New Zealand’s quarterly suite of labour market data came out yesterday, and it seems to have shifted markets – and some domestic economists – a bit closer to expecting OCR cuts later this year.

Before getting to the substance, it is worth noting again some of the deficiencies in New Zealand’s (official and survey) macroeconomic data. Of 34 OECD countries, for example, we are one of only two without a monthly unemployment rate series. And neither of the two main business surveys – the QSBO and the ANZBO – has a question on wage expectations. The QSBO is a wonderful resource, and has a very long time series even by international standards. But sometimes history can be an obstacle: 25 years ago, when New Zealand wage-setting was being liberalised I encouraged the NZIER to include a wages question, and the response was “oh, we wouldn’t want to disrupt a survey with such a long time series”. The Reserve Bank pays to help keep the QSBO going, so perhaps they might renew the approach one day.

In one sense there was nothing very new in yesterday’s numbers, but the data will have unsettled those backing the Reserve Bank’s stance precisely because there was no sign of wage inflation picking up or excess capacity being reabsorbed. Employment growth continued, but in a way that continues to imply pretty poor productivity growth against a backdrop of reasonable (but unspectacular) GDP growth.

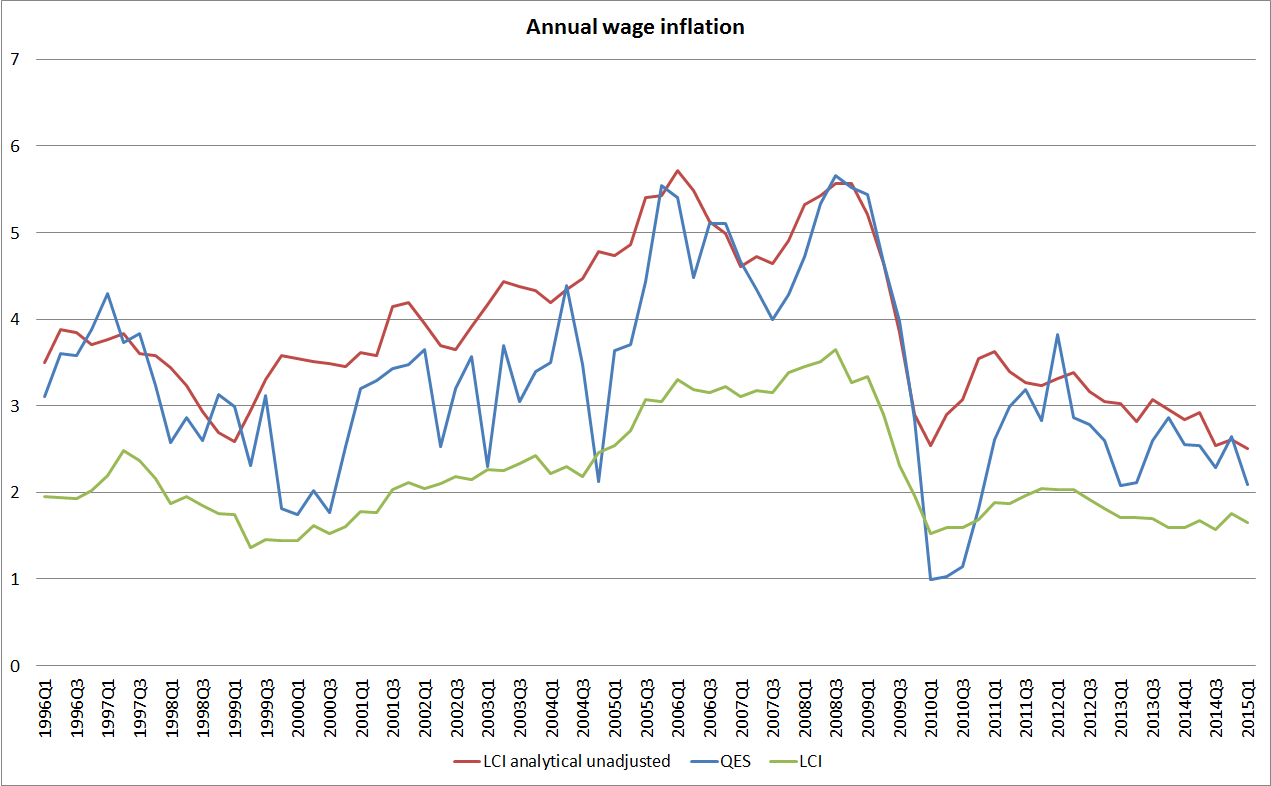

