My teaser for today’s post was this tweet

If I remember correctly, the last time was probably in mid-2011 when the then OCR Advisory Group was debating when to reverse the emergency cut we’d put in place after the February 2011 earthquake. As it happens that was all overtaken by the intensifying euro crisis.

Yesterday’s Monetary Policy Statement has been described, colloquially, as “hawkish” or at least having taken a “hawkish tilt”. I’m not really sure that is warranted, but it is hard to tell.

The MPC reintroduced a projection track for the OCR for the first time since this time last year, and in that track the OCR starts to be lifted gradually from the September quarter of next year. I have never been a fan – going back to the introduction in 1997 – of the OCR projection track, since it is little more than castles in the air make believe to suppose that anyone knows now what OCR will be appropriate a couple of years hence, in turn driven by the outlook a couple of years beyond that. What we need – and what central banks can tell us sensibly – is where they think things might head by the time of the next review. But, like it or not, we have a forward track. That track was always going to show OCR increases at some point, if only for two reasons (a) the Bank’s model will always have interest rates heading back towards neutral as inflation settles around target, and (b) the LSAP programme – which the Bank claims to believe is highly effective – runs out next June.

And when the Governor was asked at the press conference how much the forward track had changed from what it would have been (unpublished) in March he simply refused to say.

But we do know, because the Committee told us, that “our medium-term outlook for growth remains similar to the scenario” in the February MPS. And their numbers support that: GDP growth over the two years to March 2022 is exactly the same (2.9% in total) as they’d shown in February, and for the following two years projected growth is just a touch lower than in February. On the other hand, they seem to have revised down their potential output growth assumptions a bit, and as a result the output gap estimates have been revised to something less negative/more positive.

| RB Output gap projections, average for full year to March | ||||

| 2021 | 2022 | 2023 | 2024 | |

| Feb MPS | -1.0 | -0.6 | 0.9 | 1.4 |

| May MPS | -0.4 | -0.2 | 1.3 | 1.3 |

And although they claim to believe that the economy is still below “maximum sustainable employment” I don’t think their hard numbers really back up that view. The unemployment rate is currently 4.7 per cent, they expect to be still 4.7 per cent next March, and then over the following couple of years when the output gap is projected to go materially positive they only expect the unemployment rate to drop to 4.4 per cent. On their numbers, unemployment must now be very close to the NAIRU (functional full employment, given the regulatory environment and labour market institutions etc).

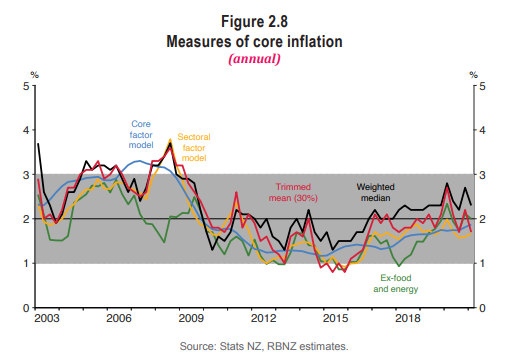

What else do they tell us about the near-term? Well, there is core inflation. They include this chart

That is much the same suite of indicators that led me to conclude last month

I think it is is probably safe to say that core inflation in New Zealand is now back at about 2 per cent. That is very welcome, even if somewhat accidental (given the forecasts that drove RB policy).

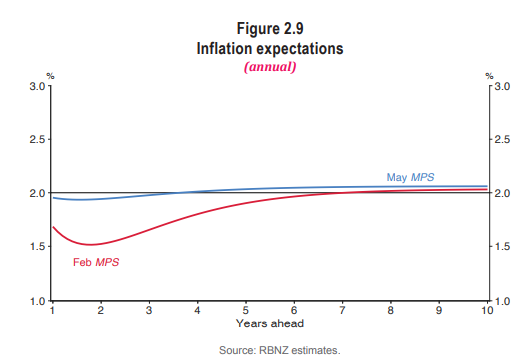

Same goes for the (somewhat selective) range of inflation expectations measures the Bank summarises here

That’s good too. Quite a lift in the last few months and now about as close as you are going to see to 2 per cent right across the horizon,

And then the Bank tells us their decision rule

The Committee agreed to maintain its current stimulatory monetary settings until it is confident that consumer price inflation will be sustained near the 2 percent per annum target midpoint, and that employment is at its maximum

sustainable level.

But on their own numbers, that seems to be (a) pretty much the current situation, and (b) the outlook. Now, to be sure, that statement isn’t entirely coherent because logically you have to be confident of those outcomes even after you start tightening monetary policy a bit, but set that to one side for moment.

