No, I’m not getting back into some routine of daily posts, and on this occasion the two topics don’t even have anything to do with each other, but are just a couple of a leftovers from things I was looking at over the last couple of days.

In my fiscal posts this week I’ve noted that the government is consciously and deliberately choosing to run cyclically-adjusted primary fiscal deficits in the coming year larger (probably much larger) than we’ve seen at any time since the end of World War Two. I noted in passing that although people are conscious of stories of large fiscal deficits under Robert Muldoon’s stewardship, in fact a large chunk of those deficits was interest payments, and this in an era when inflation was high, sometimes very high. When nominal interest rates are high just to reflect high inflation, the resulting “interest payment” is really more akin to a principal repayment. Back in the day, various people – especially at the Reserve Bank – did some nice work inflation-adjusting various macro statistics.

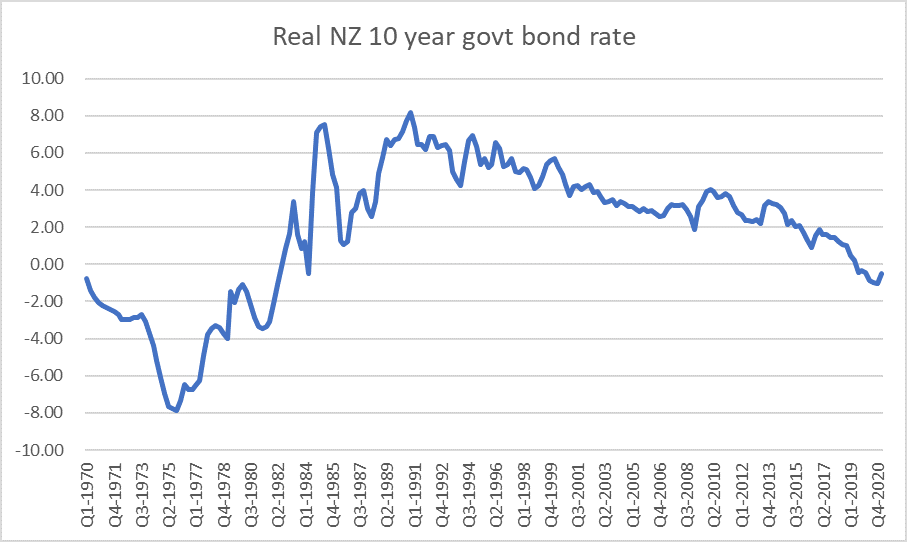

But just to check my point I put together this graph

What have I done here?

- got the OECD’s series for long-term nominal bond rates that goes back to 1970 (this will mostly be 10 year bonds or thereabouts, although for a time in the late 80s we were not issuing bonds that long),

- for the period since 1993, subtracted the Reserve Bank’s sectoral factor model measure of core inflation,

- for the period up to 1993, subtracted a three-year centred moving average of the CPI inflation rate.

So for almost entire period prior to 1984 real New Zealand government bond yields were negative.

This is, of course, not testimony to different patterns of desired savings and investment, but (mostly) to financial repression. Until 1983 government bond yields were administratively set and – much more importantly – most financial institutions were simply compelled by law to buy and hold government securities (often 25 per cent of more of total deposits). The costs were borne by depositors.

It is also worth noting that pre-1984 the government was also borrowing, at times heavily, directly from the retail market, at times offering real interest rates well above those shown here. And the government was also borrowing, again at times quite heavily, from abroad. In some of those markets, inflation was a big chunk of the headline interest rate, but in none of the major borrowing markets were government borrowing rates by then as repressed as they were still in New Zealand.