There is a variety of different wage measures in the QES and the LCI. I’ve charted some of them below. As former colleagues know, I’ve long had a bias towards the LCI analytical unadjusted series – both during the boom, and in more recent years. It is smoother than the QES hourly earnings series, and it is a wages series, rather than an attempt at a ULC measure. But we have all the series, and we should probably look at them all.

None of them suggests any recovery in wage inflation. The chart shows annual growth rates. There is seasonality in quarterly wage inflation, and SNZ does not seasonally adjust any of the series, but the data showed the equal lowest quarterly increase in the LCI since the recession began in 2008, and the lowest quarterly increase in the analytical unadjusted LCI since the recession began (the QES is too noisy to make anything much of quarterly changes).

And remember that these trends are consistent with what businesses have been expecting in the wages question in the Reserve Bank’s own smaller survey of expectations.

Wage inflation tends to lag a bit behind activity in the labour market, so we probably shouldn’t normally put too much weight on wages numbers. Unemployment (and underemployment) measures are another matter, and they don’t make a welcome picture. Recent unemployment rates were revised up a touch, and there was no change in the unemployment rate in the most recent quarter. The official unemployment rate lingers at 5.8 per cent – and I know no one who thinks the New Zealand NAIRU is that high – but it has come down by around one percentage point from the average level over 2009 to 2012.

