The NZIER this morning released the results of its Shadow Board exercise. They survey nine people (currently three market economists, three business people, and three with academic affiliations) and ask them to assign probabilities for the “most appropriate level of the OCR for the economy”. In principle, I suppose “the most appropriate level for the economy” could be different from “the most appropriate level to be consistent with the requirements of the Policy Targets Agreement”, although I suspect that respondents will typically be treating the two as the same. Note that, in principle, the information in the Shadow Board responses is different from the information in financial market prices (which are close to a direct view on what the Reserve Bank will do – as distinct from what people think it should do) or from ipredict, which runs direct contracts allowing people to bet anonymously on what they think the Reserve Bank will do. When I looked just now, the prices reflected an 84 per cent chance of a 25 basis point cut tomorrow

Launching the Shadow Board was a modest but useful initiative by NZIER. It helps spark a little more debate, and a little more scrutiny, about what the Reserve Bank is doing, and puts the results in a useable (and reportable) format. It was inspired by a similar exercise in Australia (which is slightly more (too?) ambitious in that it also asks respondents for probabilities for the right rate six and twelve months ahead).

But what the Shadow Board doesn’t really do is provide any additional information on what the Reserve Bank should do. As everyone recognises, there is a great deal of uncertainty around monetary policy. Central banks talk of trying to target inflation a couple of years out, and yet have no great certainty even as to what is going on right now, let alone what will be going on 12-18 months hence.

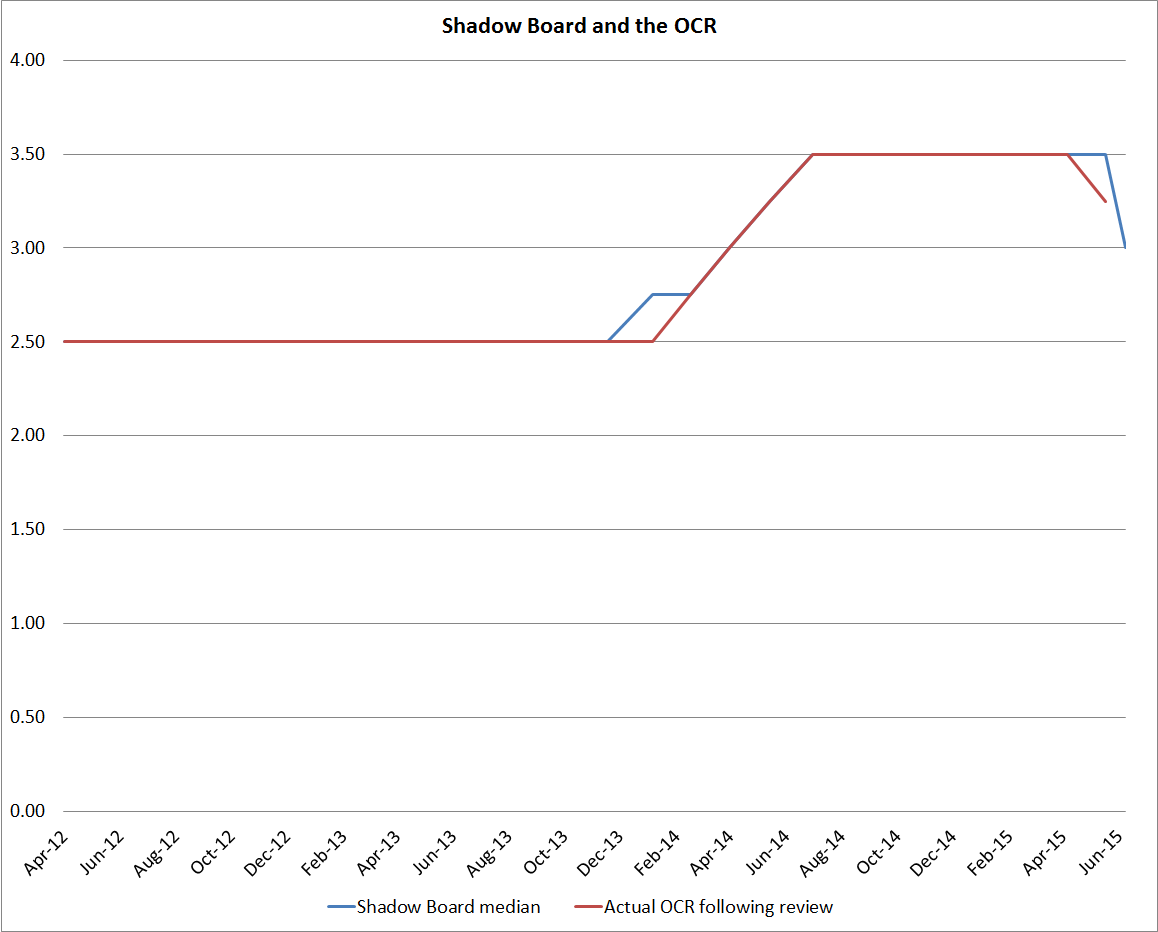

Here is a chart showing the actual OCR following the relevant review and the median view of the Shadow Board (thanks to Kirdan Lees at NZIER for sending me the historical data).

