The possibility of a sustained rise in the inflation rate (internationally and here) has been getting a lot of attention in the last few months. Note that I call it a “possibility” rather than a “risk”, because “risk” often has connotations of a bad thing and, within limits, a rise in the (core) inflation rate is something that should be welcomed in most advanced economies where, for perhaps a decade now, too many central banks have failed to deliver inflation rates up to the targets either set for them (as in New Zealand and many other countries) or which they have articulated for themselves (notably the ECB and the Federal Reserve). I’m not here engaging with the debate on whether targets should be higher or lower, but just take the targets as given – mandates or commitments the public has been led to believe should be, and will be, pursued.

Putting my cards on the table, I have been quite sceptical of the story about a sustained resurgence of inflation. In part that reflected some history: we’d heard many of the same stories back in 2010/11 (including in the countries where large scale asset purchases were then part of the monetary policy response), and it never came to pass – indeed, the fear of inflation misled many central banks (including our own) into keeping policy too tight for too long for much of the decade (again relative to the respective inflation targets). Central banks weren’t uniquely culpable there; in many places and at times (including New Zealand) markets and local market economists were more worried about inflation risks than central banks.

I have also been sceptical because, unlike many, I don’t think large-scale asset purchases – of the sort our Reserve Bank is doing – have any very much useful macroeconomic effect at all (just a big asset swap, and to the extent that there is any material sustained influence on longer-term rates, not many borrowers (again, in New Zealand) have effective financing costs tied to those rates). And if, perchance, the LSAP programme has kept the exchange rate a bit lower than otherwise, it is hardly lower than it was at the start of the whole Covid period – very different from the typical New Zealand cyclical experience. In short, (sustained) inflation is mostly a monetary phenomenon and monetary policy just hadn’t done that much this time round.

Perhaps as importantly, inflation has undershot the respective targets for a decade or so now, in the context of a very long downward trend in real interest rates. There is less than universal agreement on why those undershoots have happened, in so many countries, but without such agreement it is probably wise to be cautious about suggesting that this time is different, and things will suddenly and starkly turn around from here. At very least, one would need a compelling alternative narrative.

Having said that, there have been a couple of pleasant surprises in recent times. First, the Covid-related slump in economic activity has proved less severe (mostly in duration) than had generally been expected by, say, this time last year when some (including me) were highlighting potential deflationary risks. That rebound is particularly evident in places like New Zealand and Australia that have had little Covid, but is true in most other advanced countries as well where (for example) either the unemployment rate has peaked less than expected or has already fallen back to rates well below those seen, for example, in the last recession. Spare capacity is much less than many had expected.

And, in New Zealand at least, inflation has held up more than most had expected (more, in particular, than the Reserve Bank had expected in successive waves of published forecasts. The Bank does not publish forecasts of core inflation, but as recently as last August they forecast that inflation for the year to March 2021 would be 0.4 per cent (and that it would be the end of next year before inflation got back above 1 per cent). That was the sort of outlook – their outlook – that convinced me that more OCR cuts would have been warranted last year.