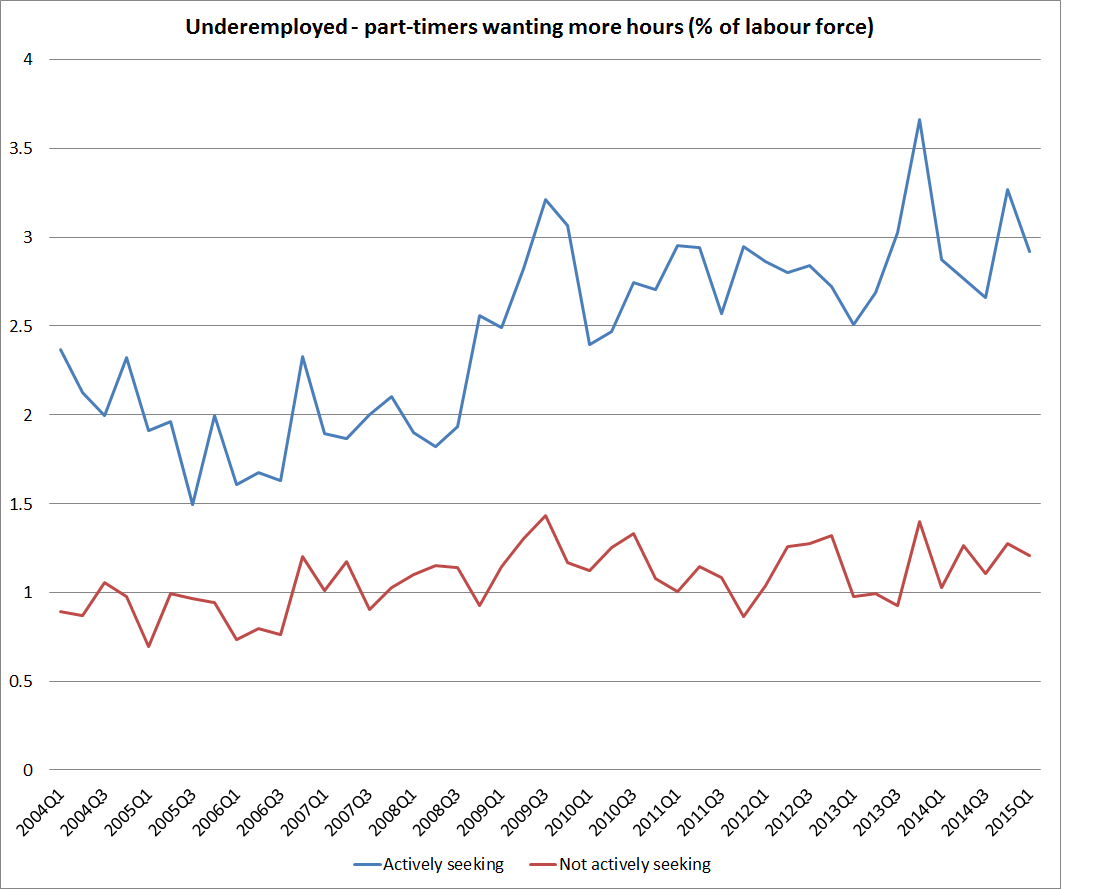

The same can’t be said for some of the other measures. SNZ has a couple of measures worth looking at, although unfortunately neither of them is seasonally adjusted.

One of them is to look at part-time workers who would like more hours (underemployment). These are people already holding down jobs – not detached from the labour market or losing basic work skills. We can distinguish between those actively seeking (a specific SNZ definition) and those wanting more hours but not actively seeking. Both represent additional available labour, but the former more immediately than the latter. It is the former category – those actively seeking extra hours – that rose sharply during the recession and has not come down at all since. The latest March observation is higher than the observation for March 2014.