And so I guess that is why I’m left wondering whether it is even remotely fair to characterise yesterday’s statement as having a hawkish tilt. They have rising (to record) terms of trade, significant fiscal stimulus from a big fiscal deficit, they think the output gap is all but closed, and any unemployment gap must be close to being closed, core inflation (and expectations at target) and yet they think that precisely the same monetary policy settings are warranted as was the case six months ago, more aggressive than those in place a year ago (given that the Funding for Lending Programme, which is effective, is a more recent addition). As a reminder, as recently as November they had inflation averaging 1 per cent for 2021 and 2022 (on exactly the current monetary policy).

Perhaps the operative word in that decision statement is “confident”, but realistically (a) when is macro forecasting ever confident? and (b) they must have greatly reduced uncertainty/error-margins now than was the case a few quarters ago. It isn’t as if actual core inflation is 1.5 per cent but the forecasts show it getting to 2 per cent, or actual unemployment is 6 per cent but forecasts show it getting to 4.5 per cent.

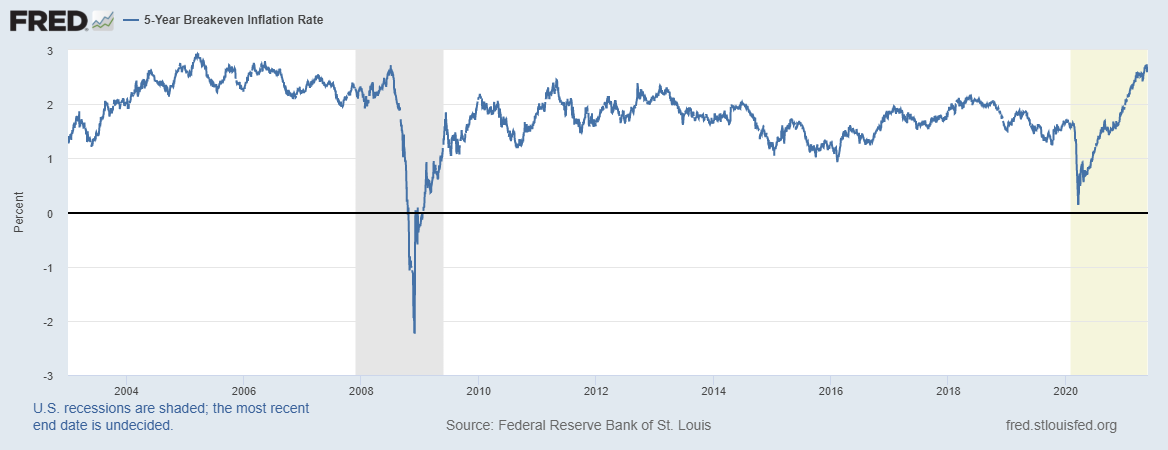

I guess the other thing I found striking about the document is that although the Bank has a couple of pages on how to think about short-term price shocks (the sort of boilerplate stuff that has appeared in MPSs every year or two for 30 years) – and I suspect they are quite right on that narrow point (eg that headline inflation of 2.6 per cent for the year to June is not, of itself, something to worry about – any more than similar spikes in, say, 2008) – there is no discussion at all of the increase in market-based measures of inflation expectations here and abroad.

In the New Zealand case those inflation breakevens from the indexed bond market are still sitting a little under (but “near”) 2 per cent, but that is a great deal higher (and thus much more reassuring) than the situation for the last few years. In the US – easiest market to get the data for if you don’t have a Bloomberg terminal – we see something like this

These breakeven numbers move around a bit but when we look, for example, at the rise in implied expectations after then 2008/09 recession it didn’t overshoot to some ridiculous, unsustained level, but settled back in a fairly orderly way (even amid some political hyper-ventiliation about inflation risks of QE) to something a bit lower than in the pre-recession period. Perhaps this time is different. Perhaps nothing will deliver average inflation anywhere near that high in the next five years. But you might expect an inflation-targeting central bank to at least discuss the point, and the possibility that the combined weight of fiscal and monetary policy will mean a drift (in some ways welcome) to higher inflation as the world emerges from Covid – especially when, at least in economic terms, the Bank’s own chart shows New Zealand to be ahead of most on that score.

And yet there is no any sign from the minutes that the Committee even robustly discussed these issues – even though, for example, just a couple of weeks earlier the Bank of England’s Monetary Policy Committee (known not just for a better class of member, but – as importantly – for more transparency) voted only by a margin of 7:2 to keep on with their bond-buying programme (a programme smaller than New Zealand’s as a share of GDP, in an economy that has been further behind New Zealand’s recovery).

