The BNZ’s Raiko Shareef has a research note out looking at the impact of including the Chinese yuan in the Reserve Bank’s trade-weighted index measure of the exchange rate. He argues that the inclusion of the CNY will increase the sensitivity of New Zealand’s monetary policy to developments in China.

I think he is incorrect about that. China has, of course, become a much more important share of the world economy in the last couple of decades. It has also become a much more important trading partner for New Zealand. Both of those developments, but particularly the former, mean that economic developments in China, including changes in the value of China’s currency, have more important implications for New Zealand, and other countries, than they would have done earlier. The Reserve Bank recognised the importance of the rise of China in setting monetary policy, and assessing developments in the exchange rate. But the Bank was quite slow to include the CNY in the official TWI measure. There was a variety of reasons for that, some more persuasive than others. But as far back as 2007 the Bank started publishing supplementary indices that included the CNY. If the Reserve Bank had used the old TWI in some mechanical way, then perhaps it would have been misled, and perhaps there would have been policy implications from the change in weighting schemes, But not even in the brief bad old days of the Monetary Conditions Index was the TWI used mechanically for more than a few weeks at a time. Every forecast round, the Bank comes back and goes through all the data, not just a reduced-form equation feeding off a particular TWI.

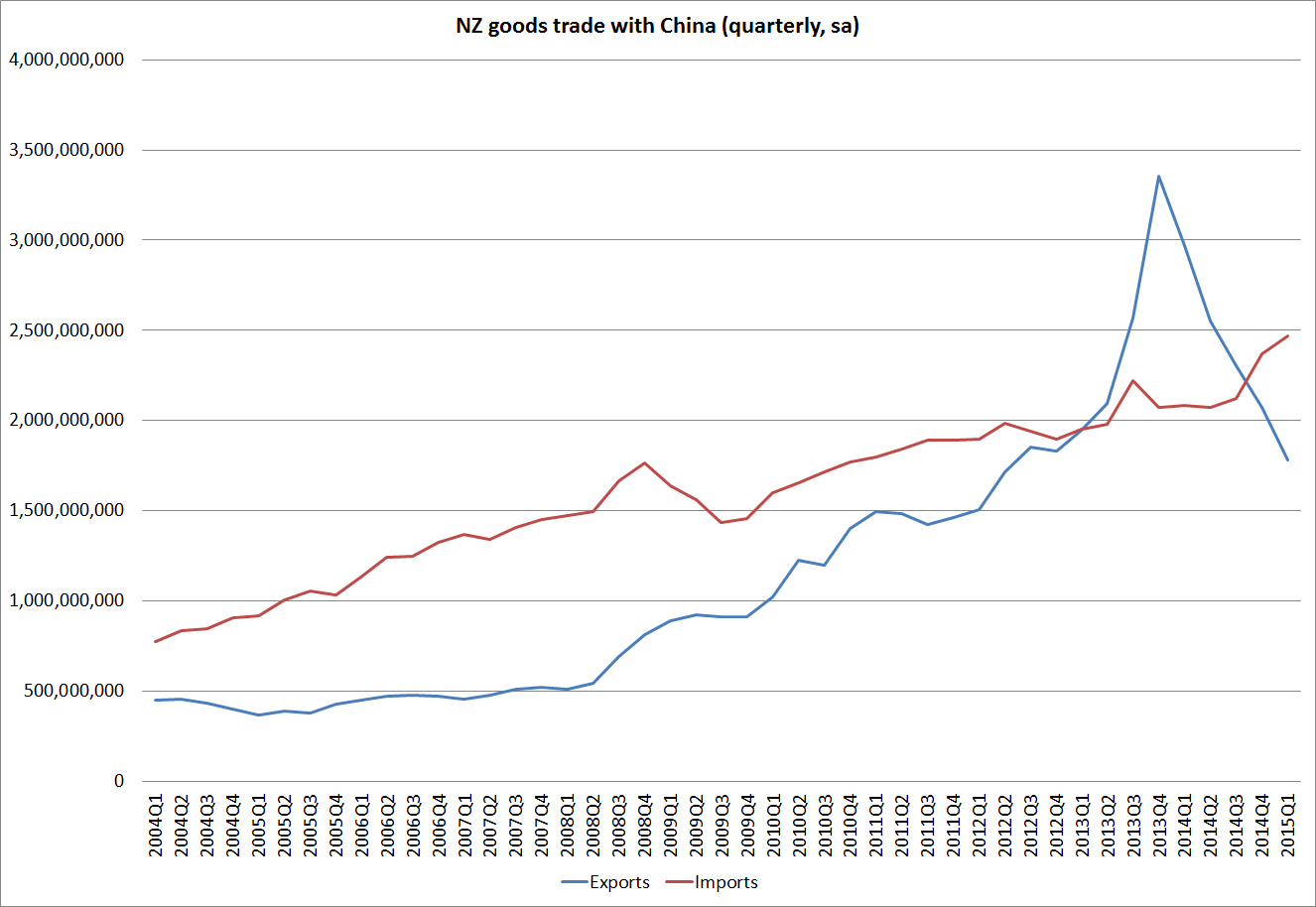

In the new TWI, the CNY has the second largest weight (20 per cent), just behind that on the Australian dollar.(22 per cent). But for the time being, that is likely to be high tide mark for the weight on China’s currency. Here is what has happened to goods trade – imports from China have kept on rising, but export values have plummeted (mostly on the fall in dairy prices).

A bigger question is one about what the appropriate weight on the CNY (and other currencies) is. I’ve argued that the CNY is important to New Zealand not because in a particular year we happen to sell lots of milk powder there, rather than in some other market, but because China is a large chunk of the world economy. If we had no direct trade with China, it would still matter quite a bit. In that sense, I reckon the new TWI understates the economic importance of the USD and the EUR, and overstates the importance of the AUD. We trade a lot with Australia, but Australia has very little impact on the overall external trading conditions our tradables sector producers face.

There are no easy answers to these issues. In a sense, that was why the Bank settled last year on a simple trade-weighted index. It wasn’t necessarily “right”, it wasn’t what everyone else did, but it was easy to compile and easy for outside users to comprehend. And without spending a huge amount of resources, on what was (probably appropriately) not a strategic priority, it wasn’t clear that any more sophisticated index would provide a better steer on the overall competitiveness of the New Zealand economy.