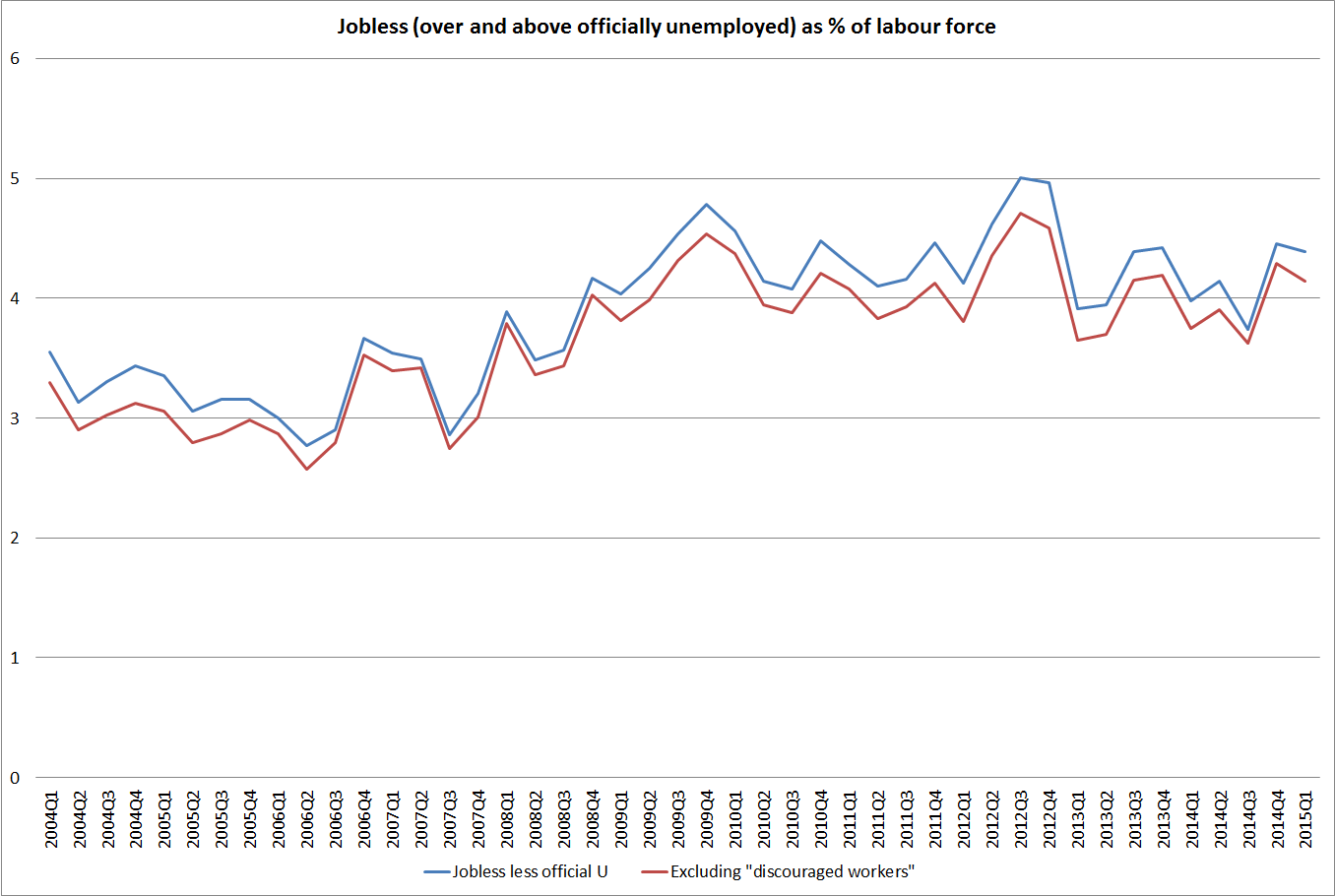

And then there are the people without jobs who would like one, but who don’t meet the definition of official unemployment (available to start work now and actively looking now). These measures of excess capacity have barely come down at all (and again, as a crude attempt to deal with seasonality, this March’s numbers are higher than those for last March).

I’m not suggesting one can simply add the various underemployment measures to the official unemployment rate to get a measure of excess labour market capacity. But looking across the range of measures, suggests that there hasn’t really been much excess labour market capacity absorbed in the last few years, and probably none at all over the last 12 months or so. That might be a quite welcome outcome if the New Zealand economy was near functional stable-inflation-consistent full employment. But it isn’t, and hasn’t been now for some years. Real people’s lives go on being marred by unnecessarily high unemployment.

And, yes, I’m well aware that participation rates have been rising. And no doubt that is welcome – some mix of voluntary optimising choices, and a bit of help from welfare reform. But excess capacity – supply relative to demand – is what should matter for monetary policy. Demand just has not been strong enough to soak up the additional labour.

