Eastern and central Europe don’t get much coverage in the New Zealand media, or in New Zealand economic analysis. But I’m intrigued by the region. There are multiple levels to that – religion, other dimensions of culture, battles in two world wars, decades of Soviet repression, and so on. But what really plays on my mind is that these countries regained their freedom, and the hope that came with that, at much the same time that many senior and influential people here (and young economists like me) were convincing themselves that New Zealand had passed a turning point and our economic prospects really would be looking up.

Here there had been the famous jibe from David Lange, comparing New Zealand’s economy pre-1984 to a Polish shipyard. At one level of course, it was a ridiculous claim, which trivialised the evils – and rank inefficiency – of Communism. But it had also captured something about the mood for change, partly in reaction to the plethora of controls the New Zealand economy had laboured under for decades. Actually, New Zealand had been been liberalising for decades, but (generally) rather slowly and inconsistently. And our living standards relative to those in other advanced countries had been dropping for several decades; the inefficiencies the heavy protectionism etc created were compounded by our worst terms of trade for a very long time. Daft interventions like the Think Big energy projects just reinforced the sense of something having gone very wrong.

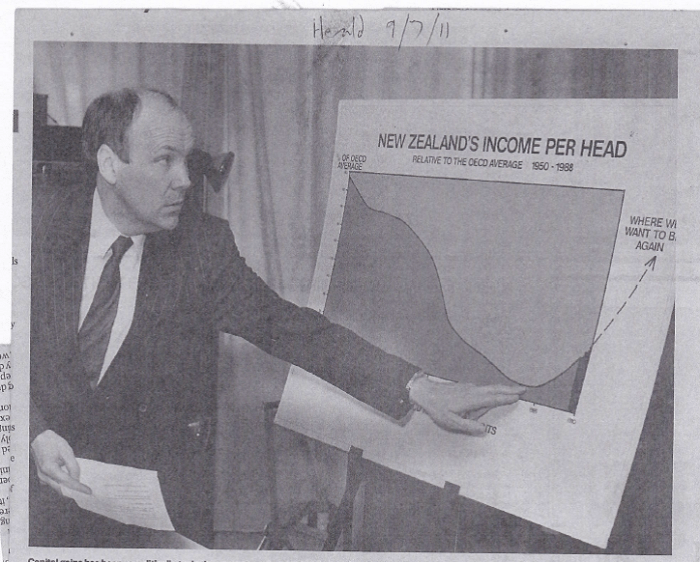

And so, over 10 years or so, there was a dramatic – at times almost frenzied – period of far-reaching economic and institutional reform. Much of it was admired – even envied – abroad, at least among the like-minded. Outfits like the OECD and IMF praised the reforms, and typically had a few more to suggest, and there really was a belief that nothing much now stood in the way of reversing the decades of relative economic decline. Productivity growth would, it was assumed, follow smart economic reforms much as night follows day. There are some people from that era who will now dispute that anyone seriously expected that sort of improvement, but David Caygill was the (very capable) Minister of Finance, and here is how he illustrated the story.

No sense there that the reforms – which were extended further by his successors – would simply slow our relative decline.

At the time, I was heavily involved in the Reserve Bank’s (small) part in all this – achieving and maintaining low and stable inflation. Medium-term growth and productivity issues weren’t our focus, but a couple of colleagues – including then deputy chief economist Arthur Grimes – had been doing some work on exactly those issues. Their findings were published in mid-1990. Having established the nature of New Zealand’s relative decline, and identified some of the possible causes (including, in their view, past rapid population growth) they ended their article this way.

And at around the same time, eastern and central Europe was regaining its freedom. The Berlin Wall fell, democratic governments were elected in Poland and Czechoslovakia, the Baltic states regained independence, a place like Slovenia emerged peacefully from what was left of hitherto communist Yugoslavia and so on. They were great days for the cause of human freedom. But also of economic opportunity. The former eastern bloc countries didn’t have identical economies, and it isn’t as if there hadn’t been economic progress even during the Communist years. Some – notably Hungary – had started reform and economic liberalisation earlier than others. But each of them had highly distorted economies, typically insecure property rights, and little in the way of a proper financial system. Data from this period are pretty patchy – especially for the countries that had been part of other countries up until then – but these countries weren’t dirt-poor: the better of them probably had GDP per hour worked in 1990 similar to, say, that in Korea. They were middle income countries. Then again, as far as we can tell, in say the 80 years prior to World War Two none of them had ever been much better than middle income countries either. Certainly, they’d nothing like the productivity, GDP per capita, or material living standards of New Zealand.

