Graeme Wheeler yesterday gave a speech on current monetary policy issues and challenges. It was accompanied by an unusually long press release, and is probably best seen as a commentary, and elaboration, on the brief OCR statement released last week. I commented on that statement here.

I thought it was a very disappointing speech.

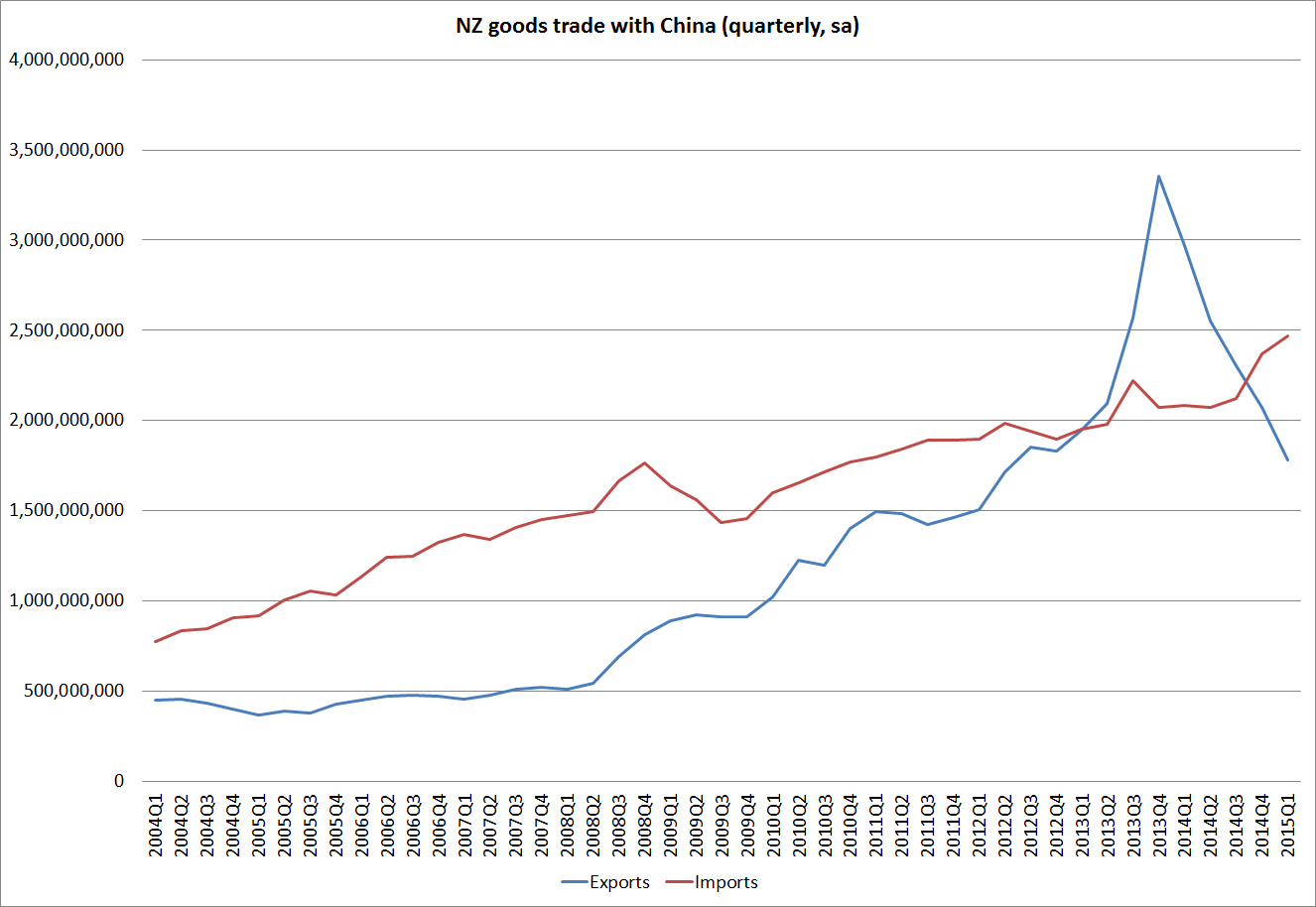

There is still no sign that the Governor recognises that he made a mistake in raising the OCR 100 basis points last year, in talking of further rate hikes as late as last December, and only beginning to cut rates in June. The fact that a mistake was made really should be blindingly obvious, even to him, by now. It should have been acknowledged and serious steps made to reverse it, and then we could move on. Instead, reluctance to acknowledge the mistake seems to have locked him into a mind-set in which he is now willing to cut the OCR as new weak data emerge, probably 25 points at a time, but is unwilling to unwind the excessively tight conditions he put in place last year. He repeatedly talks of GDP growth rates around 2.5 per cent as if these are good outcomes, but New Zealand’s population is estimated to have grown by 1.8 per cent in the last year. After an anaemic recovery, New Zealand is already experiencing weak per capita growth, before the full impact of the sharp fall in international dairy prices (let alone any threat from a weakening Asia) has been felt. And it is idle to talk repeatedly of the “need” for a lower exchange rate when he is personally deciding to hold the OCR at levels higher than the inflation target would appear to require.

Far too much weight in the speech is given to headline CPI inflation. As the Policy Targets Agreement has put it for years:

For a variety of reasons, the actual annual rate of CPI inflation will vary around the medium-term trend of inflation, which is the focus of the policy target.

