In my post yesterday about the Reserve Bank’s FSR and the subsequent press conference conducted by the Deputy Governor I included this

The sprawling burble continued with questions about whether banks should lend more to things other than housing – one veteran journalist apparently being exercised that a large private bank had freely made choices that meant 69 per cent of its loan were for houses. Instead of simply pushing back and noting that how banks ran their businesses and which borrowers they lend to, for what purposes, was really a matter for them and their shareholders – subject, of course, to overall Reserve Bank capital requirements – we got handwringing about New Zealand savings choices etc etc, none of which – even if there were any analytical foundation to it – has anything to do with the Bank.

Someone got in touch about the 69 per cent line and suggested that it must be a sign of something being wrong, going on to suggest that the Reserve Bank’s capital framework and associated risk weights was skewing lending away from agricultural and (in particular) business lending.

My summary response was as follows:

I guess where I would come close to your stance is to say that if we had a properly functioning land market producing price/income ratios across the country in the 3-4 range (as seen in much of the US, incl big fast-growing cities) then the share of ANZ’s loan book accounted for by housing lending would be much less than 69%, and in fact the total size of their balance sheet would be much smaller. But my take on that is that the high share of housing loans is largely a reflection of central and local govt choices that drive land prices artificially high, and then we need financial intermediaries for (in effect) the old to lend to the young to enable houses to be bought. The fault isn’t the ANZ’s and given the capital requirements in NZ there is little sign that the overall balance sheet is especially risky, and therefore should not be of particular interest to the RB (except perhaps in a diagnostic sense, understanding why balance sheets are as they are). I’m (much) less persuaded that there is a problem with the (relative) risk weights, given that every comparative exercise suggests that our housing weights are among the very highest anywhere (and, in effect, rising further in October).

But to elaborate a bit (and shift the focus from one particular bank) across the depository corporations as a whole (banks and non-banks) loans for housing are about 62 per cent of total Private Sector Credit (and total loans to households are about 64 per cent). A large chunk of the balance sheets of our financial intermediaries are accounted made up of loans for housing.

The gist of my response was that that shouldn’t surprise us at all, given the insanity of the land use restrictions that central and local government impose on us, rendering artificially scarce – and expensive – something of which there is an abundance in New Zealand: land. If, from the perspective of the economy as a whole, relatively young people are buying houses from relatively old people (or from developers) the higher house/land prices are the more housing credit there needs to be on one side of banks’ collective balance sheets and – simultaneously – the more deposits on the other. If median house prices averaged (say) $300000 – as they do in much of the (richer) US – there would be a great deal less housing credit in total.

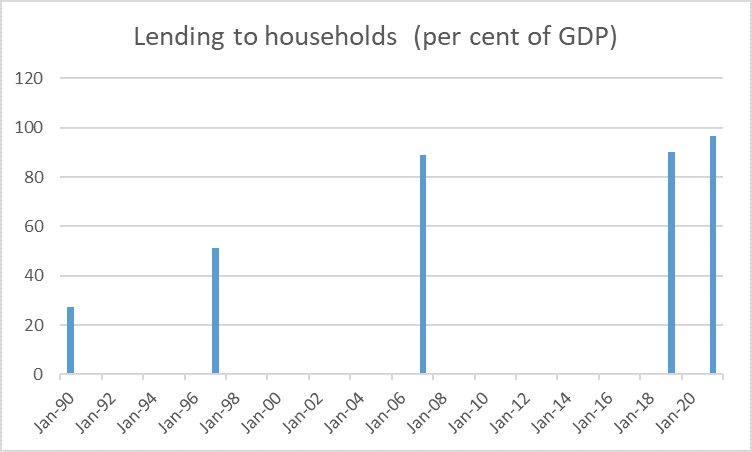

One other way to look at the stock of housing credit is to compare it to GDP – in effect, all the economic value-added in the entire country. Since the GDP series is quarterly and the credit data are monthly, I haven’t shown a full time series chart here. The data start from December 1990, and then only for an aggregate of housing+personal loans (but personal loans are small in New Zealand). So I’ve shown lending to households in Dec 1990, in mid-97 (roughly the peak of the business cycle), Dec 2007 and Dec 2019 (two more business cycle peaks), and March 21 (for which we have credit data, but only an estimate for GDP).

There was a huge increase in the stock of lending, as a share of (annualised) GDP over the first 17 years of the series. What I’ve long found interesting is how little change there was over the following full business cycle (there were ups and downs in between the dates shown), and then we’ve had a bit of a step up in the last year or so (and even if house prices stay at this level, future turnover will tend to further increase housing debt expressed as a share of GDP).

Since real house prices have more than tripled since 1990 it is hardly surprising the stock of housing debt (share of GDP) has increased hugely. Were real house prices to, for example, halve then we might over time expect to see the stock of housing debt drift gradually back – it could take decades – towards say the 1997 sort of number.