So what is appropriate New Zealand policy now? I find it simply extraordinary that the Bank is continuing on with its huge bond-buying programme as if nothing has changed at all. Not only that we are told that

The Committee agreed that the OCR is the preferred tool to respond to future economic developments in either direction.

They offer no rationale for this statement. It might make some sense if things were suddenly to get a lot worse, but it makes no sense at all from here – inflation at target, expectations consistent with that, unemployment below 5 per cent – either substantively, or in view of all the criticism (often misplaced) the Bank has taken of the LSAP (“money printing”, “blowing bubbles” and so on). As I noted on Twitter yesterday, in the Budget documents there is stable suggesting that the stock of settlement cash balances is expected to rise by tens of billions of dollars over coming year (presumably as bond buying goes on and Crown issuance is pulled back). That just invites more (reputational) problems as well as complicating the eventual unwind of the huge bond portfolio. So had it been me, I’d have been cutting the LSAP now, perhaps terminating it completely within the next three months (all going according to plan). But since I do not believe that the LSAP is making any material difference to anything that matters much in New Zealand – where long-term government bond rates mostly only affect government borrowing costs – I wouldn’t have seen that as any material tightening of monetary conditions. The Bank would of course, but on their numbers there is a good case now for beginning to wind back purchases (as a policy lever).

I wouldn’t favour winding back the FLP or raising the OCR yet, but the FLP should be the next in line (after the LSAP). It is a extraordinary intervention, inconsistent with the general preference for indirect competitively neutral tools. It had a place late last year, but the current macro data suggest it should not be too long for this world (and should not be needed in future downturns now that the RB is confident they can do negative OCRs).

Lest I appear too hawkish, I should add that my decision rule would not be the one the MPC outlined. After a decade or below-target core inflation I think we probably should welcome at least some overshoot, for some period, of the 2 per cent midpoint (in core terms), if only to help cement in the public mind that 2 per cent is a target midpoint and not a ceiling.

Perhaps too the Bank is wrong about the macro situation. Perhaps there is more spare capacity than they think, in the labour market and more generally. I don’t have a strong view on that, but see no reason to think them very wrong (and I noted with interest there was no mention of the potential impact of higher minimum wages and higher benefits on either labour demand or supply, or the NAIRU – but any such effect is likely to be for the worse.)

Everyone tends to fight the last war. The decade after 2008/09 was one when too often central bankers (often egged on by markets) kept over-estimating how much inflation there was in the system, and kept getting it wrong. Perhaps that is still where central banks should err, but I would feel more confident about it in the New Zealand context if there was more evidence of careful thought/analysis, or sustained and searching debate around the MPC table, and of serious public engagement by thoughtful MPC members open to exploring differences. As it is, there is a strong sense of “trust us, we know what we are doing”, with little real evidence that they do.

Am I really more hawkish (less dovish) than the Bank. It is still hard to be sure, but there are things about their numbers on the one hand, and their policy stance on the other, that really don’t seem to add up. These include small points like the difference (a few paragraphs apart in the minutes) about how long it make take for them to be confident: first there was this

They agreed this would require considerable time and patience.

and then just a little later this

The Committee agreed it will take time before these conditions are met.

Those seem to me rather different emphases – the latter perhaps plausible, the former distinctly (probably too) dovish.

(To the Bank’s credit – and not that it greatly matters to them or their deliberations – they do not share the unreasonably over-optimistic productivity growth assumptions built into The Treasury’s Budget numbers).

Finally, I was reading last week The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival published last year (mostly written pre-Covid) and written by Charles Goodhart and Manoj Pradhan. There is a summary version of the story here. I’m still not quite sure what to make of the story, but I’m less unpersuaded than I had expected to be. Perhaps they are wrong, but it would be good to see some thoughtful central bankers and policymakers engaging on the possibilities and risks.)

Michael, the current incumbents, Grant Robertson and David Parker and many within the decision ranks of this Labour government were in opposition the last time you were aggressively hawkish on interest rates which saw bank Overdraft interest rates(which NZ businesses rely on for working capital) rising rapidly to 10% and beyond. The RBNZ engineered a bouyant and strong NZ economy into a deep recession with the loss of the entire building industry sector, which dominoed into the collapse of 61 Finance companies and the loss of $6 billion of ma and pa savings.

I certainly hope they will act as a handbrake towards any aggressive RBNZ interest rate rises. Any increases must be well spaced out to give businesses a chance to adjust. The nutcase policy of 3 or 4 interest rate rises in a year so common of previous RBNZ policy makers is just plain stupid.

