That was the title of the presentation at yesterday’s lunchtime seminar hosted by Motu, the economics consultancy/research group. Motu has started up this series of public policy seminars – a laudable initiative, even if the costs mostly seem to be being met a group of sponsoring government agencies. The first such session was a month ago on minimum wages – I never got round to writing about it, but the summary is probably “not as useful or as damaging as is often claimed”. Perhaps it is going to be a theme, since a one line summary of yesterday’s immigration session could be quite similar.

A session on immigration policy is obviously timely, given that the government says it is cooking up changes to various aspects of policy (for which, despite a speech from the minister, there is still no supporting analysis or any details), and in view of the inquiry the government has directed the Productivity Commission to undertake. (On that note, the Productivity Commission recently released an Issues Paper, outlining some of the issues and posing some questions they particularly want submissions on.)

So I went along to the seminar yesterday expecting to be challenged and stimulated by the speaker, David Card from Berkeley (by Zoom). Card has written a lot over the years on immigration, and some of his studies are widely cited. My impression was that he was generally positive about immigration, but then he was mainly writing with the US in mind, and based in greater San Francisco. But clearly a very able guy.

In fact, the seminar was a bit disappointing. I suspect most of that was the fault of the organisers rather than of Card. They’d scheduled the session for 90 minutes, allowing time for some discussion from local panellists and some audience questions, but Card only spoke for at most 30 minutes and was evidently operating to a time slot he’d been given. And although he had made some effort to dig out some New Zealand numbers, none of those numbers would have been news to the New Zealand audience, and he (unsurprisingly) didn’t have much in-depth knowledge of New Zealand or its challenges. But that meant that what he had time to say more generally won’t (I suspect) have added much to anyone’s understanding, whatever one’s view on New Zealand immigration policy. That was a shame.

There were familiar snippets. The stock of foreign born people in New Zealand is high, among OECD countries. There is a lot of variability in net immigration to/from New Zealand (although, oddly, he never touched on the distinction between New Zealanders (not the subject of immigration policy) and others (who are). There were various high-level outcome numbers (employment, incomes) that often don’t look too bad – at least for non-Pacific migrants – but – not stratified by age – often don’t reveal much either.

There was the useful reminder that while there might be a ready (“potentially infinite”) supply of people from poor countries who would move to rich countries if they could, the potential supply of people from rich countries is much more limited. He noted that in the US context – which is quite different from New Zealand – policy settings tend to mean that immigrants are either very lowly skilled (illegals and family reunification) or very highly skilled (“doctors and janitors” – a large proportion of US migrants are apparently in the healthcare sector).

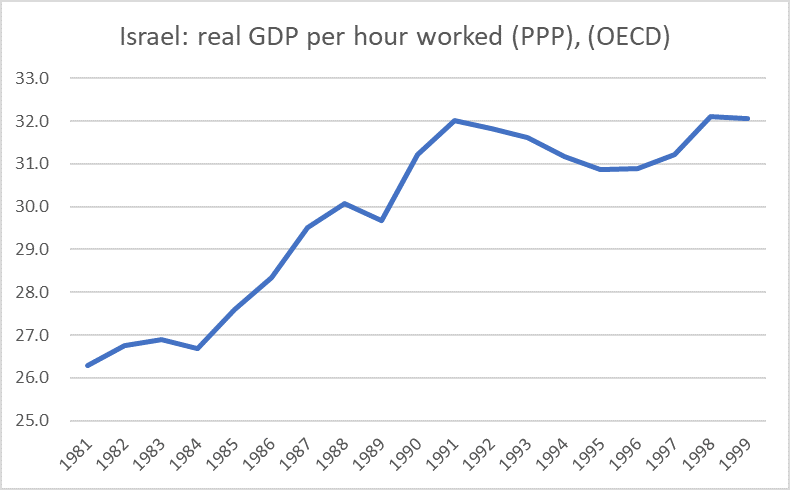

He touched on the perennial question of whether growth in the capital stock keeps up with migrant inflows, and while suggesting that it generally does – especially in the US – he noted that these things needed to be looked at on a case-by-case basis. There is a series of studies in the literature on large shocks to migration – eg French returnees from Algeria, Portugese from Mozambique and Angola, and the influx of Soviet Jews to Israel in the early 1990s. Card talked briefly about the latter case, presenting a chart showing the big surge in investment in Israel in the wake of the influx of people. That is what one would expect – and hope for – but as one of the discussants pointed out, actually it hadn’t tended to happen here (business investment as a share of GDP has been low by OECD standards for decades).

More generally, Israel’s productivity performance has been poor, especially in the 1990s.

But I’m not going to disagree with Card: careful case-by-case analysis really does matter.

