Bernard Hickey – fluent and passionate left-wing journalist – had a piece out the other day headed thus

with a one sentence summary

TLDR: Put simply, the sort of true independence enjoyed by the Reserve Bank of New Zealand as it pioneered inflation targeting for the last 30 years is now over, and that’s a good thing.

I found it a strange piece on a number of counts, and I say that as someone who (a) does not think financial regulatory policy (as distinct from the implementation and enforcement of that policy) should be handed over to independent agency, and (b) is probably less compelled now than most macroeconomists by the case for operational independence for monetary policy. So I’m not responding to Hickey’s piece to mount a charger in defence of central bank independence. Mostly I want to push back against what seems to me quite a mis-characterisation of the effect of the Robertson Reserve Bank reforms – those already legislated, those before the House now, and those the government has announced as forthcoming. But also about the responsibility of central banks for the tale of woe Hickey sets out to describe.

It is worth remembering that, by international standards, the Reserve Bank’s monetary policy independence – de facto and de jure – was always quite limited by international standards. Under the 1989 Act the Minister and the Governor jointly agreed the target, but every Governor largely deferred to the Minister in setting – and repeatedly changing – the objective, even if details were haggled over. And with a fairly specific target, and explicit power for the Governor to be dismissed for inadequate performance relative to the target, it was a fairly constrained (operational) independence. The accountability proved to be weaker that those involved at the start had hoped, but it could have been used more.

The monetary policy parts of the Act were overhauled in 2018. There were some good dimensions to that, including making the Minister (alone) formally responsible for setting the monetary policy targets. The Minister got to directly appoint the chair of the Bank’s (monitoring) Board. And a committee was established by statute to be responsible for monetary policy operational decisions. But setting up the MPC didn’t change the Reserve Bank’s operational independence, and if it had been set up well could even have strengthened it de facto over time. The Minister did not take to himself the power – most of his peers abroad have – to directly appoint the Governor or any of the other MPC members. As it is, the reforms barely even reduced the power of the Governor – previously the exclusive holder of the monetary policy powers – who has huge influence on who gets appointed to the MPC (three others are his staff) and who got the Minister to agree that no one with any ongoing expertise in monetary policy and related matters should be appointed as a non-executive MPC members. Oh, and got the Minister to agree that the independent MPC members should be seen and heard just as little as absolutely possible (unlike, say, peers in the UK or the USA).

Hickey cites as an example of the reduced independence the Bank’s request for an indemnity from the Minister of Finance to cover any losses on the large scale asset purchase programme the Bank launched last March. I’d put it the other way round. The Bank did not need the government’s permission to launch the LSAP programme – indeed it is one of the concerns about the Reserve Bank Act that it empowers the Bank to do things (including fx intervention and bond buying) that could cost taxpayers very heavily with no checks or effective constraint. It seemed sensible and prudent of the Bank to have sought the indemnity, partly to recognise that any losses would ultimately fall to the Crown anyway. Operational independence never (should meant) operational license, especially when (unusually) the Bank is undertaking activities posing direct financial risk to the Crown. (And I say this as someone who thinks that the LSAP programme itself was largely pointless and macroeconomically ineffectual.)

What about the other reforms? I’ve written previously about the bill before the House at present, which is mostly about the governance of the Bank. It will make no difference at all to the Bank’s monetary policy operational independence (although increases the risk that poor quality people are appointed in future to monetary policy roles). That bill transfers most of the Governor’s remaining personal powers to the Board. The Minister will appoint the Board members directly (unlike the appointment of the Governor) but even then the Minister will first be required to consult the other political parties, so it is hardly any material loss of independence for the Bank. The Minister will, in future, be required to issue a Remit for the Bank’s uses of its regulatory powers – and we really don’t know what will be in such documents – but those provisions don’t even purport to diminish the Bank’s policy-setting autonomy (notably since it is much harder, probably not sensibly possible, to pre-specify a financial stability target akin to the inflation target).