They are all but identical, at least over this relatively short period. And yet the Reserve Bank has subsequently acknowledged that, with the benefit of hindsight they would have had the OCR lower in 2011 and 2012. And most observers would now agree that the OCR did not need to have been as high as it was over the last year.

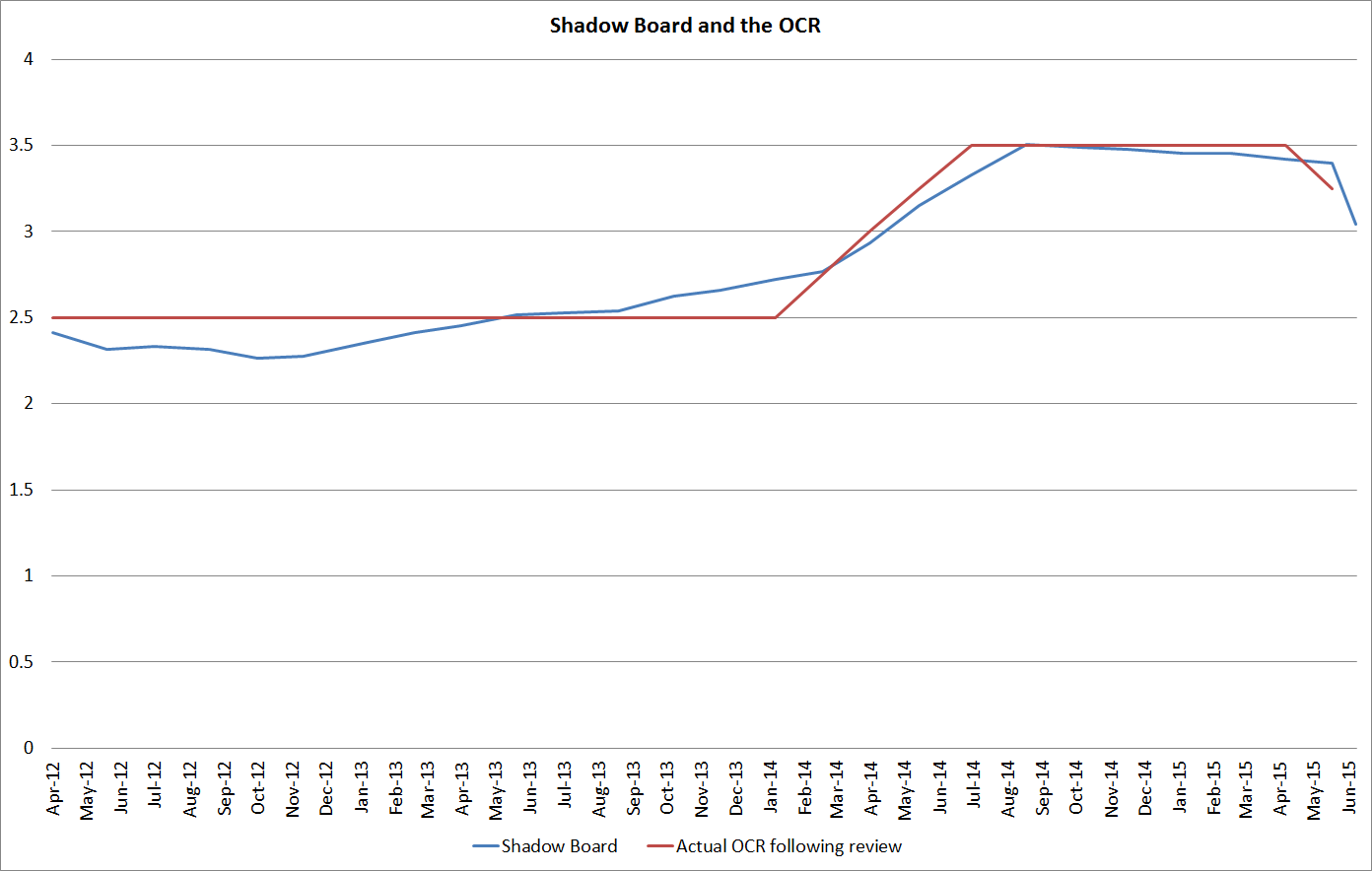

Perhaps the information is in the distribution of probabilities rather than in the median view? Here is the mean of the views of the Shadow Board members. It does deviate a little from the actual OCR, and perhaps during last year the Shadow Board’s views were a little more cautious than the Reserve Bank was. The Shadow Board’s mean view was a little below the actual OCR, while the Reserve Bank itself was still stressing upside risks and the probable need for further rate increases.