An issue of the Bulletin, written by Daan Steenkamp, covered some of this ground last December.

As already discussed, the new TWI has appreciated much less than the old TWI over the past decade or so. It is natural to ask whether the difference has, or should, affect how the Reserve Bank interprets or assesses the exchange rate. For example, are recent judgements about the ‘unsustainability’ of the exchange rate around recent levels affected? The exchange rate, however measured, is never considered in isolation from everything else that is going on in the economy. The Reserve Bank has, for example, recognised the rising importance of Asia in New Zealand’s trade and has taken that into account in its analysis and forecasting over the past decade or more. Exporters and importers deal with individual bilateral exchange rates, not summary indices. And New Zealand’s longstanding economic imbalances have built up with the actual bilateral exchange rates that firms and households have faced over time. How those individual bilateral exchange rates are weighted into a summary index therefore does not materially alter the Reserve Bank’s assessments around competitiveness and sustainability. Applying the macro-balance model (Steenkamp and Graham 2012) or the indicator model of the exchange rate (McDonald 2012) to the new TWI there are inevitably some changes, but the conclusions of those models, about how much of the exchange rate fluctuations are warranted or explainable over the past decade or so, are not materially altered.

There is no single ideal measure of an effective exchange rate index. Different TWI measures are useful for different purposes. In trying to understand changes in competitiveness it is likely to be prudent to keep an eye on them all. Developments in specific bilateral exchange rates will also have different relationships with economic variables and will be useful for different types of analysis. The focus of the Reserve Bank’s approach is on assessing the impact of the exchange rate on the competitiveness of New Zealand’s international trade, and the implications for future inflation pressures. Developing a full indicator of competitiveness, that reflected the specific nature of New Zealand’s international trade, and in particular the importance of commodity markets would require a very substantial research programme. It is difficult to be confident that the results would offer a materially better summary exchange rate measure than the simpler approaches the Reserve Bank has customarily adopted.

Of course, if China continues to grow in significance in the world economy, and if its currency becomes more convertible and is floated, it will become increasingly important to New Zealand. At the moment, the risks around China look somewhat the other way round – the influence of China may be more about the nasty aftermath of one of the biggest, least-disciplined credit booms in history. Growth looks to have fallen away much more than many (including the Reserve Bank) seem to have yet recognised. But whatever the correct China story, the influence on New Zealand has little or nothing to do with how the Reserve Bank’s trade-weighted index is constructed.