So if we go back 25 years or so, both in New Zealand and in eastern Europe those leading the economic reforms, and those running governments, had serious aspirations of catching up with the richer and more productive advanced countries. Of course, the mess in eastern Europe was a whole lot bigger than the mess here. In both countries, unwinding controls and protectionist structures involved short-term losses of output. Those were moderate here, but savage in some of the eastern European countries. But in both places there seemed to be great opportunities for catch-up and convergence.

I illustrated the other day how poor our productivity performance has been relative to the other advanced OECD countries over that period. From a starting point in 1989, productivity levels have slipped another 12 per cent further behind the median advanced OECD country. In other words, no convergence has happened at all. That has been so even over the last decade or so when productivity growth in the the “frontier” countries has itself slowed, which might have been an opportunity for some catch-up when we were starting so far behind.

But how do we compare with the eastern European countries? Seven of them – the Czech Republic, Estonia, Hungary, Latvia, Poland, Slovakia, and Slovenia – are now in the OECD, and thus in the OECD statistical databases. One other – Lithuania – isn’t in the OECD but has apparently reached data standards that mean the OECD is reporting their productivity data. There are other countries not covered – from Belarus or Moldova at the bleak extreme, to EU countries such as Bulgaria, Romania (which I wrote about here), and Croatia at the other. There is good data for some of them in other databases, but for today I just wanted to use the same OECD database Steven Joyce was using the other day in talking up New Zealand’s performance.

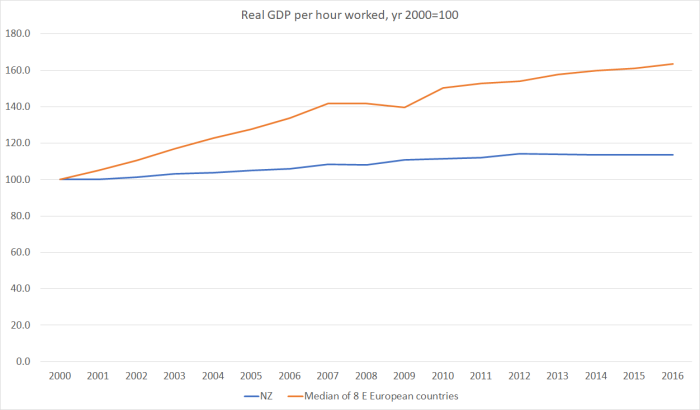

The OECD data on real GDP per hour worked for these countries starts in various years during the 1990s. 2000 is the first year for which there is data on all eight eastern European countries. In a way, it is a shame not to be able to start from the late 1980s, as I did in comparing us with the more advanced OECD countries. On the other hand, by 2000 the worst of the immediate post-communist disruption was well behind these countries (as the initial output losses in our own structural reforms were behind us). Sixteen years since 2000 (annual data is available to 2016) is a reasonable run of time to see how we’ve done relative to them – and neither the initial year nor the most recent year is muddied by recessions or financial crises. Each country has had a recession during this period, and in some cases they were pretty wrenching adjustments, involving IMF support.

Here is the cumulative real productivity growth for each of those countries, and New Zealand, since 2000.

The country with the slowest growth – Slovenia – managed twice the productivity growth of New Zealand over this period, and the OECD estimates suggest that the level of productivity in Slovenia – 30 years ago a province of a communist non-market country – is now approximately equal to that in New Zealand.

And here is the time series: the level of productivity in each country is indexed to 100 in 2000 and then I’ve taken a median of the eight eastern European countries.

You can see that the downturn in 2008/09 was much more severe for many of these countries (especially the ones running semi-fixed or hard-fixed exchange rates).