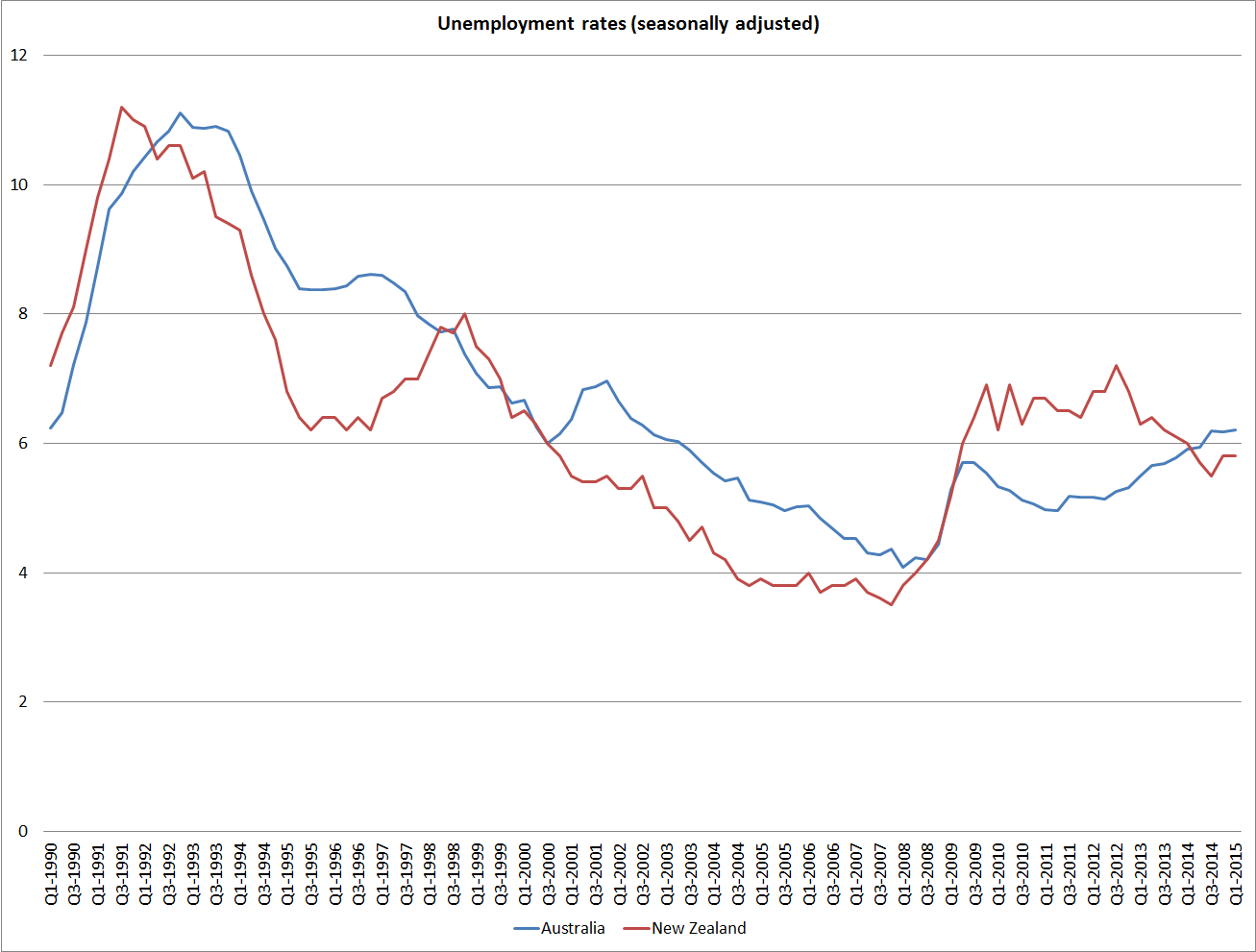

Finally, a trans-Tasman comparison. The Reserve Bank of Australia cut it policy rate again earlier this week. Australia’s inflation rate (headline and underlying series) is less far below target midpoint than is the case in New Zealand. But it was the unemployment rate comparisons I wanted to illustrate.

New Zealand’s unemployment rate is a little below Australia’s. But that has been the normal of state of affairs since New Zealand liberalised its labour market regulation in the early 1990s. From 1992 until the end of 2007, New Zealand’s unemployment rate averaged just over 1 percentage point lower than Australia’s – a credit, mostly, to New Zealand’s generally more flexible labour markets. During those 16 years there was only one period when New Zealand’s unemployment rate matched and briefly went above Australia’s – the period associated with the 1998 recession, a period in which everyone agrees that the Reserve Bank of New Zealand did not exactly cover itself with glory (the MCI, and holding monetary policy far too tight too long during the Asian crisis).

The unemployment rates in both New Zealand and Australia rose in 2008/09. But what is striking, and sobering, is how long New Zealand’s unemployment rate stayed above Australia’s. Even now, the gap is only 0.4 percentage points. Defenders of the Reserve Bank’s stance might point out that Australia experienced a huge investment boom in response to the high terms of trade. And New Zealand saw nothing of the sort. That is of course true, but we might reasonably wonder what New Zealand’s economy might have looked like if the OCR had been cut further and held lower after 2009. With hindsight there was no reason not to have done so. Unlike many advanced countries, our Reserve Bank was not constrained by either actual or perceived near-zero lower bound issues. It was simply a repeated misreading of the inflation outlook – not a no-cost mistake either but one that has left the unemployment rate lingering so much higher, and for longer, than it needed to be. And, as I noted last week, our real economic recovery, measured in terms of real GDP growth, has not been strong by historical standards either, despite the initial deep recession.