Implicit in the journalist’s comment was a suggestion that lending to housing somehow limits how much lending banks do for other things. That generally will not be so. Banks (as a whole) are generally not funding-constrained – not only do loans create deposits (at a system level) but international funding markets are available (and used to be very heavily used, when NZ had large current account deficits). Of course, there is only so much capital devoted to New Zealand banking at any one time, but in normal circumstances capital flows towards opportunities.

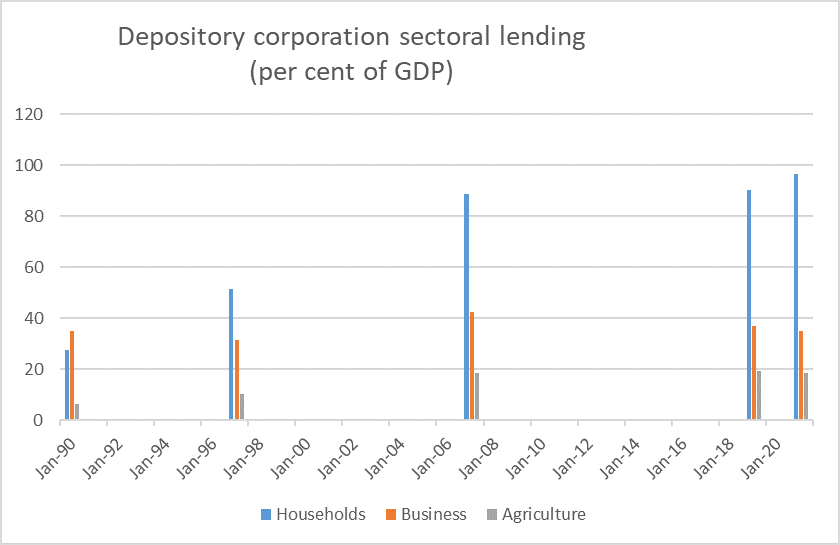

But what has the empirical record been? The Reserve Bank publishes data for business lending from banks/NBDTs (which isn’t all business borrowing by any means – between funding from parents and the corporate bond market) and for agricultural lending.

Here is how the full picture looks

For what it is worth, intermediated lending to business in March was exactly the same as a share of GDP as it was in December 1990. For younger readers, December 1990 was just a couple of years into banks working through the massive corporate debt overhang that had built up in the few years immediately following liberalisation. Farm credit, of course, has increased very substantially – again particularly over the years leading up to 2007/08 with the wave of dairy conversions and higher land prices.

On the business side of things, it is worth bearing in mind that business lending (share of GDP) was consistently weak throughout the last business cycle. Some will argue that banks had some sort of structural bias against business but even if so (a) over that decade or so there was no growth in the stock of housing lending as a share of GDP, and (b) there is little compelling evidence that systematic and large unexploited profit opportunities were going begging over that decade. It seems more likely that the markets – including banks – financed the profitable opportunities that were around, but there just weren’t many of them.

So my story remains one that if central and local government were to free up land markets and house price to income ratios dropped back to, say, 3-4 then over time the stock of housing debt (share of GDP) would shrink, a lot. There are some stories on which much cheaper house prices generate fresh waves of business entrepreneurship etc with workers able to flock to those opportunities, but I don’t find those stories convincing in New Zealand (in the aggregate). But simply repressing the financial system some more – the agenda the Reserve Bank and the government have been pursuing for several years now – will not change those business opportunities one iota.

(This post hasn’t tried to deal with the riskiness of the housing loans. My take on that is really the same as the Reserve Bank’s – at least when it isn’t champing at the bit to intervene. Capital requirements (and actual ratios) are high – materially higher than they were – and they are calculated in a fairly conservative way, with risk weights on housing that are fairly high, including by international standards. For what it is worth, the ratings issued by the agencies seemed aligned with that interpretation. )

That we have such a large share of total credit for housing isn’t, prima facie, a banking system problem – banks will follow the opportunities that (in this case) bureaucratic distortions create, and our central bank has demanding capital standards and in APRA one of the better banking regulators around – but rather just another indicator of how warped our housing market has been allowed – by governments – to become. But we knew that already. In fact, governments knew it to, but they prefer to try to paper over cracks, hide behind ever more pervasive RB controls, rather than tackle the core issue.

On which note, a couple of months ago the Wellington magazine Capital asked if I would contribute an article on what might be done to fix the housing market, with a Wellington focus. I wasn’t really familiar with the magazine – having previously seen it only in hairdressers, takeaway outlets and the like, for readers to glance through while they wait – but I said yes, and looking through the edition I picked up this week it looks like a mix of fairly geeky material (eg a whole article on lead-rubber bearings) and the lifestyle stuff.

Since I didn’t give them my copyright, many readers are out of Wellington. and the issue with my article seems to have been on sale for a while now here is the piece I contributed.

Free up the land: unravelling the unnatural housing disaster

Michael Reddell[1]

April 2020

New Zealand house prices, even adjusted for inflation, have more than tripled over the last 30 years. The persistent trend was unmistakeable even before the latest surges. Million-dollar houses were once the rare exception in Wellington, but now are almost the norm in too many suburbs. The Wellington region median house price is now perhaps 10 times median income, putting home ownership increasingly beyond the reach of an ever-larger share of those in their 20s and 30s.