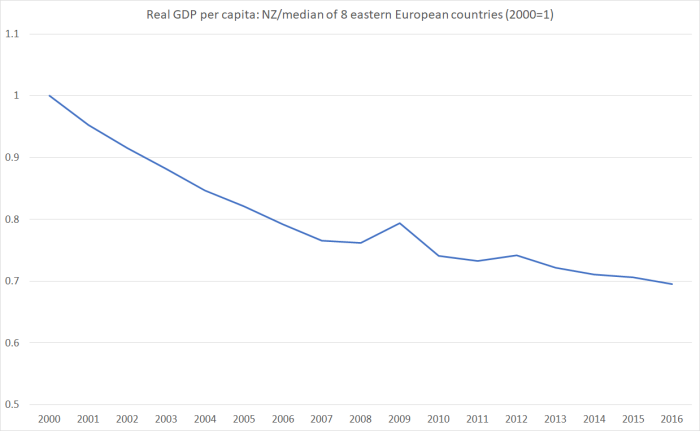

And here is the ratio of those two series.

Our rate of decline, relative to the eastern European countries, might slowed a little in the last decade, but there is no sign of things levelling out.

And if defenders of New Zealand’s performance want to argue something along the lines of ‘well, they are still poorer and less productive than New Zealand, so they should be achieving faster productivity growth than we are’, well we are a great deal less productive than the median advanced OECD country, and yet we’ve not managed to achieve faster productivity growth than them.

In fact, here is a chart showing OECD estimates of the 2015 level of real GDP per hour worked, converted at PPP exchange rates, for the eight eastern and central European countries, for New Zealand, and for four of the big higher-productivity OECD countries.

These days, our productivity levels look a lot more like those of the eastern and central European countries than of the OECD leaders (and Norway and Luxembourg and – questionably – Ireland are well above even those countries’ numbers).

At about this point, people often start saying “well, of course…those eastern European countries are close to the industrial centres of western Europe, and have been able to be attract foreign investment in manufacturing and become extensively integrated into the value chains associated with modern manufacturing”.

To which my response is along the lines of “well, yes, that is my point about New Zealand”. We are poorly located – for anything other than not being overrun by German or Soviet armies – and not many firms seem to have been able to develop substantial (unsubsidised) businesses selling internationally competitive products and services from here, based on anything other than our (fixed) natural resources.

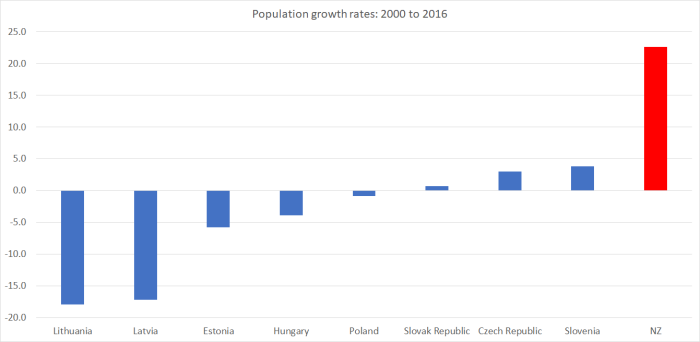

Which is why it has come to seem so odd that we, as a matter of public policy, are aggressively trying to grow our population – issuing 45000 residence approvals a year, three times the per capita rate of the US. In doing so, we simply make it harder for ourselves to prosper here.

In fact, here are the population growth rates of the eastern European countries and of New Zealand since 2000.

I don’t think I’d be too keen on living next door to revanchist Russia. But the five non-Baltic states here are firmly ensconced in central Europe, and over the last 16 years they’ve had an average of zero population growth, while our population has grown by almost 23 per cent.

Countries like that don’t have to devote huge shares of available resources (capital and labour) simply to keeping with the infrastructure needs of a rapidly rising population. That, in turn, keeps pressure off domestic costs, and keeps the real exchange rate lower than otherwise. Combined with more favourable locations, lower company tax rates (in most cases) and (the perhaps mixed blessing of) EU membership, they’ve been able to lift productivity and living standards for their people in a way that has had no parallel in recent decades in New Zealand. On typical institutional metrics like ease of doing business and corruption perceptions we score well ahead of any of those countries. We don’t need marches in the street to protect the independence of the judiciary (as in Poland). And our people do well on international skills comparisons. But it isn’t enough if one draws too many people into an unpropitious location.

Until we face up to the evident limitations of our location, and the absurdity of actively importing so many people from abroad into such a difficult location, it is difficult to believe that our underperformance, that has now stretched out over almost 70 years, will even begin to be reversed. For most of modern New Zealand history, France and Germany and the Netherlands had lower labour productivity than New Zealand did. Now they are far ahead. Slovakia is already passing us, and it seems reasonable to think that if we and they keep doing the same things we’ve been doing for the last 20 years, Slovenia and the Czech Republic will also go past us in the next decade. That’s good for them. I don’t begrudge their success – the fruits of freedom and decent policy, in the context of a good location – but what about us?

