Zealand banks are better-capitalized than most – one really needs more than simply the claim that “they got monetary policy wrong, so we shouldn’t give them credence on any other score”.

I would be very wary of Shamubeel Eaqup’s comments, he has for the last decade encouraged renting as a better option financially than buying your own home. He has ended up having to rely on his mommy’s equity if he now wants to buy a house in Auckland.

Like many economists he has failed to look at the savings, the investments, the equity and the assets of New Zealanders and have merely focused on one side of the balance sheet, the debt. And with a trillion in assets and $120 billion in debt, New Zealanders debt is actually far too low. House prices can withstand a 40% stress test so it is not housing value that is the issue. If house prices are rising then demand has exceeded supply, time to build. Developers can only build if the price exceeds the costs so you do need higher prices or you need lower costs ie falling interest rates and more cheaper imported building products and cheaper imported labour.

When a bank fails, it is not debt that causes the failure, it is the promises it makes, eg the derivative market. Derivitives are off balance sheet and it is based on promises, I promised to lend you x amount and in turn a bank uses that promise to promise another bank and earns a margin based on the premise of promises. Therefore when a bank collapses there is a chain reaction as the chain of promises is broken and delivery is uncertain. Is this stress tested? What is our banks exposure to other countries derivatives?

NZ banks problems which is not stressed tested is the level of savings in banks. Savings cannot be allowed to get ahead of debt because savings in banks impair a banks balance sheet, Debt is an asset on banks books. It is when interest rates rises that is when bank stability risks rises.

These days bank runs on savings is unlikely, quite different from 1929 where bank runs on savings resulted in bank collapses which in turn forces a bank to foreclose on debt impairing asset values and putting people wholesale out on streets. That’s why we have deposit guarantees and a banks assets and liabilities are frozen and that’s why OBR is a very important tool.

LikeLike

It is when interest rates rises, that results in more and more savings in bank accounts which results in impairment of the banks net assets as savings deposits are a liability on the banks books. Too much savings impairs the net asset position of a banks balance sheet and the higher interest paid on savings impair margin and leads to lack of profitability. That is the reason why a bank with an army of risk managers panic and we saw that panic when banks started to offer low documentation loans and 100% finance LVR products when Allan Bollard started to push interest rates to 9%.

LikeLike

I was wondering about the definition of the tradables sector.

In particular, I wondered about including/excluding mining, agriculture etc. I accept they meet the criteria, but perhaps the criteria could be fine tuned. My thinking is that something like mining iron ore in a globally competitive manner mainly depends on being able to find a big enough body of iron ore to extract. For smaller miners it is a more akin to globally competitive industry because their margins are lower, so they need to compete harder.

There is another element to this, and that relates to the demand/supply and prices in these industries. In the mining/dairy boom the likes of the miners and dairy industry got paid a lot more than now, but as businesses they weren’t really any “better”.

A third point, I believe that most dairy markets are very internally focused, with relatively small amounts exported/imported, apart from NZ. I wonder if this qualifies as being exposed to global competition? Partially exposed yes, but fully exposed?

Anyway, given my comments above, I just wonder what your graphs would look like if agriculture and mining were excluded from tradables? And whether they could give us any further insights into the make up of Aus/NZ GDP growth?

LikeLike

Interesting points LIndley

Re dairy, yes most dairy is consumed in the country it is produced in, and there are often restrictions of various sorts. But from NZ’s perspective, dairy is most definitely tradables – we have to find our way in a world with various restrictions and subsidies. Bear in mind too that the EU is one of the world’s biggest dairy exporters, and the US has also been emerging as a major exporter.

Re mining, yes discovering a huge lode is no guarantee of higher productivity – but it is probably a path to greater wealth and higher consumption in the medium term (eg Norway or Australia). Note that productivity levels in Australia are not enormously high – ok by OECD stds ( better than NZ, but not great). I’d argue that Australia is, like NZ, materially penalized by location/distance, with the great good fortune to have found, and been able to exploit, those huge mineral resources. (They’d probably be better off per capita if they’d not had so much immigration – but it matters less for them than for us, because they are so much further up the OECD league tables.

As I noted, manufacturing sector performance in Aus over 25 years has been even weaker than in NZ. Services exports have been similar. The real difference, among these tradable sectors, has been mining.

LikeLike

If NZ house prices fell 40%, “stress” would no doubt be high! And to my mind, that remains a problem with bank stress test exercises – how does one attempt to predict the true reaction of people to such a material development and the unknowable knock on effects? The banking system relies on ‘confidence’ / ‘trust’ as much as it does on quantitative analysis of hypothetical risk events. Whether a 40% decline in house prices would cause a funding strain on our banking system is anyone’s guess but as I read once, ‘it makes no sense to start a bank run but complete sense to join one’……not sure how you model that!

LikeLike

Yes, funding risks are a matter for a separate test. Offshore funding remains the main vulnerability. I was thinking of writing something on that later in the week.

Just bear in mind the unemployment component of that test – it is incredibly demanding, and it has to happen for banks to realise really big losses on residential mortgage books. It did in Ireland – but they had a fixed exchange rate, and fixed exchange rates make a lot of difference

LikeLike