J.B Condliffe was one of the greater New Zealand economists of the first half (or so) of the 20th century. One evening earlier in the week I was dipping into his New Zealand in the Making, an economic history of New Zealand, the second edition of which was published in 1959. On the first page, I noted this line

“Today New Zealand claims the largest overseas trade per head of any country in the world”

Those were the days when the story was often told about about how exposed to foreign trade New Zealand was. Protectionists wanted to reduce that exposure. In the 1950s, global trade as a share of GDP was much lower than it is today. Even New Zealand’s trade share was a little lower than it is now (services exports were not material in those days, and merchandise exports were around 27 per cent of GDP). Our export share of GDP was about that high even though New Zealand had very heavy industry protection in place, promoting domestic manufacturing. That acted as a tax on exports, reducing both exports and imports below what they would otherwise have been.

The late 1950s were also the days when New Zealand still had among the highest per capita incomes in the world. In the mid- late 1950s, Maddison estimates that New Zealand incomes were behind only those in the United States and Switzerland. Whatever the “true” number, we were still in the top tier of material living standards

How do things compare today on foreign trade?

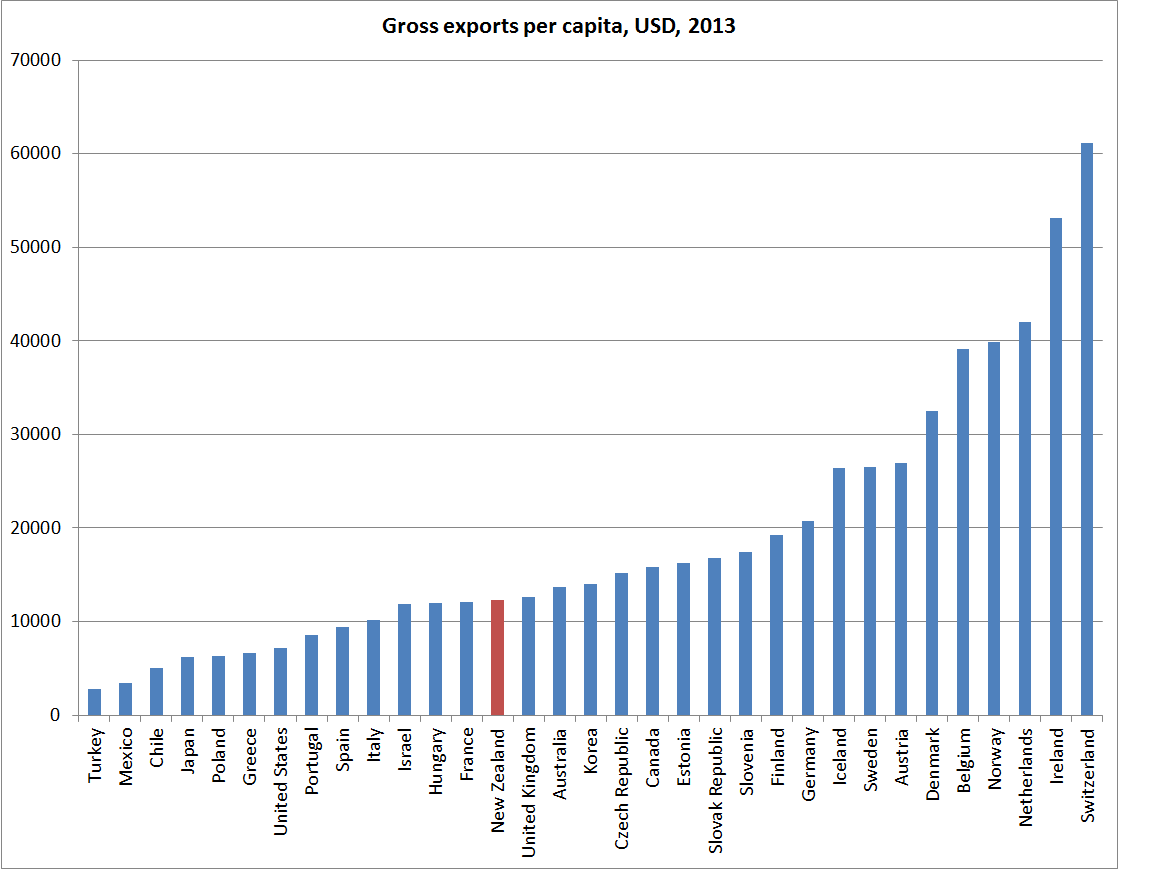

I dug out the OECD data for total exports per capita (for 2013) and converted them into a common currency. Here is the chart.

New Zealand is in the bottom half of this chart.

Big countries tend to export less than small countries – fewer firms need to tap the wider world when there is already a large market at home – and distant countries tend to export less than countries that are close to lots of other markets. Firms in the United States, for example, export a lot less per capita than firms in (similarly well-off) Switzerland does.