Here we have one main party that wants to pretend that productivity growth is just fine – simply ignoring the data. And another which recognises and is now highlighting the problem – I was seriously encouraged to see Jacinda Ardern making the “flat-lining at best” point about productivity in last night’s debate – but doesn’t seem to have seriously engaged with what might produce significantly better and different outcomes in the future. The scary thing is that if their roles were reversed, Labour might well be pretending there wasn’t a problem, while National still wouldn’t be offering much of a serious solution. And so, from the apparent refusal of either main party to really confront the presenting symptoms and attempt a serious diagnosis of what has been going on, we seem doomed to slip slowly ever further down the league tables. There are always many useful reforms to be considered. But, foremost, we need to markedly cut back that 45000 residence approvals target, and then back our own able people to make the most of the natural resources we have, in the face of the real and – on curent technology ineradicable – severe disadvantages of our location.

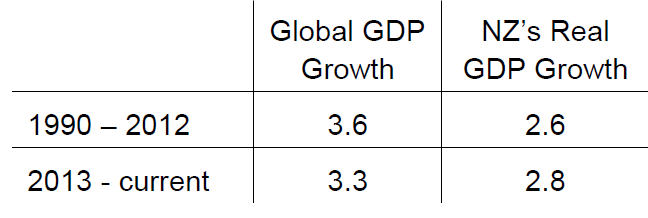

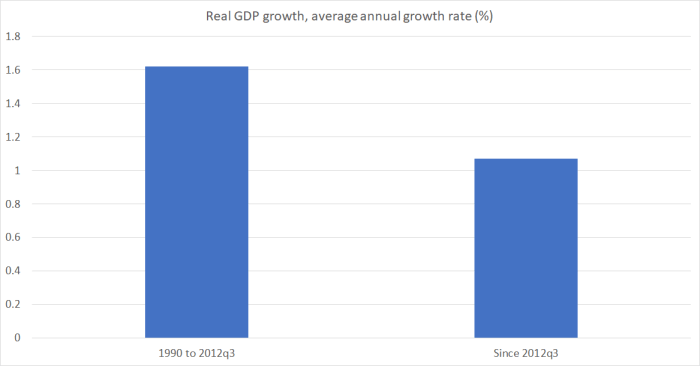

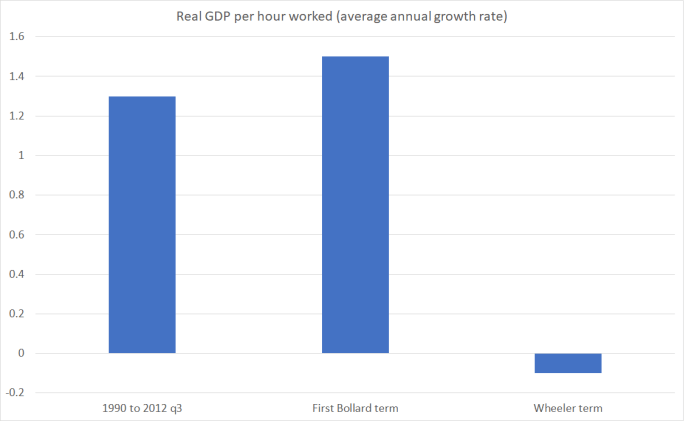

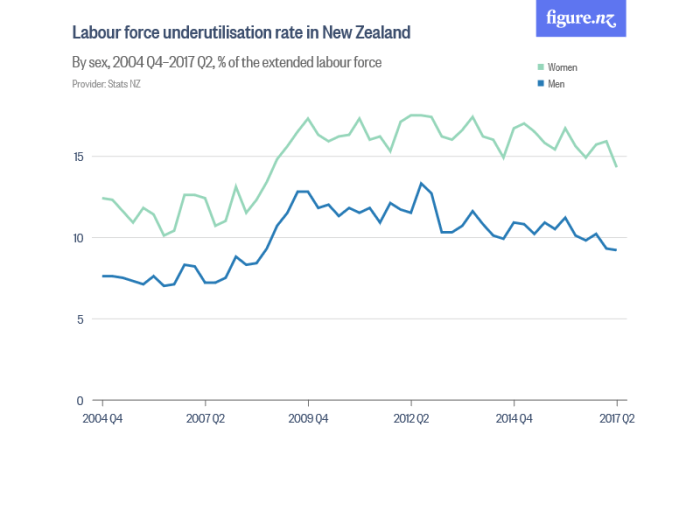

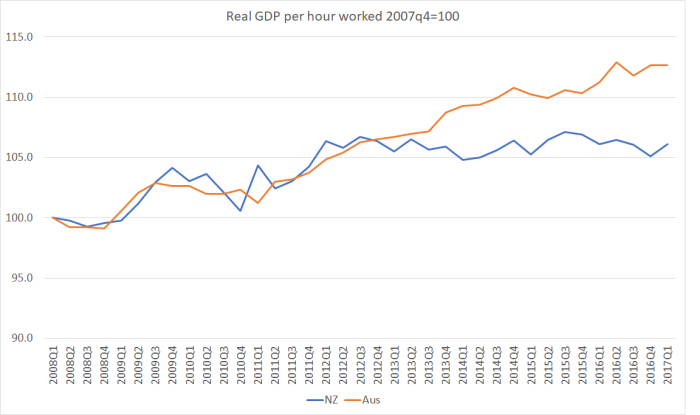