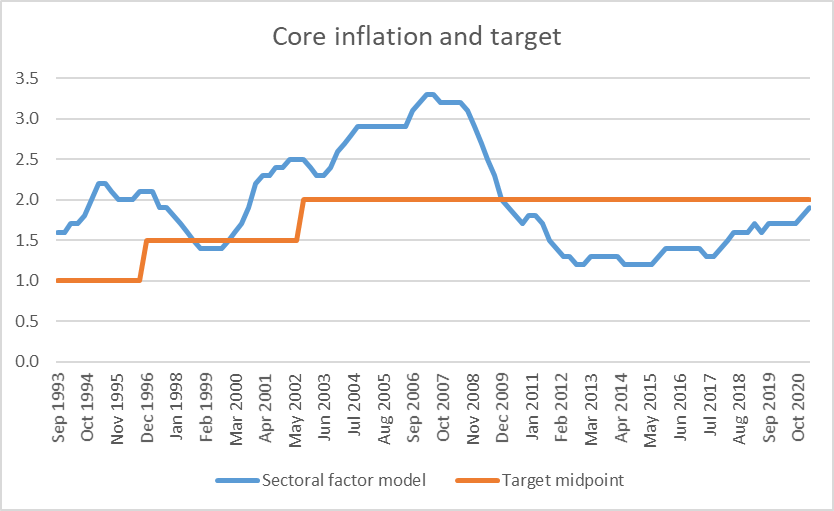

As it is, headline CPI inflation for the year to March was 1.5 per cent. But core measures are (much) more important, and one in particular: the Bank’s sectoral core factor model, which attempts to sift out the underlying trends in tradables and non-tradables inflation and combines them into a single measure: a measure not subject to much revision, and one which has been remarkably smooth over the nearly 30 years for which we now have the series – smooth, and (over history) tells a story which makes sense against our understanding of what else was going on in the economy at the time. This is the chart of sectoral core inflation and the midpoint of successive inflation targets.

It is more than 10 years now since this (generally preferred) measure of core inflation has touched the target midpoint (a target itself made explicit from 2012 onwards). With a bit of lag, core inflation started increasing again after the Bank reversed the ill-judged 2014 succession of OCR increases, but by 2019 it was beginning to look as if the (core) inflation rate was levelling-off still a bit below the target midpoint. It was partly against that backdrop that the Reserve Bank (and various other central banks) were cutting official rates in 2019.

The Bank’s forecasts – and my expectations – were that core inflation would fall over the course of the Covid slump and – see above – take some considerable time to get anywhere near 2 per cent. So what was striking (to me anyway) in yesterday’s release was that the sectoral measure stepped up again, reaching 1.9 per cent. That rate was last since (but falling) in the year to March 2010.

As you can, there is a little bit of noise in this series, but when the sectoral factor model measure of core inflation steps up by 0.2 percentage points over two quarters – as had happened this time – the wettest dove has to pay attention.

To be clear, even if this outcome is a surprise, it should be a welcome one. (Core inflation) should really be fluctuating around the 2 per cent midpoint, not paying a brief visit once every decade or so. We should be hoping to see (core) inflation move a bit higher from here – even if the Bank still eschews the Fed’s average inflation targeting approach.

Nonetheless, even if the sectoral factor model is the best indicator, it isn’t the only one. And not all the signs are pointing in the same direction right now. For example, the annual trimmed mean and weighted median measures that SNZ publishes – and the RBA, for example, emphasises a trimmed mean measure – fell back in the latest quarter. The Bank’s (older and noisier) factor model measure is still sitting around 1.7 per cent where it first got back to four years ago. International comparisons of core inflation tend to rely on CPI ex food and energy measures. For New Zealand, that measure dropped back slightly in March, but sits at 2 per cent (annual).

Within the sectoral factor model there is a non-tradables component – itself often seen as the smoothest indicator of core inflation, particularly that relating to domestic pressures (resource pressures and inflation expectations). And that measure has picked up a bit more. On the other, one of the exclusion measures SNZ publishes – excluding government charges and cigarettes and tobacco – now has an inflation rate no higher than it was at the end of 2019 and – at 2.4 per cent – probably too low to really be consistent with core inflation settling at or above 2 per cent (non-tradables inflation should generally be expected to be quite a bit higher than tradables inflation).

I think it is is probably safe to say that core inflation in New Zealand is now back at about 2 per cent. That is very welcome, even if somewhat accidental (given the forecasts that drove RB policy). As it happens, survey measures of inflation expectations are now roughly consistent with that. Expectations tend not to be great forecasts, but when expectations are in line with actuals it probably makes it more likely that – absent some really severe shock – that inflation will hold up at least at the levels.

But where to from here?

Interestingly, the tradables component of the Bank’s sectoral factor model has not increased at all, still at an annual rate of 0.8 per cent. All indications seem to be that supply chain disruptions and associated shortages, increased shipping costs etc will push tradables inflation – here and abroad – higher this year. But it isn’t obvious there is any reason to expect those sorts of increases to be repeated in future – the default assumption surely has to be that shipping, production etc gradually gets back to normal, perhaps with some price falls then.

