The Wall Street Journal ran an article yesterday by Jon Hilsenrath about this week’s (widely-expected) increase in the Federal funds rate target. So extraordinary have the times been that many Americans will have gone almost a quarter of their working life and never experienced an increase in official interest rates.

Hilsenrath is generally regarded as a well-briefed journalist, and writes intelligently about the Federal Reserve and related issues. This article seems to have two separate points to it. The first is the suggestion that Federal Reserve officials themselves are worried that “they’ll end up right back at zero”. And the second is a report of a new WSJ poll of economists about the outlook for the Fed funds target rate over the next five years.

Taking the poll first, 58 per cent of the surveyed economists reportedly expect that the Fed funds target rate will be back at zero in the next five years, and 16 per cent think the target will have been taken negative.

58 per cent seemed, if anything, a surprisingly low percentage, and not telling us very much. After all, most policy rate cycles seem to have been only around five to seven years. In the US, the Fed started raising rates in February 1994 and was back where it started by September 2001. And then it started raising rates in June 2004 and was back where it started by October 2008.

In Australia, the RBA started raising rates in August 1994 and was back to the same level by September 2001. It started again in November 2003, and was back where it started by December 2008, and the rate cycle that started in October 2009 was unwound by December 2012.

And what about New Zealand (abstracting from the very quickly reversed small cycles)?

Start End

March 1994 November 1998

November 1999 November 2001

January 2004 December 2008

In New Zealand we never quite got to a cycle even as long as five years. So if I was ever asked, and without looking at a single piece of data, I’d say there was always a pretty good chance that policy rate tightening cycles would be fully unwound within five years.

Some will argue that the current US position is different, in that it is starting from such a low rate. Perhaps, but the Fed funds target was 1 per cent before the previous cycle got underway. Neutral rates seem to have been declining around the world, and there is little sign that the US is an exception to that. And on the other hand, as the WSJ article notes, the US recovery has now been underway for six years, so it is a long way into the recovery (weak as it has been) for the tightening cycle to be starting.

So if Fed officials had only this sort of five year horizon in mind in worrying about the possibility of reversal, it probably shouldn’t be newsworthy. Shocks will inevitably happen, and there is a good chance that even if a tightening is warranted now, it won’t be needed in several years’ time.