Not only have we had no labour productivity growth for five years, but our near-neighbour Australia – which the government was once willing to talk about catching up to – has gone on generating continuing labour productivity gains. Yes, there has been a productivity growth slowdown in much of the advanced world, dating back to around 2005. But our additional and more recent slowdown – well, dead stop really – looks like something different, and probably directly attributable to New Zealand specific factors. Things New Zealand governments have responsibility for responding to.

Not only have we had no labour productivity growth for five years, but our near-neighbour Australia – which the government was once willing to talk about catching up to – has gone on generating continuing labour productivity gains. Yes, there has been a productivity growth slowdown in much of the advanced world, dating back to around 2005. But our additional and more recent slowdown – well, dead stop really – looks like something different, and probably directly attributable to New Zealand specific factors. Things New Zealand governments have responsibility for responding to.

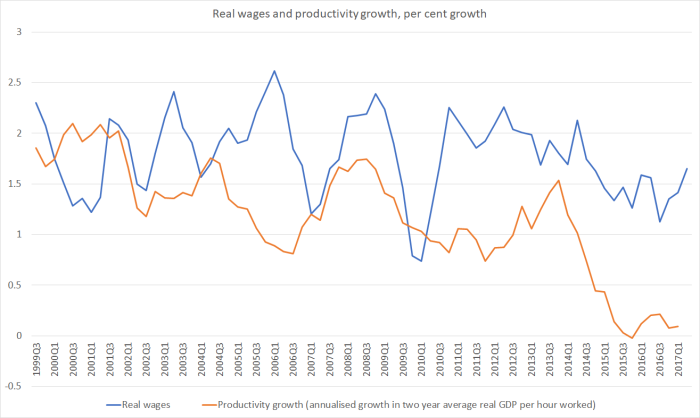

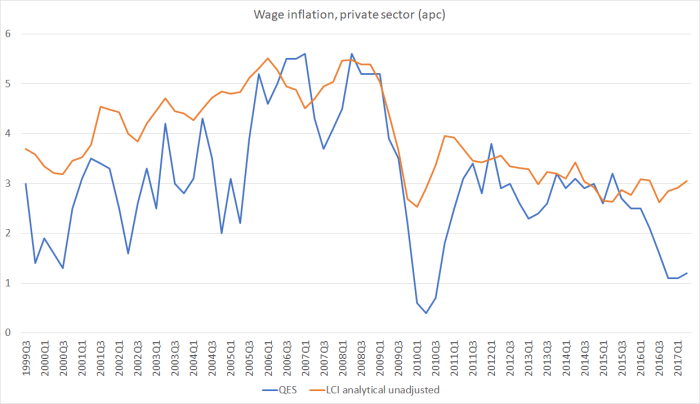

No economic analyst thinks wage inflation is anything like as volatile as the blue line – in fact, wage stickiness, and persistence in wage-setting patterns is one of the features of modern market economies.

No economic analyst thinks wage inflation is anything like as volatile as the blue line – in fact, wage stickiness, and persistence in wage-setting patterns is one of the features of modern market economies.