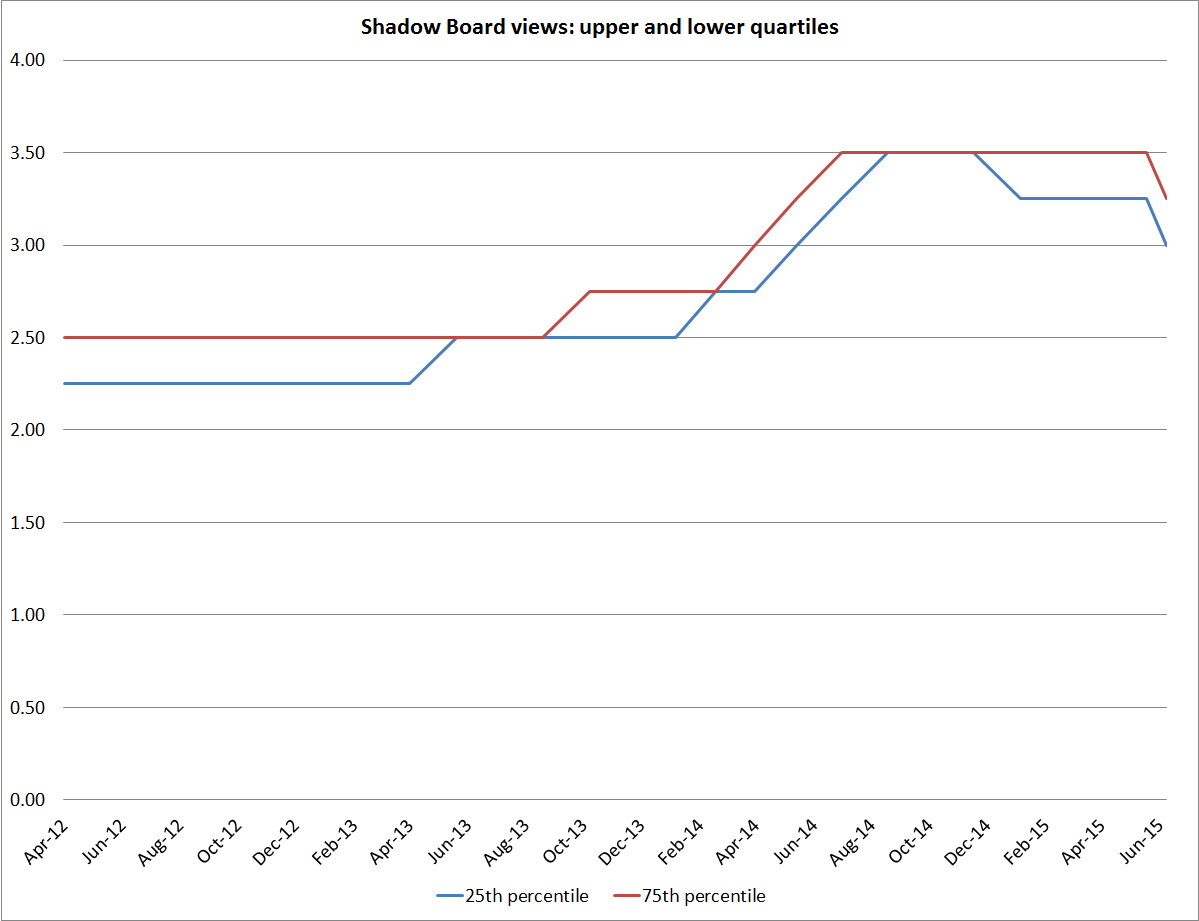

And here are the 25th and 75th percentiles. Respondents collectively put at least a 25 per cent chance on something at or below the 25th percentile being appropriate, and at least a 25 per cent chance on something at or above the 75th percentile.

It is striking just how tight these ranges are. I noted back in June that most individual respondents’ views seemed excessively tightly bunched, given the huge historical uncertainty about the appropriate OCR. This time around there is a little more dispersion. The Shadow Board exercise has now been running for 27 reviews, and this is one of only three in which respondents collectively put a less than 50 per cent weight on one particular OCR (the other two were January last year, when the Reserve Bank was just about to commence raising the OCR, July last year which proved to be the last of the OCR increases). I doubt, if I’d been assigning my own probabilities, if I would ever have put even a 40 per cent weight on any particular OCR in any particular review.