What of the current situation? Our unemployment rate is below Australia’s again, even if less far below than the historical average. But both countries have unemployment rates above any reasonable NAIRU estimates – and with no sign now of falling unemployment rates. One country has been steadily cutting interest rates, to new historical lows. The other first distinguished itself from the rest of the advanced world by raising interest rates even as inflation fell further below target, and then has resisted the increasing calls to do something about reversing last year’s mistake. Overseas commentators tended to see the mistake first, but even domestic bank economists are now beginning to recognise that something went wrong. How long will it take for the Reserve Bank of New Zealand to act?

It surprises me a little that the political Opposition has not made more of this bad misjudgement by the Reserve Bank, and its consequences for the unemployed. We don’t want a situation in which every OCR decision is a partisan contest, but an essential feature of the monetary policy framework is supposed to be serious accountability for the Governor. Perhaps some of that is happening behind closed doors, but the next time the Governor appears before the Finance and Expenditure Committee on monetary policy we should hope that our representatives ask him some pretty searching questions about what increasingly look like costly monetary policy misjudgements.

Speaking as a “shifted” domestic economist, in my mind yesterday’s labour market data was material. Given my worries about where the housing market is headed I was happy to defend the RBNZ’s position for as long as I believed that economic growth was above-trend, the labour market was tightening and thus wage and (core) inflation pressures were more than likely than not to pick up over the coming year or so. I had regarded the lift in labour force participation and the unemployment rate in the Q4 survey as exaggerated. After yesterday I can’t defend that position. I still think we will see some lift in inflation going forward (surely there is a limit to how far participation can rise?) but yesterday’s data suggests it will be more moderate and confidence levels around that forecast have surely grown. I expect it will be hard for the RBNZ to compile a set of projections in June that on an unchanged-OCR basis sees inflation rise to an acceptable level within an acceptable timeframe. And if they project easing, but don’t deliver it in June, the question will be ‘why did you wait’?

I will be interested to see what the RBNZ comes up with in the FSR next week – if they can progress measures that might help slow Auckland’s housing market (even if only at the margin) the market will be far more comfortable with modest rate cuts (as will I).

LikeLike

I’m sure your final sentence is descriptively accurate, although I would argue that (a) house prices, esp just Akld house prices, aren’t part of the target – or any wider unwritten mandate – for mon pol, and (b) any new regulatory measures are only likely to impede the efficiency of the financial system, and perhaps the efficiency of the housing market. Without fundamental changes to supply conditions, or population pressures, any controls only provide cheap entry levels – as they would have if imposed in 2006 (say).

LikeLike

It seems to me that the RBNZ and most domestic economists have completely underestimated the structural changes in the global economy over the past 20 odd years and instead have been relying on historical cyclical models. Globalisation has been a huge influence as has the rapid introduction of new technology and innovation. these factors plus others have opened up the world and created a far more competitive market place. Capital and labour have generally moved freely between markets and so the emphasis on ‘domestic’ capacity constraints seems near irrelevant.

One of the unintended consequences of QE and near zero interest rates around the world has been the expansion of capacity – cheap money has funded a massive increase in supply – leading to today’s global deflation (centred in China). The original intention was to increase demand but with balance sheets maxed out with debt around the world, populations aging, and unemployment stubbornly high the old analogy comes to mind.. you can lead a horse to water but you cant make it drink!

New Zealand will continue to import deflation while the deceptiveness of nominal GDP and terms of trade data hollows out the rest of the economy.

LikeLike

I only have a quibble. The wage and employment data do not imply “poor productivity” they only say that “real” wages are still lower than productivity, thus firms hire more now. Firms do not hire workers when real wages equal to productivity, and they certainly layoff workers when real wages are higher than productivity. I think macroeconomic analysis of the labor market in New Zealand could benefit from microeconomics analysis at the firm level. I have not seen that. Givencurrent data, one must expect the unemployment to fall in the future, towards the natural rate, and expected inflation to start to increase. I suppose that the RBNZ looks at tomorrow ( one to two years ahead) when setting the OCR for today so the development of expectations matter.

LikeLike