LikeLike

We may (and do) disagree on the past, but I don’t see anyone calling for large OCR increases. But one of the reasons for some of the past RB increases being relatively rapid was that the Bank was sometimes slow to start.

To be clear I am not suggesting any OCR increases at all at present.

LikeLike

Your statement lies the heart of the problem with OCR decisions at the RBNZ.

“But one of the reasons for some of the past RB increases being relatively rapid was that the Bank was sometimes slow to start.”

This is the same as the RBNZ saying “I arrived home and my wife did not turn on the heater earlier to keep the house warm. Because it is too cold, I will start a fire and burn down the house to get warm.”

LikeLike

Central bankers themselves use a less extreme version of your analogy – coming into a cold hotel root and turning the heating right up only an hour or so later to end up quite overheated.

On the other hand, if I’m running late I will run for a bus or a meeting or whatever.

Do note that when the Bank was tightening in the 00s, I’m pretty sure no commentator/forecasters was predicting that doing so would result in inflation undershooting the target range. In fact, without the US crisis those OCR increases would probably only have been enough to have brought core inflation back down to 2-2.5%.

LikeLike

Your statement ” On the other hand, if I’m running late I will run for a bus or a meeting or whatever.” again highlights a major problem with RBNZ decisions.

It is like saying, “I am late, I will run to the bus. But the bus is across a 4 lane motorway and the traffic is heavy with cars running at speeds at more than 100km/hr in either direction. But Because I am late I will run across this 4 lane motorway laden with cars and pray there is no accidents and no one gets killed.”

LikeLike

Michael, the problem with setting a target of 2% for price increases in NZ decimates the NZ productive industrial economy. Our domestic producers operates in a low volume due to a small population. Low volume businesses need higher margins from higher prices to survive. The competition is China which is a High volume and low margin producer due to its much larger domestic market. Yes we want our producers to export and increase volumes but they must survive which means our RBNZ needs to be softer and allow wider inflation band targeting. Being the first in the world to tighten is just stupid. 3 or 4 interest rate increases a year just to get inflation to 2% is also stupid. It is just a train wreck and decimates our productive economy every time we go into a hawkish interest rate tightening.

LikeLike

Do note that even if the RB tightens a bit in the next 12-18 months it will not be the first advanced country to tighten: tiny Iceland has done so already.

But also note that so far our economy has rebounded faster than most, a good thing.

LikeLike

The NZ economy rebounded with a $13 billion wage subsidy and the the government borrowed an extra $41 billion last year for projects. If others like Iceland wants to be reliant on China and decimate our local producers then it is their stupidity. Why would we want to tighten and decimate our local producers and be China import reliant?

LikeLike

I disagree with you comment that there may not be much capacity increase available.The current clown show has and continues to demotivate the productive sector which could increase output & productivity given the right incentives so the laws & regulations they don’t like means the reaction is likely to be to push against and undermine and that effort is not productive, it is negative but on top of that many will not consider working as hard/long as currently as they do not see it worthwhile. The results will likely be a reduction in output and when the global economy enters a deep recession or depression the above will magnify and the loss of capital will make it more difficult to recover. My fear is that history will repeat and the solution as usual will be violence – war/civil war.

LikeLike

I don’t necessarily disagree with your general point, but note that mine was much narrower: the RB has to take all the rest of the regulatory structure etc as given and set monetary policy accordingly. There is much that could be done by policy makers to lift productivity in NZ but as they won’t the RB just has to operate with the constraints and limits that exist as a result.

LikeLike

The problem with our policy makers is that they mix up Productivity with Profitability.

To shut down Marsden Point refinery by NZ Refinery owners is a massive loss of Productivity but is a massive increase in Profitability for the business owners as it is now an import terminal to bring in cheaper refined petrol from Singapore. So if the government wants higher Productivity it must save Marsden Point Refinery with government subsidies.

In the past, NZ has simply added cows each year to increase Productivity because the number of cows are not counted in the Productivity equation. But having reached Peak Cow with now 10 million cow we simply cannot add more cows. As a result our Productivity suffers. Billion dollar government subsidies go towards supporting the farming community.

The question is why subsidise farming and not factories? Factories have higher Productivity outputs with less inputs than faming. 10 million cows use up the equivalent land, food and drinking water resources of 200 million people. GDP in NZ would be in the trillions of dollars with the same land, food/drinking water resources that 10 million cows that generate only a meagre $16 billion in GDP.

LikeLike