Most of the talk is loosely about “house” prices but what has really skyrocketed is the price of land in and around our urban areas; whether land under existing dwellings, or potentially developable land. And this in a country with so much land that all our urban areas cover only about 1 per cent of New Zealand.

It is scandalous, perhaps especially because it is an entirely human-made disaster. Land isn’t scarce, and hasn’t become naturally much more scarce, even as the population has grown. Instead, central and local governments together have put tight restrictions on land use. They release land for housing only slowly and make it artificially scarce, not just in and around our bigger cities but often around quite small towns. And if there is sometimes a tendency to suggest it is “just what happens”, citing absurdly expensive (but much bigger) cities such as Melbourne, San Francisco or Vancouver, nothing about what has gone on is inevitable or “natural”.

The best way to see this is to look at the experience in the United States, where there are huge regions of the country – often including big and growing cities – where price to income ratios are consistently under 4. Little Rock, for example, is the state capital of Arkansas. It has a growing metropolitan population of just under 900,000, and a median house price of about NZ$300,000 – little changed, after allowing for inflation, over 40 years. The US also helps illustrate why it is wrong to (as many do) blame low interest rates: not only are interest rates the same in both San Francisco and Little Rock, but US longer-term real interest rates are typically a bit lower than those in New Zealand. The same goes for tax arguments: they have much the same tax code in both the high-priced growing US cities as in (much) more affordable ones. High real house prices are a policy choice; not necessarily the desired outcome of central and local government politicians, but the inevitable outcome of the land use restrictions they choose to maintain.

Both central and local government politicians sometimes talk a good game about making housing more affordable, but neither group seems to have grasped that in almost any market aggressive competition among suppliers is what keeps prices low. People sometimes suggest there isn’t enough competition among, for example, supermarkets or building products suppliers, but if we really want widely-affordable housing again in New Zealand what we need is landowners aggressively competing with each other to get their land brought into development. And that has to mean an end to local councils deciding where they think development should happen, whether within the existing footprint of a city or on its periphery. We need a presumptive right for owners to build, perhaps to two or three storeys, on any land (and, of course, councils need to continue to be able to charge for connecting to, for example, water and sewerage networks). It could be done now. That it isn’t tells us that councils are the problem not the solution. Too many – including in Wellington – seems to think it is their role to use policy so that in future lots of people are living in townhouses and apartments, even as experience suggests that what most (but not all) New Zealanders want, for most of their lives, is a place with a backyard and garden. And they seem to fail to understand that simply allowing a bit more urban density, perhaps in response to a build-up of population pressure, hasn’t been a path anywhere else to lowering house prices. Instead, such selective rezoning simply tends to underpin the price of those particular pieces of land.

Sometimes people suggest that even if this sort of approach would be viable in Hamilton or Palmerston North, it isn’t in rugged Wellington. But as anyone who has ever flown into or out of Wellington knows there is a huge amount of undeveloped land in greater Wellington. And if the next best alternative use should be what determines the value of land that could be used for housing, much of the land around greater Wellington simply does not have a very high value in alternative uses (not much of it is prime dairying or horticulture land). Unimproved land around greater Wellington should really be quite cheap, although the rugged terrain would still add cost to developing it to the point of being ready to build.

Some worry about, for example, the possibility of increased emissions. But once we have a well-functioning ETS the physical footprint of cities doesn’t change total emissions, just the carbon price consistent with the emissions cap. And for those who worry about traffic congestion, congestion charging is a proven tool abroad, which should be adopted in Wellington (and Auckland).

I’m not championing any one style of living. The mix between densely-packed townhouses and apartments on the one hand, and more traditional suburban homes on the other, shouldn’t be determined by the biases and preferences of politicians and officials but by the preferences of individuals and families, exposed to the true economic costs of those preferences. Similarly, policymakers should respect the (changing) preferences of groups of existing landowners what development can, or cannot, occur on their land.

The behaviour of councils over many years reveals them as, in practice, the enemies of the sort of widely-affordable housing which the market would readily provide (as it does in much of the US). If councils won’t free up the land, to facilitate the aggressive competition among land providers that would keep prices low, central government needs to act to take away the blocking power of local councillors.

And this need not be the work of decades. Of course, it takes time to build more houses, but the biggest single element of the housing policy failure is land prices. Once the land use rules look as though will be freed up a lot, expectations about future land prices will adjust pretty quickly, and prices will start falling. We could be the boutique capital city with widely-affordable housing. The only real obstacles are those who hold office in central and (especially) local government.

[1] Michael Reddell was formerly a senior official at the Reserve Bank, and also worked at The Treasury and as New Zealand’s representative on the board of the International Monetary Fund. These days, in additional to being a semi-retired homemaker, he writes about economic policy and related issues at http://www.croakingcassandra.com