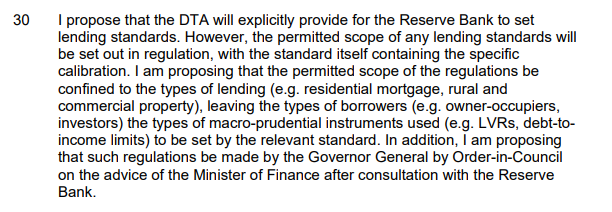

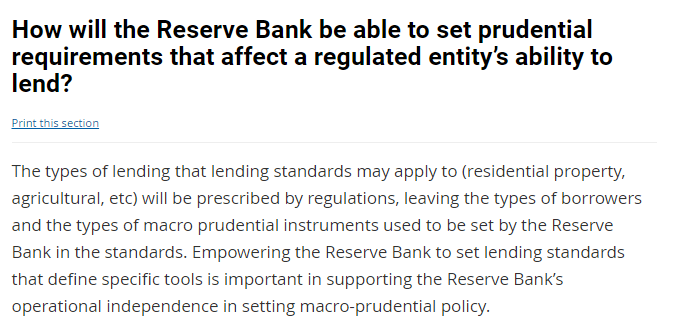

Details of the next wave of reforms were announced last week. Of particular note is the provisions around the standards that the Bank will be able to issue setting out prudential restrictions on deposit-takers, including banks. I wrote about that announcement last week. Since then more papers, including the (long) Cabinet papers and an official sets of questions and answers has been released. We do have the draft legislation yet, so things might change, but as things stand it is clear that what the government is proposing will amount to no de facto reduction in the Bank’s policymaking autonomy, and only the very slightest de jure reduction.

Why do I say this? At present, the Bank regulates banks primarily by issuing Conditions of Registration (controls on non-bank deposit-takers, mostly small, are set by regulation, which the Minister has control over). Under the new legislation is proposed that Conditions of Registration will be replaced by Standards, which will be issued (solely) by the Bank, but will be subject to the disallowance provisions that are standard for regulations via theRegulations Review Committee. In between the Act (which will specify – loosely, inevitably – objectives and principles to guide the use of the statutory powers) and the Standards, the Minister will be given the power to make regulations specifying the types of activity the Bank can set standards for. Note, however, that empowering the Bank to set standards in particular areas does not compel the Bank to do so (in practice, it is likely to be a simultaneous process)

There was initially some uncertainty about how specific the Minister could get – the more specific, the more effective power the Minister would have. But the Cabinet paper removed most of the doubt.

Backed up in the relevant text of the official questions and answers released on The Treasury’s website.

That isn’t very much power for the Minister at all; in effect nothing at all in respect of housing lending (since once the new Act is in force the Minister will simply have to regulate to allow a Standard on residential mortgage lending, if only to give continuing underpinning to LVR restrictions). Perhaps what it would do is allow a liberalising Minister to prevent the Bank setting specific standards for specific types of lending but……that doesn’t seem like the Labour/Robertson approach. And once a Minister has allowed the Bank to set standards for residential lending, the Minister will have no further say at all: the Bank could ban lending entirely to particular classes of borrowers, ban entirely specific types of loans, impose LVRs, impose DTI limits, perhaps impose limits of lending on waterfront properties (we know the Governor’s climate change passion). For most practical purposes it is likely to strengthen the independence of the Bank to make policy in matters that directly affect firms and households, with few/no checks and balances, and little basis for any formal accountability. Based on this government’s programme, the age of central bank policy-setting independence is being put on more secure foundations (since the old Act never really envisaged discretionary use of regulatory policy, which crept in through the back door).

Hickey argues that the introduction of LVR controls in 2013 by then-Governor Graeme Wheeler required government consent. In law, it never did. If the law allowed LVR controls – a somewhat contested point – all the power rested with the Governor personally. It may have been politically prudent for the Governor to have agreed a Memorandum of Understanding with the Minister on such tools, but he did not (strictly) have to. At best, it was a second-best reassertion of some government influence of these intrusive regulatory tools.