And if one looks at the government bond market, participants there are still not acting as if they are convinced core inflation is going higher. If anything, rather the opposite. There are four government inflation-indexed bonds on issue, and if we compare the yields on those bonds with the conventional bonds with similar maturities, we find implied expectations over the next 4 and 9 years averaging about 1.6 per cent, and those for the periods out to 2035 and 2040 more like 1.5 per cent. Again, these breakevens – or implied expectations – are not forecasts, but they certainly don’t speak to a market really convinced much higher inflation is coming. One reason – pure speculation – is that with the Covid recession having been less severe than most expected, it isn’t unreasonable to think about the possibility of a more serious conventional recession in the coming years with (a) little having been done to remove the effective lower bound, and (b) public enthusiasm for more government deficits likely to reach limits at some point.

So I guess I remain a bit sceptical that core inflation is likely to move much higher here, even if the Reserve Bank doesn’t change policy settings. Fiscal policy clearly played a big role in supporting consumption last year but we are likely to be moving back into a gradual fiscal consolidation phase over the next few years. And if the unemployment rate is now a lot lower than most expected, it is still not really a levels suggesting aggregate excess demand (for labour, or resources more generally). For the moment too, immigration isn’t going to be providing the impetus to demand, and inflation pressures, that we often expect to see when the economy is doing well (cyclically). And if you believe stories about the demand effects of higher house prices – and I don’t- house price inflation seems set to level off through some mix of regulatory and tax interventions and the exhaustion of the boom (as in numerous previous occasions).

What should it all mean for monetary policy? Since I don’t think the LSAP programme is making much difference to anything that matters – other than lots of handwaving and feeding the narratives of the inflationistas who don’t seem to realise that asset swaps don’t create additional effective demand – I’d be delighted to see the programme canned. But I don’t think doing so would make much sustained difference to anything that matter either. So in a variant of one of the Governor’s cheesy lines, it is probably time for “watch, hope, wait”. The best possible outcome would be a stronger economic rebound, a rise in core inflation, and the opportunity then to start lifting the OCR. But there is no hurry – rather than contrary after a decade of erring on the wrong side, tending to hold unemployment unnecessarily high. And there is little or no risk of expectations – or firm and household behaviour – going crazy if, for example, over the next year or two core inflation were to creep up to 2.3 or 2.4 per cent.

But what of the rest of the world? I’ve tended to tell a story recently that if there really were risks of a marked and worrying acceleration in inflation it would be in the United States, where the political system seems determined to fling borrowed money around in lots of expensive government spending programmes.