Whatever the situation in the 1950s, it would have been a little surprising if we had been in the top tier of the 2013 chart. One of the big changes in international trade since the 1950s has been the rise, particularly in manufacturing, of “global value chains”, where different stages of production occur in different countries. In other words, a car finished in Germany and exported to France might include a substantial proportion of components produced in (and exported from) a range of Eastern European countries. And some other products exported from, say, Slovakia will use lots of components imported from Germany. The value of a country’s gross exports rises with this (typically mutually beneficial) activity, but the share of a country’s total value-added (which GDP is capturing) resulting from exports might not have risen much at all. For New Zealand, a long way away, this sort of trade doesn’t happen in the way that it might between say Austria and the Czech Republic.

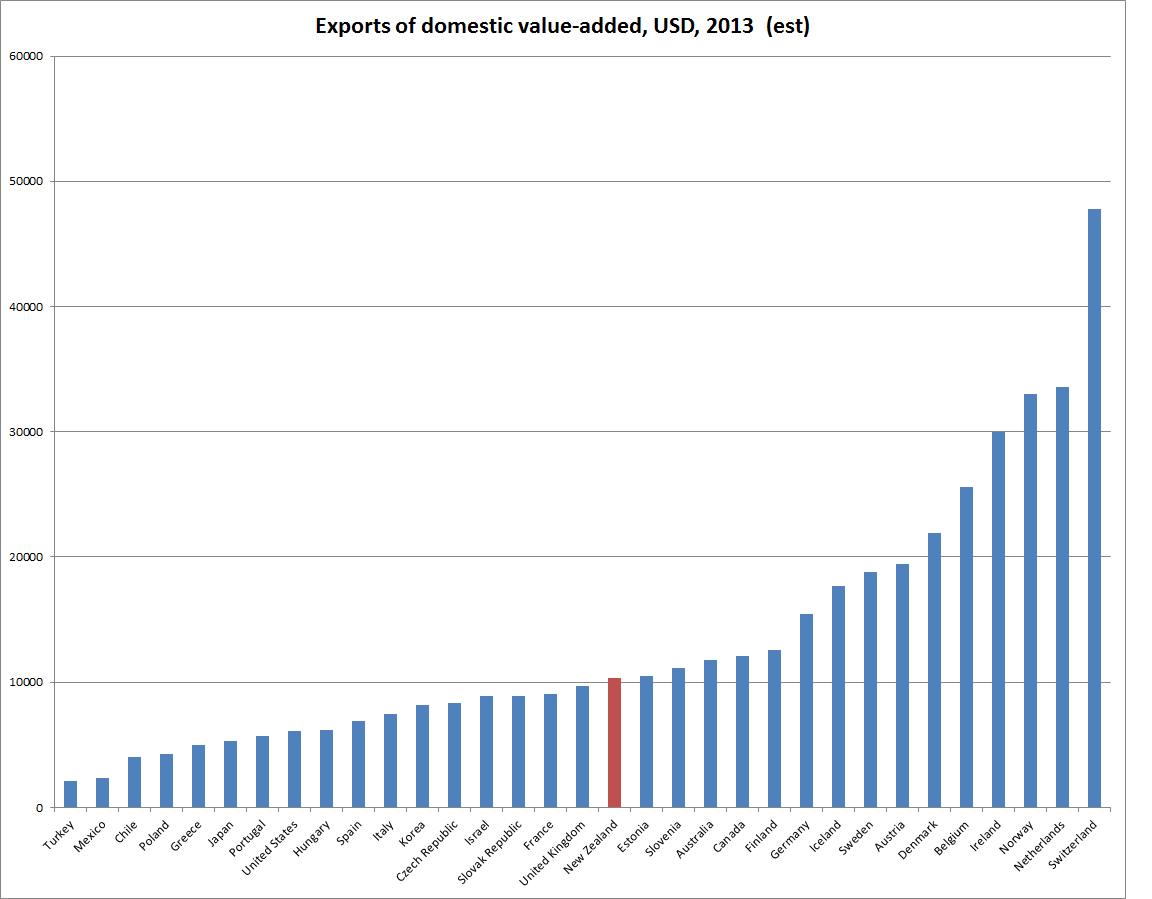

The OECD and WTO have recently done the work of trying to trace what proportion of each country’s exports are domestic value-added. The latest data are for 2011, but the domestic value-added shares don’t fluctuate much from year to year (production patterns don’t change that fast). Applying the 2011 data on the share of exports that reflect domestic value-added to the 2013 exports data, we get a chart of per capita exports of domestic value-added.

Here, New Zealand shows up just above the middle of the pack, but with a level of exports per capita (near the peak of a terms of trade boom) that was only a third to a quarter of the exports of domestic value-added from the Netherlands and Switzerland.

It is a far cry from the 1950s position of the largest overseas trade per head. And, of course, today we languish in the bottom third of OECD countries for GDP per capita.