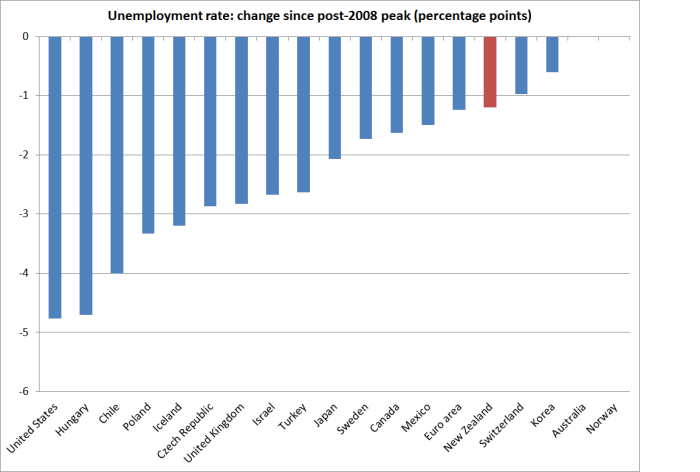

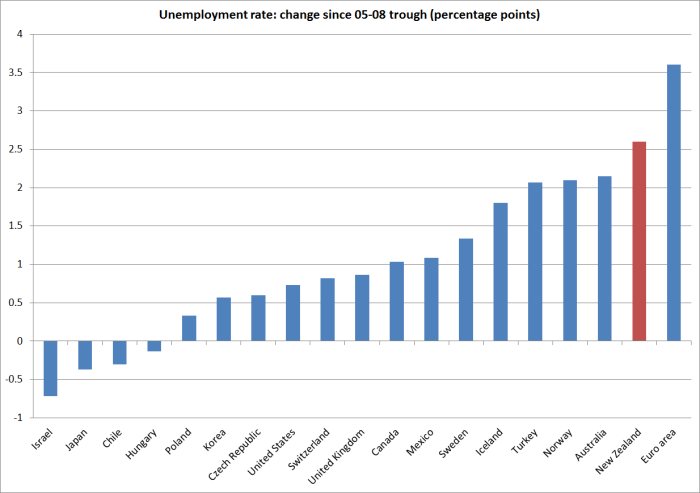

But it would be more newsworthy if some significant chunk of the FOMC were worried that the US might experience the sort of policy reversal all too many advanced countries have had in the last few years. The WSJ article lists a number of policy reversals in the period since the 2008/09 recession , including that of the ECB and those of smaller countries such as Sweden and Israel. Mercifully, and perhaps reflecting the extent to which New Zealand has dropped under the radar in recent years, they don’t highlight New Zealand – the only advanced country to have had two quick policy reversals since 2008/09. I wrote about the various policy reversals a few months ago (here and here).

All too many central banks have misjudged the extent of the inflationary pressures in their economies, tightening before the evidence was in that inflation was really increasing. Acting pre-emptively probably made sense in the early post-recession period – forecast-based policy has, after all, been the mantra. But it has become harder to justify as the years went by, and inflation continued to remain surprisingly weak (at any given interest rate) in most countries. In New Zealand, forecast-based policies have probably ended up increasing the variability of interest rates.

Perhaps the US is different, and they really will be able to sustain not just a single Fed funds rate increase but a succession of them (of the sort apparently envisaged by many FOMC members in the dot chart). But it isn’t clear to me why the US should be different. It has been a pretty anaemic recovery, and if the unemployment rate has fallen a long way, the employment rate is still very subdued. And the real exchange rate has risen a lot. It isn’t that high by historical standards, but a 15 per cent increase in the real exchange rate over the last 18 months or so makes a difference even in a country where exports are only 14 per cent of GDP (tradables are a much larger share).

In this climate, I’d have thought that the inflation numbers themselves should be a key guide. But even there, there is little obvious reason to think higher interest rates are warranted. The Fed chooses to target inflation as measured by the deflator for personal consumption expenditure (PCE) – as distinct from the CPI. Headline annual PCE inflation is 0.2 per cent (those weak petrol prices, which affect US inflation more than NZ inflation, because taxes are a much lower share of petrol prices). PCE inflation excluding food and energy has been 1.3 per cent over the last year – an inflation rate unchanged now for many months. And the trimmed mean PCE inflation rate has also been steady, at 1.7 per cent. The Fed’s chosen target is 2 per cent inflation. Perhaps one could argue that inflation is not too far from the target, especially if one chose to emphasis the trimmed mean measure, but it is not getting any closer. Given the state of knowledge, and the precedents from other countries, it seems quite likely to be premature to act now.

Which raises the question of why are they (apparently) moving now? Perhaps the majority of the FOMC is just falling into the same trap other central banks (including the Reserve Bank) have done, expecting a resurgence of inflation (even though there is little or no sign of it yet). Perhaps it is the low unemployment rate? But is it not plausible that the NAIRU could be moving lower again? Former senior Fed official Vince Reinhart has an interesting commentary out, in which he suggests that part of the motivation for a move now might be a desire by Janet Yellen to establish credibility as someone sufficiently tough and willing to move, that she can afford to make the case later for moving only very gradually. Perhaps there is something to that story, but I hope not. My impression is that central bankers usually play things fairly straight, reacting to the data as they read it (whether reading it correctly or otherwise) because any other approach is a dangerous game. Of course, American politics is different, and there is a lot of suspicion of the Fed on the right. But in an anaemic recovery, when so many other central bankers have tightened and then had to reverse themselves, and in a global economy where the threats seem to be growing rather than dissipating, and where (for example) commodity prices are moving ever lower, adopting a strategy that might jeopardise the US recovery out of some desire to “establish credentials” would seem particularly inappropriate. Within the terms of their own articulation of their mandate, there is little sign that the Fed has had monetary policy too loose in the last seven years – Scott Sumner and others make a reasonable argument that they were too slow to ease at the start – and no sign that monetary policy is too loose now. None of us might adequately understand why interest rates are as low as they are, but that isn’t a basis for a central bank to try to end that on the basis of not much more than a mental model that “in a sensible well-functioning economy, interest rates really should be higher than they are now”.

And all that is before the growing signs of renewed financial fragility and risk. I found this chart that I saw in a newsletter yesterday somewhat sobering.