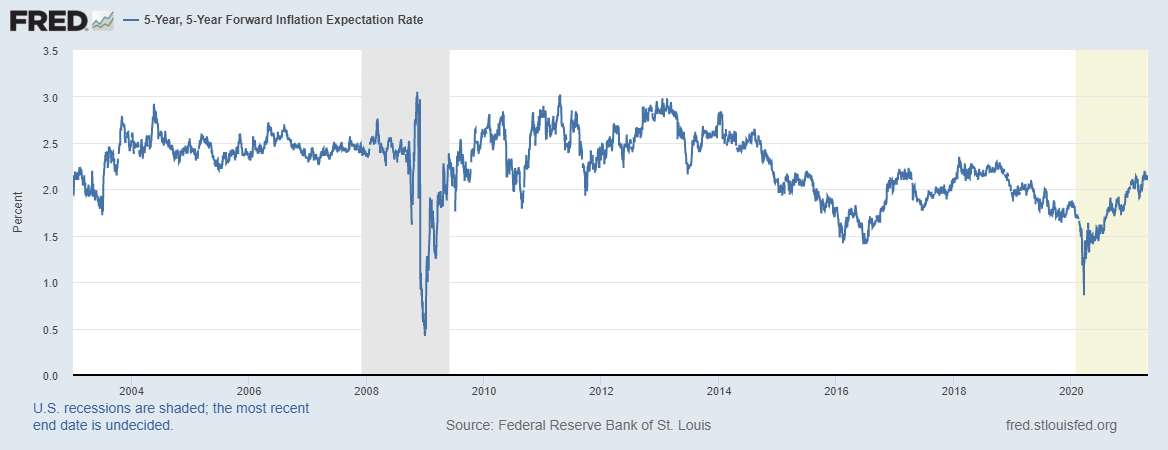

But for now, core inflation measures still seem comfortably below 2 per cent (trimmed mean PCE about 1.6 per cent). The Cleveland Fed produces a term structure estimate for inflation expectations, and those numbers are under 2 per cent for the next 28 years or so (below 1.7 per cent for the next 15 years). And if market implied expectations have moved up a lot from the lows last year, the current numbers shouldn’t be even remotely troubling – except perhaps to the Fed which wants the market to believe it will let core inflation run above 2 per cent for quite a while before tightening, partly to balance past undershoots. Here are the implied expectations from the indexed and conventional government bond markets for the second 5 years of a 10 year horizon (ie average inflation 6-10 years hence).

These medium-term implied inflation expectations are barely back to where they were in 2018, let alone where they averaged over the decade from about 2004 to 2014 – for much of which period the Fed Funds rate sat very near zero.

What of the advanced world beyond the US. It is harder to get consistent expectations measures, so this chart is just backward-looking. Across the OECD, core inflation (proxied by CPI inflation ex food and energy) has been falling not rising (these data are to February 2021, all but New Zealand and Australia having monthly data).

Are there other indicators? Sure, and many commodity prices are rising. And markets and economists have been wrong before and will – without knowing when – be wrong again. Perhaps this will be one of those times. Perhaps we’ve all spent too much time learning from the last decade, and forgetting (for example) the unexpected sustained surge in inflation in the 60s and 70s.

But, for now, I struggle to see where the pressures will come from. Productivity growth is weak and business investment demand subdued. Global population growth is slowing (reducing demand for housing and other investment). We aren’t fighting wars, we don’t have fixed exchange rate. And if interest rates – very long-term ones – are low, it isn’t because of central banks, but because of structural features – ill-understood ones – driving the savings/investment (ex ante) balance. For now, the New Zealand story is unexpectedly encouraging – inflation finally looks to be near target – but we should step pretty cautiously before convincing ourselves that the trends of the last 15 or even 30 years are now behind us, or that high headline rates – here and abroad – later this year foreshadow permanently higher inflation (or, much the same thing, higher required interest rates).

Thanks for this piece Michael, a pleasure to read as always.

I feel similarly to you. Commodity prices are one thing but let’s wait to see some sustained evidence of consumer inflation before we take away the punch bowl.

On Thu, 22 Apr 2021 at 2:56 PM, croaking cassandra wrote:

> Michael Reddell posted: ” The possibility of a sustained rise in the > inflation rate (internationally and here) has been getting a lot of > attention in the last few months. Note that I call it a “possibility” > rather than a “risk”, because “risk” often has connotations of a bad th” >

LikeLike

When I walk into Countdown and a 4kg bag of frozen Tegel chicken thighs are on discount at $18 per 4kg bag down from the usual $25 per 4kg, NZ is indeed the land of plenty and cheap. With the NZD rising now to $0.72 against the USD up from $0.66 pre covid not too sure why anyone thinks inflation is a risk or even a possibility?

LikeLike

” Note that I call it a “possibility” rather than a “risk”, because “risk” often has connotations of a bad thing and, within limits, a rise in the (core) inflation rate is something that should be welcomed in most advanced economies where, for perhaps a decade now, too many central banks have failed to deliver inflation rates up to the targets either set for them”

My main question is “what is it about inflation that you think is so good or to be welcomed?”

My understanding is that inflation *is* a bad thing. I thought that is why central banks were originally mandated to reduce inflation and keep it low. Surely the point of doing this wasn’t so commentators can fixate on an arbitrary number (apparently 2%). I thought the point was that low and stable inflation was intended by the legislators to to produce some economic good – it is not an end in itself – which seems to be how you approach it.