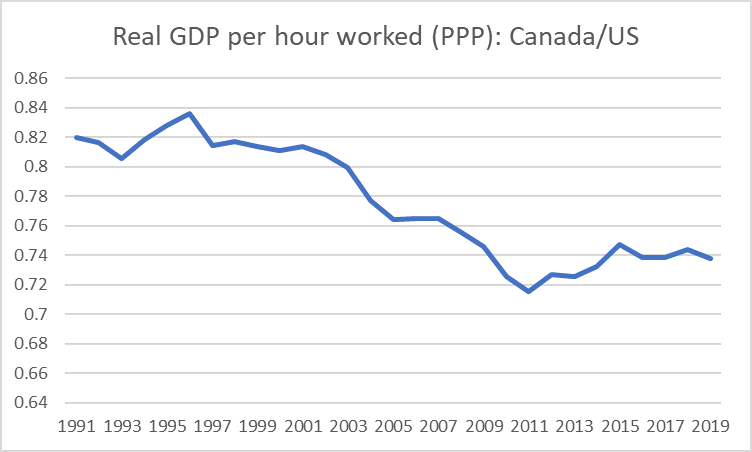

I hadn’t known that Card was Canadian, and he did offer some interesting comments on the Canadian experience – they now target about as many non-citizen migrants per capita as we do. As he noted, in the US there is often (correct) talk of the number of Nobel prize winner or entrepreneurs who had been migrants, but experiences different considerably by country, and he noted that Canada had had nothing of that sort of experience, suggesting that Canada’s shift to a skills-based migration approach had, on that sort of metric, been a “failure”. Canada has never been an OECD productivity star – not even 100 years ago when New Zealand and Australia matched the US as richest countries in the world – and the last 30 years have seen their gap to the US widen, despite an immigration policy (a) very similar to New Zealand’s and (b) widely admired.

And that with all the advantages of proximity (Toronto is closer to New York than Wellington is to Auckland).

(Incidentally, one of Card’s points was about the benefit to migrants themselves, and the question of what weight should be placed on that benefit in national policymaking. Both are fair points/questions. But he noted that his own English ancestors had been dirt-poor when they migrated to Canada in the early 19th century, as an illustration of the gains. I’m sure many of us have similar stories – I like to talk of one particular set of my ancestors who were poor Yorkshire farm labourers when they left in 1860 – but it does rather overlook two things: first, most ancestors of present day English people were also very poor 150-200 years ago, and – at least on the OECD numbers – average productivity in New Zealand, Canada, and even Australia – is now below that in the UK, and that is before getting onto the better of the Latin American countries (Chile, Uruguay and Argentina) in comparison to Spain and Italy.)

He touched on a couple of other aspects that some times pop up in debates around immigration. On fiscal effects, his read of the (limited) literature tended to be that “immigrants contribute a little more than they take out”, but even that result depends on (a) the types of immigrants, and (b) how one allows for the implications of migrants having children, and how well those children do. The fiscal effects of immigration are never an issue I’ve focused on (I don’t think it is a big issue, one way or the other, with the type of migration we’ve mainly had) but did offer some thoughts here on some earlier (too positive) New Zealand estimates (which were done by the firm run by the now chair of the Productivity Commission)

And then there was housing. For me, he got off to a bad start by suggestion that in Wellington “like San Francisco” there was really no more land for building houses – he seemed quite unaware of just how much low value land the Wellington region (and city) has. Card really wanted to play down this issue, and presented some back of the envelope guesstimates suggesting that if our cities allowed development as readily as, say, Houston does, it really wouldn’t make much difference at all to house price inflation in the presence of population growth. It was clear he really didn’t like Houston – even as individuals self-select towards affordable housing in Texas. Believe that if you want, but I suspect it is a guesstimate from a model that takes into account house-building but not land restrictions. (And to repeat, in a first best world the housing market should not be a consideration one way or the other in setting immigration policy, since fresh land would readily and continuously be brought into development at a price not much different to the value of that land in alternative uses.)

Oh, and he observed that across the variety of types of models, the effects of immigration on the labour market (positive or negative) tended to be pretty small.

And that was the end of the presentation.

There were three panellists: Dave Maré from Motu itself who has done various micro studies over the years on immigration in New Zealand, Julie Fry who has written quite a bit in the last 7 or 8 years and was recently co-author of a contentious piece for the Productivity Commission, and Nik Green the director of the Productivity Commission’s immigration inquiry. There were a few interesting snippets in their remarks:

- Maré noted that for all the research that had been done it was hard to find strong evidence of much good or bad stuff resulting from New Zealand’s immigration. He noted that ideally you really want people who are different from natives – to complement us – but that a qualifications-based approach wasn’t necessarily the way to achieve that. And, on that note, he seemed very sceptical of the “literal and engineering approach” taken to granting visas, with the heavy focus on immediate short-term gaps.