Now perhaps some will argue that there might be something similar in future too: the Minister might have no formal powers, but any prudent central bank might still seek some non-binding agreement with the government. But I don’t believe that. If the government had wanted any say on whether, say, DTI limits were things it was comfortable with, or what sorts of borrowers they might apply to, the prudent and sensible approach would be to provide explicitly for that in legislation. The old legislation may have grown like topsy, but this will be brand new legislation. The Minister is actively choosing to opt out and given the Bank more policy-setting independence (including formally so for non-banks) on the sorts of matter simply unsuited to be delegated to an independent agency, that faces little effective accountability (see the table from Paul Tucker’s book in last week’s post).

Whether independence should be strengthened or not, the Ardern/Robertson government has announced plans that will do exactly that, while at the same time weakening the effective accountability of the Bank (since powers will be diffused through a large board, with no transparency about the contribution of individual members).

That was a slightly longwinded response to the suggestion that actual central bank independence (monetary policy or financial regulation) is being reduced, in practice or by this goverment’s reforms. I favour a reduction in the policymaking powers of the Bank around financial regulation (the Bank should be expert advisers, and implementers/enforcers without fear or favour, not policymakers – the job we elect people to do).

What about monetary policy. Hickey reckons not only (and incorrectly so far) that monetary policy operational independence has been reduced, but that it should be reduced.

As it happens, I’m now fairly openminded on the case for monetary policy operational independence. One can mount a reasonable argument – as Paul Tucker does – for delegation to an independent agency (since a target can be specified, there is reasonable agreement on that target, there is expertise to hold the agency to account etc). But it has to be acknowledged that much of the case that was popular 30 years ago – that politicians could not be trusted to keep inflation down and would simply mess things up on an ongoing basis – is a lot weaker after a decade in which inflation has consistently (in numerous countries) undershot the targets the politicians (untrustworthy by assumption) set for the noble, expert and public-spirited central bankers.

What I’m not persuaded by is any of Hickey’s case for taking away the operational autonomy. Five or six years ago, I recall him – like me – lamenting that New Zealand monetary policymakers were doing too little to get the unemployment back down towards a NAIRU-type rate (it lingered high for years after the recession) and core inflation back up to target. But now, when core inflation is still only just getting back to target, unemployment is above any estimate of the NAIRU (notably including the Bank’s) Hickey seems to have joined the “central banks are wreaking havoc, doing too much etc etc” club.

One can debate the impact of the Bank’s LSAP programme. Personally, I doubt it has any made material useful macroeconomic contribution over the last year (good or ill – I don’t think it has done anything much to asset prices generally, and not that much even to long bond prices), and as I’ve argued previously it has mostly been about appearing active, allowing the Governor to wave his hands and say “look at all we are doing”. But even if you believe the LSAP programme has been deeply detrimental in some respect or other – Hickey seems to be among those thinking it plays a material part in the latest house price surge (mechanism unclear) – why would anyone suppose that a Minister of Finance running monetary policy last year would have done anything materially different to what the Bank actually did. After all, as Hickey tells us the Minister did sign off on the LSAP programme anyway, and a decisionmaking Minister of Finance would have been advised primarily by…..the Reserve Bank and the Treasury (and recall that the Secretary to the Treasury sits as a non-voting member of the MPC, and there has been no hint that Treasury has had a materially different view).

I think the answer is that Hickey favours a much heavier reliance on fiscal policy – even though he laments, and presents graphs about, how much additional private saving has occurred in many advanced economies in the last year, the income that is being saved mostly have resulted from….fiscal policy. Again, I think the answer is that he wants the government to be much more active in purchasing real goods and services – not just redistributing incomes. I suppose it comes close to an MMT view of the world.