Because the Bank doesn’t “control” inflation it merely influences it the Bank was given a target range. Inflation that stays largely within the target range seems intuitively reasonable in terms of its mandate. Advocating for higher inflation makes no sense to me since the objective, I would hope, is that there be some economic benefit resulting from a the higher inflation. If there a benefit, what is it?

For example, generally, in terms of someone’s disposable income in principle they are happier if inflation is 1% than if it is 3%, unless the inflation is compensated for through higher wages – but this is uncertain probably lagged and isn’t necessarily going to be the case for many people. But then even if it is compensated, wouldn’t the sum result be that inflation has now made us less competitive? (We produce the same amount of output for higher cost?)

I could talk about increases in petrol, stratospheric price rises in some computing and electronic equipment, persistent huge increases in insurance costs, impending power price rises, and a host of other price rises well in excess of 3%. I agree the Bank should be looking through most of these and not risking what is looking like a fragile recovery, but I *am* trying to understand what it is about higher inflation that you consistently seem to present as something that is good or desirable, rather than harmful.

Finally, can I recommend this article, which raises some interesting points relevant to this and your previous post.

https://www.spectator.com.au/2021/04/dear-comrade-jacinda/

LikeLiked by 1 person

In lieu of a response from someone more educated than me – I see it’s been five days since you posted this and have not yet had an answer – my understanding of the benefit of higher inflation is to promote businesses to invest. If a business borrows money for an infrastructure upgrade, R&D, etc, their expectation is that, at bare minimum, the money they eventually pay back to the lender is worth less than what they borrowed it for, so inflation essentially earns a 2%pa return on investment (at the target rate of inflation). Conversely, a negative rate of inflation (or deflation) deters any investment, since the money paid back to the lender will be worth more in the future than it was when it was borrowed.

The target of 2% is intended to be a reliable and consistent indicator that investors can account for when deciding whether or not to invest. The infrastructure upgrade, R&D, etc they invest in intends to create jobs (which is a net benefit against the population having 2% less buying power), though I’d assume that the net benefit of job creation starts to erode when faced with significant consumer price increases at higher inflation (say, >8%), so a more modest, non-negative number (i.e. 2%) would be appropriate. As it’s notoriously hard to measure accurately, 2% gives a reasonable buffer over 0%, though it’s still a fairly arbitrary target (as opposed to a 1.5% or 3% inflation target).

If anyone has a better explanation, please do respond: I’d like to understand this better as well, if my answer is not accurate.

LikeLiked by 1 person

Sorry, I didn’t see your comment when it came in. I’m reluctant to go another round with you on this (we’ve done it numerous times before, often in what seems to me like quite an antagonistic tone). You will have noted in my post this explicit comment

“I’m not here engaging with the debate on whether targets should be higher or lower, but just take the targets as given – mandates or commitments the public has been led to believe should be, and will be, pursued.”

In other words, for better or worse, a 2% target midpoint and a requirement to focus on it was established by National in 2012, reaffirmed by Labour subsequently, having first become the effective midpoint under Labour in 2002. My personal preference would be for a lower target, centred on true zero CPI inflation, but only if the effective lower bound issues were dealt with.

LikeLiked by 1 person

Matt, it really is more to do with behaviour. If you as part of a wider population believe that next month, the price of your consumables will get a discount, you would wait until next month to buy your product because it is cheaper. If everyone is waiting for cheaper prices then nothing gets sold. That is why deflation slows investment because no one is buying there is no economy.

If there is an expectation that prices are stable and could rise then you would buy today rather than wait and have to pay higher prices. That is why some inflation 1% to 3% encourages buying and more buying equates to a buoyant and healthy economy.

LikeLiked by 1 person

[ deleted – MHR ] How long does she think it takes from issuing an exploration permit to (possibly) pumping gas into the network?? Does the weather have nothing to do with the ability of hydro stations to produce power?? [deleted – MHR ] I’m struggling to find anything to recommend this.