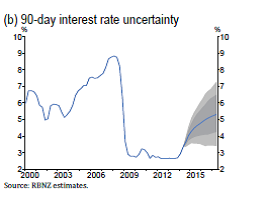

One other way of looking at the scale of the uncertainty around the OCR is the fan charts that the Reserve Bank published in the June MPS last year. These were somewhat controversial, and are hedged around with lots of caveats in the technical notes, but the Governor presumably regarded them as a sufficiently useful device to run prominently in the main policy analysis chapter of a Monetary Policy Statement. On the subset of shocks and uncertainties considered in that exercise, the 90 per cent confidence interval for the 90 day rate (proxy for the OCR) two years ahead was some 400 points wide. Perhaps a little embarrassingly for the Bank, that range did not even encompass an OCR of 3 per cent or less by July 2015.

What do I take from all this? I’d probably make only two points:

- There is a huge amount of uncertainty in running discretionary monetary policy. Some would argue that it is a mug’s game and only likely to introduce additional volatility. That isn’t my view, but the uncertainty (across a range of different dimensions) is large enough that in general everyone should be a little cautious in taking a stand on a particular OCR (of course, under the current regime, the Reserve Bank must take a view, in actually setting the OCR). Mistakes won’t be uncommon – whether by commentators or central banks – and that should be recognised, with appropriate humility, by all involved. Of course, Reserve Bank mistakes matter more because they are charged with the power to take decisions that affects all of us in one way or another.

- That very uncertainty highlights just how important it is that there is robust debate around a range of perspectives. In this post, I haven’t looked at the diversity in the individual respondents’ views (partly because the panel of respondents has kept changing, and the sample is quite short), but looking through that data there hasn’t been much diversity of view across respondents either (with the creditable exception earlier in the period of Shamubeel Eaqub). It is very easy for consensus views to form – both within the Reserve Bank – and in the wider New Zealand debate more generally. And yet those consensus views will often be wrong. Sometimes those looking at New Zealand from the outside have had a better take on things, but I doubt that has been consistently true (in the last year, HSBC in Sydney has been running the “rockstar economy” story, while other offshore players were rather more sceptical of the Reserve Bank’s continuing tightening cycle). Encouraging that diversity of perspective is particularly important within the Reserve Bank, and yet it can be hard to maintain. That is probably true in all central banks, but is a particular risk in our system, in which the Bank’s chief executive controls resources and rewards and is also single monetary policy decision-maker. A very good single decision-maker would probably want as much debate and challenge as possible, recognising just how uncertain the game is. A less-good one would find it too easy to discourage debate and challenge – while never explicitly saying so, or perhaps even meaning to – preferring material that supports the decision-maker’s own priors and predilections.

great article with plenty to think about

I have a lot of sympathy for Central Banks post GFC.

It is much harder to know exactly what to do.

Ironically I think it is harder for those Central Banks where rates are not at the zero bound level.

Glen Stevens here in Australia has uttered that he would prefer not go get near that level and has wondered publicly about how potent monetary policy is as interest rates get lower and lower.

LikeLike

I’d suggest the longer rates are at zero the more potent monetary policy becomes… but only in one direction!

Would be interesting to see some educated comment on how NZ would fare if the OCR was reduced to levels significantly closer to what is on offer from the US or Germany. Lower NZD would help our exporters but would we have any issue with funding?

LikeLike

Interesting question, but I think the answer is likely to be “no” (and, in addition, at a much lower exchange rate the fx amount of offshore funding banks would need to raise would be much lower anyway (the assets they need to fund are all in NZD). Of course, if we got to zero because of rising concerns about our banking system it might be a different matter, but at present the RB’s stress tests suggest the banks can cope with some pretty severe adverse shocks.

Note that banks had no particularly difficulty funding in 2000 when our short rates were last around US levels.

LikeLike

Thanks Michael, yes fewer USD to raise due to FX movement – although still significantly more than were needed in 2000 I suppose.

LikeLike

Well the 16th July tender for Sep 2035 inflation linked bonds came in at 2.23%, down 37bp in the past six weeks. Implies inflation expectations falling fast & real rates may not be falling at all.

LikeLike

Other way round surely? The IIB yield is a real rate – and if anything IIB yields look to fallen a bit further than nominal yields in the last month suggesting a modest rise in implied inflation expectations

LikeLike

Now I’m confused. If the policy rate is cut but is still above the Wicksellian rate, wouldn’t you expect the real yield to fall?

LikeLike

Sorry, I’m a bit lost.

The IIB curve suggests the market thinks a neutral real rate is around 2.5% (max) – the implied 10 year forward rates in 10 years time is about 2.5%, and one might reasonably subtract a bit of a term premium. Long-term inflation expectations might be anywhere in a 1.7 to 2% range (between surveys and market-implied rates. On that basis, the OCR is below the Wicksellian rate, and (presumably goes a little lower tomorrow).

LikeLike

Ah, my error.

LikeLike