But again there is little sign of anyone much – not just in New Zealand but anywhere – adopting this approach, or even central bank independence being restricted in other countries (what there is plenty sign of is central bankers getting out of their lane and into all sorts of trendy personal agendas – be it climate change (non) financial stability risks, indigenous networks or whatever.

None of this agenda seems to add up when it comes to events like those of the last 15 months. We know that monetary policy instruments can be activated, adjusted, reversed almost immediately. We know that governments are quite technically good at flinging around income support very quickly. But governments – this one foremost among them – are terrible at, for example, wisely using money to quickly get real spending (eg infrastructure) going in short order, and such projects once launched are hard to stop or to adequately control. Monetary policy is simply much much better suited to the cyclical stabilisation role.

Hickey is a big-government guy, and there are reasonable political arguments to have about the appropriate size and scope of government, but they haven’t got anything much to do with stabilisation policy – and nor should they. One doesn’t want projects stopped or started simply for cyclical purposes – brings back memories of reading of how the Reserve Bank wasn’t able to build its building for a long time because the governments of the day judged the economy overheated.

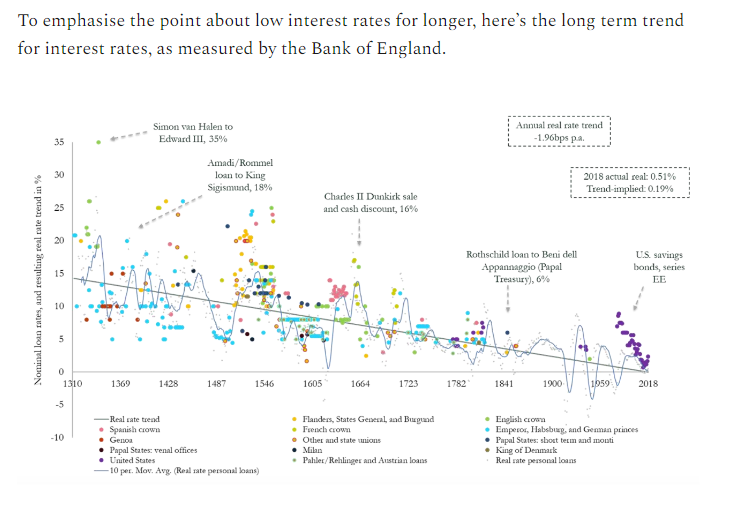

The (unstated) final part of his story seems to relate to a view that perhaps monetary policy has reached its limits. It would be a curious argument, given that much of his case seems to rest of the damage monetary policy is doing (impotent instruments tend to be irrelevant, even if deployed). He repeat this, really nice, long-term Bank of England chart

The centuries-long trend has been downwards, and many advanced country rates are either side of zero. But interesting as the chart genuinely is, including for questions about the real neutral interest rate (something monetary policy has little or no impact on), it tells one nothing about (a) who should be the monetary policy decisionmaker, or (b) the relative roles of fiscal and monetary policy. After all, the only reason why nominal interest rates can’t usefully go much below zero yet is because of regulatory restrictions and rules established – in much different times – by governments and central banks. Scrap the unlimited convertibility at par of deposits for bank notes – not hard to do technically – and conventional monetary policy (the OCR) immediately regains lots more degrees of freedom, able to be used – easily and less controversially – for the stabilisation role for which is it the best tool.

To end, I wouldn’t be unduly disconcerted if the government were to legislate to return to a system in which the Bank advised and the Minister decided on monetary policy matters. It might just be an additional burden for a busy minister, but it would be unlikely to do significant sustained harm (and one of the lessons of the last 30+ years is that central bankers and ministers inhabit the same environment, have many of the same ideological preferences etc) in a place like New Zealand. But to junk monetary policy as the primary cyclical stabilisation tool really would be to toss out the baby as well as the bathwater, no matter how big or active you think government tax and spending should be.