LikeLiked by 1 person

I am reluctant to, and very rarely do, withhold comments in part on or in full, but I don’t want outright abuse on here (in this case, of someone who is not even party to the comment thread).

LikeLiked by 1 person

The bus drivers are on strike tomorrow, the nurses still aren’t happy, the minimum wage is now $20 an hour. Building supplies are scarce and everyone seems to be wanting work done on their house, etc. Seems to be plenty of inflationary signs to me?

LikeLike

I see the bus drivers have now been locked out, so we could be in for quite a standoff. But I guess both groups are really public sector employees (directly or indirectly) and I’m not sure there is much evidence of increased private sector wage inflation.

There are all sorts of odd shortages – my son’s computer battery was near death the other day, and for a pretty std model it was going to be 3 weeks to get a new one – but it will be interesting to see how generalised any inflation pressures become. I’m not dogmatic – esp having been v pessimistic last year, and surprised – but really only time will tell,

LikeLike

Inflation is and always has been a slow motion device designed to transfer wealth to the state. Purchasing power decreases and the incentives to save and then to invest in production are hampered.

Inflation statistics are derived from a set of approved inputs (nothing allowed that might embarrass the great state policymakers). The general level of prices is merely a statisticians tool of thought.

Fiscal policy settings by this interventionist government have completely warped the choices of investments between different types so much so that prices are not so much a discovery in a free market but a manipulation in a bubble. The market will have its way even full on socialism will not save us from the next depression. Debating inflation is just fiddling while rome burns.

LikeLike

In your last sentence you could probably exchange inflation for wellbeing, equity, diversity, climate change, sustainability, etc!

LikeLike

Hi

I think you have to put construction and housing aside. Plainly in these we are already hitting capacity and inflation following. However there is plenty of capacity everywhere else in the economy. This is a worldwide thing.

Uber is an example where you can now get a taxi in 3 or 4 minutes. It used to take an hour at peak times. If you ask them they always want more work. So even though it might seem like 3-4 minutes is unsustainable if anything it could get quicker. The supply chain for most consumable things is highly elastic. World suppliers can kick in easily. Stock is monitored on computers.

There is hidden productivity ie there are gains that would come if there was demand but there is no demand to measure it. This is why inflation is at bay and it will stay that way. I think any rise will peter out. It no longer matters about excess money so much as it did before. Consumers simply find they can buy what they need when they need it at the same price tomorrow.

LikeLike

Watched a bicyclist trying to fight with a Uber driver on a Queen St intersection because he believed that a bus lane restriction at the traffic light intersection means that a Uber car should not have stopped there and that he had right of way. No wonder dumb and stupid cyclists get killed when they demand right of way against a car.

LikeLike

‘And if you believe stories about the demand effects of higher house prices – and I don’t’

I’m not sure which country you’re living in but here in NZ since the lockdown every single thing that isn’t bolted down has sold for ever increasing prices, pretty much every single home owning Kiwi has borrowed against their increasing ‘home equity’ and then bought anything and everything, the demand for dirt bikes, boats, used cars, caravans and practically everything else is unprecedented in all of recorded history.

Only an economist could miss it. A work mate started a caravan importing business in the middle of COVID and thought it was the works time possible to have done so. He’s now sold over 70 and they are not cheap. Everyone I talk to that was around in ’87 say that this reminds them of the peak of the boom, the spending simply has not ever before happened like this, not even close. If it’s not debt driven, mostly demand effect from higher house prices then I’d love to know what it is because money not being spent on overseas holidays doesn’t cut it…

While true inflation (not carefully manipulated stats) is through the roof in NZ now, well over 10%, I agree with your outlook longer term but for a reason you don’t mention. DEBT. The massive crushing debt load that Kiwis are under – has to be deflationary, just a tiny tick up in rates and down they come to their knees.

Yes QE is an asset swap, but the money printing is done by the government issuing new bonds – that’s the inflationary part. If it isn’t then can they issue a trillion dollars worth all bought by the Reserve bank and spend it all next week and no inflation??