- Fry noted that she had first worked on immigration at Treasury 30 years ago when the new immigration policy looked like a one-way bet, really only offering upside. Her conclusion was that reality was a lot less clear, noting that although we had attracted “lots of nice people” there had been no dramatic economic gains. But she was at pains to stay on the liberal side of the debate, noting that naysayers needed to be confronted, and wasn’t it a good thing that Covid had shown we could have crazy house price inflation without immigration.

- Green didn’t say much, but did note questions around the increasing reliance on temporary migrants, as well as explicitly referencing my points around the macroeconomic imbalances New Zealand immigration may have contributed to over many years.

Card’s response was brief, and centred on a chart of GDP per employee for the Anglo countries over the last 10 years or so, indexed to a common starting point. His point seemed to be that immigration hadn’t made much obvious difference to any country’s productivity story – which might possibly be so, but it seemed an odd basis on which to rest such a claim (being poor relative to the other Anglos, we’d have hoped to be catching up, growing faster).

And then he presented a chart of population densities by OECD country, in which – of course – the three OECD countries most focused on targeting high immigration have among the lowest population densities. I’m pretty sure there are good reasons why people don’t live in most of Canada or Australia…….and there seemed to be no reference to economic geography in any of this anecdote.

Then there were questions from the floor.

Eric Crampton tried to get a ringing endorsement of high migration by asking if we shouldn’t just believe overseas research, noting that water flows downhill everywhere. Card – having previously explicitly noted the need to look at experiences case by case – noted that such a question was “a little above my pay grade”. But then he went on to make the weird claim that New Zealand was an “extraordinarily open economy” – when our trade shares are very low for a small advanced country – and that in such an economy wages should simply be set globally (labour supply not making much difference). Nonetheless, actual New Zealand wages are low by OECD standards, commensurate with low rates of labour productivity here.

There was the useful note that – in New Zealand, and the Anglo countries, but often not in Europe – kids of migrants educated in the host country tend to do pretty well.

There was another question from the floor – from a fairly eminent figure – about regional effects, in which it appeared to be suggested that actually rising house prices in Auckland, even if driven by migration, might be a good thing as they allowed natives to sell up and move to nicer places elsewhere in the country (the questioner, raised in Auckland, deemed most places nicer). It seemed a really bizarre question, especially if – as the consensus tends to be – big cities are the cutting edge of innovation and income growth. Card avoided that specific question, but actually seemed quite cautious on the cities point, noting that although incomes in big cities tend to be higher it wasn’t clear how much of that was causal, and suggesting that the true effects might be quite modest (globally, I was a bit puzzled by that given the huge differences – especially in Europe – in GDP per capita in big cities vs the rest of the respective countries.)

That question prompted Julie Fry to throw in the observation – with which I totally agree – that the policy (adopted by the NZ government) of trying to steer migrants regionally does not work and should be stopped. (It also tends to lower the quality of the average accepted migrant, by selecting for willingness to go to the provinces rather than ability.)

The final question was about crime and migration. Here again, Card was cautious and noted that different places had different experiences (noting challenges especially in Sweden and Denmark). He noted that in the US per capita crime rates of migrants were lower than for natives – while noting, in effect, that per capita might not count for much if you are the victim of an individual – with (as in so many other variables) regression towards the mean in the second generation. Eric Crampton added the similar New Zealand experience, noting correctly that it isn’t that surprising since one needs a criminal record check etc to be a migrant to New Zealand.

It was an odd session. Perhaps some people in the audience got something out of it, but I’d be surprised if anyone got much. It was interesting to see the near-complete absence of much enthusiasm – whether from Card or the local panel – for large scale immigration as something economically transformative (recall that not many years ago MBIE was telling us – and ministers – immigration to New Zealand was a “critical economic enabler”). One was left wondering why then the New Zealand government should be running one of the very largest per capita immigration programmes in the world – perhaps the more so when the natives are leaving and governments refuse to fix the housing/land market – when the programme has long largely been economic in motivation.

But – as with the Commission’s Issues Paper – there was a lot missing from the discussion, including a lack of any engagement with the possibility that even though wages in New Zealand have done well relative to producttivity, large scale immigration, in our specific circumstances, may have contributed to the deeply underwhelming productivity and foreign trade performance.

(It was a seminar day. I went on from the Motu event to a presentation at Treasury of the BERL work done for the Reserve Bank on “the Maori economy”. Even the speaker noted that “the Maori economy” is not a “separate, distinct, and clearly identifiable segment” of the New Zealand economy, and so one was still left wondering why they’d spent the money. I won’t extend this post with a lengthy account of a fairly underwhelming session, but will leave you with the data that simply staggered me. According to the report, in 2018 35 per cent of the total income of Maori households came from welfare benefits and other state direct assistance, up from 21 per cent in 2013. For the rest of the population BERL reported that the share was 9 per cent in 2018, down from 13 per cent in 2013. I’d have been reluctant to believe it, but so it appeared to be.)