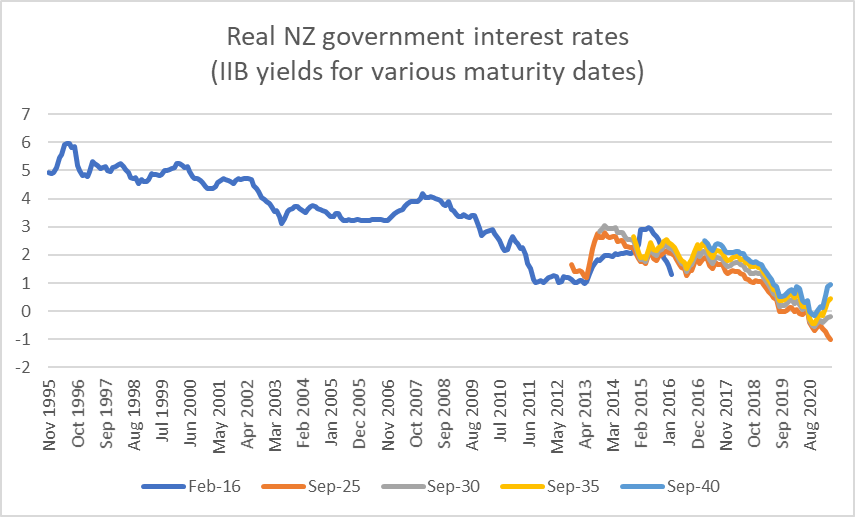

Finally, note that in the chart I have compared a 10 year bond yield to a one year inflation rate. But at least since 1995 we have had a direct read on real government bond yields through trading in government inflation indexed bonds. As this chart shows, the pattern over that period is very similar,

Developments in the last few months are interesting, but that is something for another day.

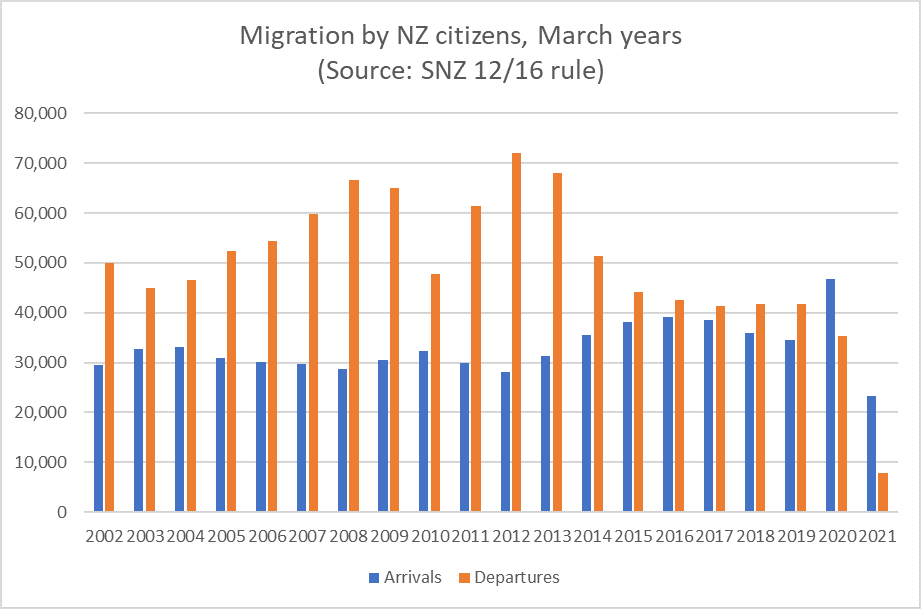

My second brief topic this morning was sparked by a strange quite-long article in the New York Times yesterday headed “New Zealanders are Flooding Home: Will the Old Problems Push Them Back Out”. A lot of work seemed to have gone into it, and some of the individual anecdotes were not uninteresting (and in the small world that is New Zealand, one of the recent returnees was even someone I’d once worked with) but…….no one (do they have factcheckers at the NYT?) seemed to have stopped and checked the numbers. It took about two minutes to produce this graph that I put on Twitter yesterday.