LikeLike

Not to get into a long debate, but your observation about people who do own homes does not give any weight to the many who do not own a home and now find themselves that much poorer- further out of the market – than they had previously thought (let alone the many like me for whom a freehold house is a place to live and the market value makes not a jot of difference to my consumption spending). But the issue is debated empirically: my take on it some years ago was here https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Bulletins/2011/2011dec74-4deveirmanreddell.pdf?revision=dec461f2-33a1-43c7-a79b-8c35d2517d36

LikeLike

Yes but one persons spending is anothers income. It makes no difference to your consumption as you are not living on a debt rat wheel. Extend the average kiwis credit card by 10k and you have 10k more spent the next day!

LikeLike

Rob, 67% of NZ households have low or no debt. Only 33% of NZ households have High debt. NZ households have $1.2 trillion in assets with only $200 billion in debt. The other $300 billion is business, commercial building and farming debt. NZ household debt is actually very very low.

LikeLike

The money being spent overseas usually is $11 billion a year. That money is now being spent in NZ. For example, I would usually spend $45,000 on a overseas holiday each year. I now have $45,000 spare cash from last year so I have been spending on Healthy homes upgrades on my investment properties which I would have borrowed if not for the Covid19 lockdown. This year another $45,000 spare cash is fast accumulating.

LikeLike

Air NZ pre covid was a $4 billion company. Today it would lucky to get crack $100 million. A large chunk of that $11 billion is air and.cruiseship transport, getting from NZ to Europe and other travel destinations.

LikeLike

Thanks. Read a bit about the 70s inflation and seems some link this period to inflation risk today: out of interest, how do you think about the major differences between now and then that fuzzy a direct comparison?? e.g public enthusiasm for more government deficits

LikeLiked by 1 person

I temember the 70s and would like to know what was different then that caused high inflation in the UK.

The inflation that ate my savings in the 70s is a bigger motivating force for my buying property today than even the embarassing unearned income made on the two ‘investment’ properties I bought 15 years ago in Auckland. I am an accidental millionaire. Spent the afternoon browsing properties online because my daughter is planning to enter the Auckland property market.

LikeLike

There was no Made in China with mega factories in the 70s.

LikeLike

So making things cheaper killed inflation. But why has it stayed dead?

LikeLike

Global competition with mega factories Made in Vietnam, Made in India, Made in Cambodia, Made in Malaysia etc providing cheap labour. This global competition forces increasing use of industrialised AI robots to replace human labour. Eg US and European factories compete with China with a significant investment in robots. Also China’s Silk road initiatives is about increasing access to markets and very simply economies of scale. The more you produce, the cheaper the product.

LikeLike

At a global level demographics was one things (lots of baby boomers in the family formation stage, needing housing), perhaps even a couple of decades of v strong productivity/income growth (lifting demands for better houses, public infrastructure etc). Demand for investment spending was high and supply of savings wasn’t – a recipe for higher neutral interest rates, The Vietnam War, and a Fed that allowed itself to be under the thumb of Johnson and Nixon clearly didn’t help, and neither did a fixed exchange rate regime – which meant other countries tended to import what the US did. Phillips curve thinking – in the med-term – must have been an issue, and linked to that a real reluctance to pay much (temporary) unemployment price to get inflation back down again (prob more so in NZ, where post-war U was so low, but it generalised). A sharp slowing in global productivity growth only aggravated things, so the system wasn’t delivering rapid increases in living stds any longer.

Quite a mix in other words. There is no guarantee that this time will be different, but it helps that people still have these discussions (in much of the West in the late 60s there had been no history of sustained higher peacetime inflation in the living memory of the public or most decisionmakers – true of all the Anglo countries, altho less so for France where the 20s were as recent then as the 70s/80s are to us now).

LikeLike

My intuition (for what it is worth) is that inflation (including price increases of a more structural kind) is not going away

And every uptick in inflation moves real after-tax interest rates even more negative

Not a happy dynamic

LikeLike