There is always a danger of seeming to come across as suggesting that exports are either good for their own sake, or are the only possible route to prosperity. We export (or sell anything) to support present and future consumption, and for an individual or a firm it makes no particular difference whether goods or services are sold to domestic or foreign purchasers. But at a whole economy level, the export underperformance nonetheless remains a disconcerting indicator. We can’t remedy New Zealand’s underperformance just by exporting more – Mao was exporting grain during the great famine, and we’ve had export subsidies in the past ourselves – but successful economies tend to be those with increasing numbers of the products that the wider world wants to buy more of, at prices that encourage further innovation and investment. Many individual firms have done well, but in aggregate New Zealand doesn’t seem to have been in that position.

What has gone wrong? I’ve argued that our real exchange rate has been out of line with the productivity fundamentals for decades. Excess domestic demand has driven up the price of non-tradables relative to tradables, skewing investment and activity away from the tradables and export sector. Part of that story – a significant part in my view – has been the active large scale inward migration programme, which has diverted resources away from global markets to (what successive governments have instead made) their most profitable use; meeting the physical capital (houses, road, factories, shops, offices etc) needs of a population that has continued to grow quite rapidly. The only time since World War Two when our governments pulled back from actively pushing up the population was from the mid 1970s to the late 1980s, and in that period we messed things up in other ways – the Think Big debacle, a post-deregulation credit and property boom and bust, and of course a very weak terms of trade.

I’ve commented previously on the government’s peculiar exports target. There is no chance of meeting that target on any sort of sustainable basis, without changing the factors that give rise to the persistently higher real interest rates and the high real exchange rate.

Agreed, you cannot run monetary policy in isolation to what the rest of the world is doing. The RB is far too inward looking and ignores the massive QE that is occurring around the world and the currency fixing/manipulation that led China to super power status.

LikeLike

Interesting for when I suggested some weeks back that the job of the RBNZ should be about wealth creation you didn’t seem to agree, but it seems that is the underlying suggestion here.

Of course that also requires the govt. to get its act together as well.

Interesting also on a day when a thoughtful analysis of Fonterra was in the paper this morning.

Stephen Franks has commented ( On his Blog),on the aggressive politics that caused the formation of an inherently flawed Fonterra. He has a lawyers view of the process of the formation of a company that processes raw material and never mind the market.

Keith Woodwood from Massey has a better view of the problem, a lack of clear strategy.

This is the problem that applies to NZ. Unlike Singapore we have no national strategy to be anything so our world revolves around politics of the biased, politics of the churches and Maori politics and politics of compromise..

One fails to see this changing. We can’t even create a sense of purpose by having a flag that represents NZer’s with apparently anything but a sports marketing symbol. Tells us lots about ourselves.

LikeLike

Singapore would be one of the earliest economies that moved away from traditional monetary policy economics with boom and bust cycles to a more guided continuos growth economics. Rather than moving interest rates up and down that created massive volatility in the business environment, Singapore adopted a high compulsory superannuation policy to control spending and consumer inflation rather than the traditional monetary policy. At its peak boom periods, Singapore employer contribution was a staggering 15.7% together with an employee contribution of 15.3% whilst its interest rate policy maintained a lower than global average interest rate policy. Currrent super policy is 8% employer and 8% employee contribution when the GFC hit global markets.

I would attribute Singapores success to the adoption of a variable superannuation policy that enriched their individual citizens compared to the wealth sapping of high interest rates on businesses that NZ adopts.

LikeLike

Unfortunately, Maori has played an excellent end game and have invaded every political party in NZ. If you examine each major political closely Maori interest is very well represented in Labour, in National, in the Greens, in NZfirst, in the Maori party and also would have strong representation even if Kim Dotcom did not crash and burn.

LikeLike

and here I was congratulating myself on having gone a day without mentioning the RB on this blog! The Rb has a limited impact on the real exchange rate in the short-term, but the sort of real exchange rate misalignment that worries me is a real phenomenon, not one mon pol (or anything RBish) can do anything about.

PS I thought the Baldwin and Franks pieces were both well worth reading.

LikeLike

That was my initial thoughts about the RB being of no serious consequence but when you look at the 90 day bank bill rate and when the pattern is so closely matched with the OCR it is clear that the RB has a massive influence on interest setting policies by NZ banks and international swap markets.

LikeLike

Ha, well not much between RBNZ and Govt. policy at the best of times and there’s the rub.

until Govt. decides what NZ Inc should be doing they have no idea what to get the RBNZ to do to encourage those goals.

Called the Catholic Compromise.

Easter trading is a shinning example. My God have the Catholics stormed out about Holly days that our ever increasing ethnic population really isn’t into and when they have their own days we ignore that.

LikeLike

Unfortunately we have a MMP system which means the government must pander to the whims of the minority groups. However the RB was given independent powers which means we have to try and ensure we do have a awfully brilliant RB governor otherwise we are going to have a real difficult financial future.

LikeLike

I think you overstate the importance/influence of the RB Governor (even if I think he – if not the institution – has too much power). Once in a while a great Governor will come along, but mostly we’ll have to be content – as in most other areas of CEO-dom – with an average person. Doesn’t mean we shouldn’t aim for the best, but we need a system that is resilient to the average (and occasional well below average) person as Governor.

LikeLike