Using the official SNZ estimates, the problem with the story was that arrivals of New Zealanders had not really changed much at all – a bit higher than usual in the March 2020 year, and then lower than usual in the most recent year. There has, of course, been a big change in the net flow of New Zealand citizens but……..that is mostly the very steep fall in the number of New Zealanders leaving. That reduction – over the March 2021 year – is, of course, not surprising in the slightest given (a) travel restrictions to Australia for much of the year, and (b) travel restrictions and/or bad Covid in much of the rest of the world.

But, on official estimates, there simply is no flood of New Zealanders returning home. None.

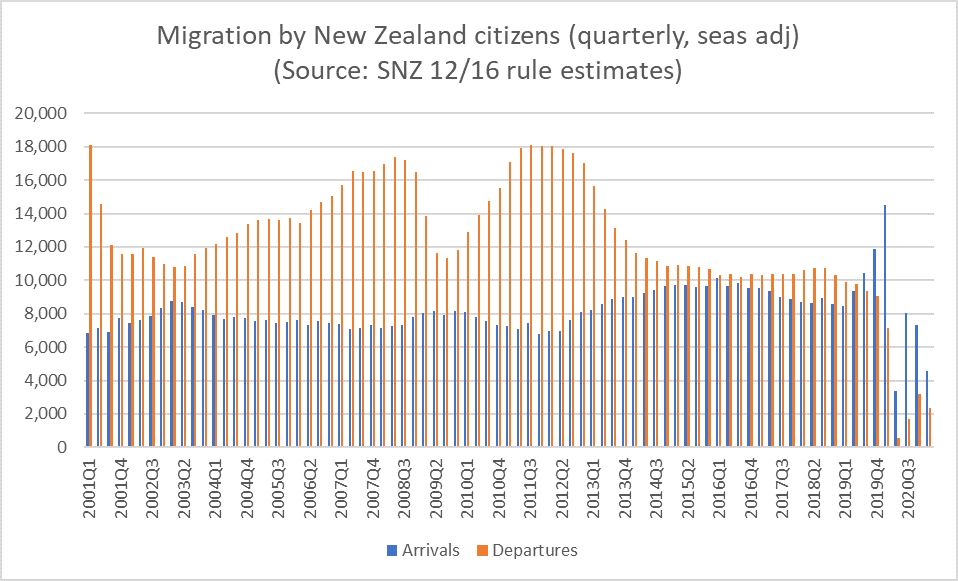

This morning I looked a little more closely, and dug out the quarterly (seasonally adjusted) version of the data.

It is, of course, much the same picture, but what surprised me a little was the upsurge in (estimated) arrivals back in late 2019, pre-Covid. Here it is worth remembering that until a couple of years ago our PLT migration data was based on reported intentions at the time of arrival, but the 12/16 approach now used looks at what actually happened. It looks as though some New Zealanders who had come to New Zealand in late 2019, probably not intending to stay, ended up doing so, voluntarily or otherwise, once Covid hit. So they are now recorded as migrant arrivals in late 2019 even though at the time they would not have thought of themselves as such.

But it does not change the picture: there is no flood, or even a little surge now, in returning New Zealanders. A problem with the 12/16 approach is that the most recent data is prone to quite significant revisions (and that is particularly a risk when the normal patterns the models use aren’t likely to be holding, but there is nothing to suggest there is a significant influx of returning New Zealanders happening.

There will be always be natives who’ve spent time abroad returning home. It happens even in rather poor and downtrodden countries, and it happens here – always has, probably always will. That adjustment isn’t always that easy, plenty of people often aren’t sure for a long time that they’ve made the right choice. Covid means a few different factors have influenced some of those choices for some people. But there is no “flood”, just a similar to usual (or perhaps now smaller than usual) number of returnees, coming back to a New Zealand of extraordinarily high house prices and productivity levels and incomes that increasingly lag behind a growing number of advanced economies. Those persistent failures – and the indifference of our main political parties – should be worth a story. But not the non-existent flood.