The Governor has stated very explicitly in this speech that the Bank’s preferred measure of core inflation is the sectoral factor model measure. That measure it has its weaknesses, but it has the longest time series of any of the measures the Bank publishes, and it tends to be the measure I use most often too. As it happens, estimated sectoral core inflation over recent years has been being progressively revised downwards. And at 1.3 per cent now (and having been below 2 per cent for five years now) it is not just a “bit” (the Governor’s word) below the midpoint. For a very persistent slow-moving series, this is a huge deviation. “The medium-term trend of inflation” is nowhere near the 2 per cent target midpoint the Bank is required to focus on.

The Governor downplays this in two ways.

First, he explains away current low headline inflation mainly by reference to the fall in international oil prices and the rise in the exchange rate last year. Which is fine, and no serious observer is focused on headline inflation. But the Governor doesn’t mention tobacco tax increases, which have “artificially” and substantially boosted headline inflation in recent years. The Governor quotes the PTA to the effect that headline CPI inflation might deviate from the medium-term trend because of “shifts in the aggregate price level as a result of exceptional movements in the prices of commodities traded in world markets” [ie oil prices], but doesn’t mention that the next reason listed in the PTA is “changes in indirect taxes”. As I noted last week:

• Even with the rebound in petrol prices, CPI inflation ex tobacco was -0.1 over the last year – this at the peak of a building boom.

• CPI ex petrol inflation has never been lower (than the current 0.7 per cent) in the 15 years for which SNZ report the data.

We develop core inflation measures to adjust for these sorts of effects. Five and a half years with core inflation (on their own preferred measure) below the target midpoint, by slowly increasing margins, is a sign of a Bank that has got monetary policy repeatedly wrong. And that matters more under Graeme Wheeler, because he explicitly signed up to the focus on the target midpoint. Alan Bollard, by contrast, could (and did) point out that the midpoint had no special status in his PTAs.

And then the Governor tells us that he expects inflation to be back to target midpoint by the middle of next year. But here he is not talking about the “medium-term trend of inflation”, but about headline inflation. All else equal, if oil prices and the exchange rate stay around current levels, headline inflation is likely to pick up somewhat over the next 12 months. But the speech says nothing at all about the expected path of core inflation, or medium-term inflation measures more generally. A lower exchange rate provides a boost to the domestic price level, all else equal, but that just means the headline inflation rate rises for a year or so. What happens after that? As the Governor acknowledges, the Bank has overestimated medium-term or core inflation in recent years, but he offers us nothing, at all, to give us reason to believe that that situation has changed. There is no sign of any correction to what has led them astray for the last few years.

For the last 15 years or so, the Bank has generally sought to “look through” the direct price effects of exchange rate changes, precisely because they usually tell us little about the underlying state of inflation pressures. Doing anything else – putting much weight on those direct effects in setting policy – risks the Bank holding the OCR higher than the medium-term trend in inflation would warrant. Not just the PTA, but plenty of good economic theory also, encourages the Bank to focus on the stickier prices, captured in (for example, and imperfectly) non-tradables or core measures.

In fact, some of the Bank’s own quite recent research suggests that we might not see even much of an increase in headline inflation. Here is one of their researchers, Miles Parker, in a paper published last year:

The net impact of a fall in the international prices of the commodities New Zealand exports on the consumers price index (CPI) has been to lower New Zealand consumer prices, even though the exchange rate has tended to fall when export commodity prices fall. Falls in export commodity prices leave New Zealanders as a whole poorer and so domestic spending, and pressure on domestic labour and capital, tends to ease. For exchange rate depreciations caused by other factors there appears to have been little net effect on aggregate consumer prices, since a rise in tradable CPI inflation has been broadly offset by a fall in non-tradable CPI. For each of these classes of exchange rate changes, the inflation outcomes implicitly include the average response of monetary policy to such exchange rate movements over the period.

In other words, falls in the exchange rate happen for a reason, and have often been accompanied by such a significant weakening in economic conditions that they have often been associated with further falls in non-tradables and core inflation measures. That has to be a real risk now, as falling real (terms of trade) incomes and slowing growth in construction activity take hold.

What else is there to say? A few scattered observations:

• The Governor rightly observes that “in most advanced economies, policy interest rates are at historic lows”, but one could go further. In all OECD countries, except New Zealand, policy interest rates are lower (or no higher) than they were at the start of last year. New Zealand has seen no sign of the sort of medium-term inflation pressures that would have warranted – or warrant now – such a stance. The Bank thought such pressures would emerge, but they were wrong. Mistakes happen, but they need to be acknowledged and corrected for.

• I find it extraordinary that the Governor continues to articulate a view that high immigration has eased inflation pressures (outside the Auckland house market presumably). Until the last 12 months or so, the Reserve Bank has for decades consistently operated on the assumption, well-supported by data, that (whatever the possible long-term benefits) the short-term demand effects of immigration dominate the supply effects. Indeed, that result is apparent in the Bank’s own quite recent published research. Here is a picture from a 2013 Analytical Note

• It is puzzling that there is no mention of unemployment in the speech at all. It isn’t a fool-proof indicator by any means, but is probably better estimated and more easily interpreted that output gap estimates which the Bank continues to rely on (despite the inability of the Bank’s existing models to explain inflation). At 5.8 per cent, New Zealand’s unemployment rate is still disconcertingly high. It is all very well to laud rises in the participation rate, but there is no evidence that New Zealand’s NAIRU is anywhere near as high as 5.8 per cent. Many real people – with lives currently blighted by unemployment – would have been back in jobs if the Reserve Bank had not set the OCR so high over the last 18 months. What, I wonder, does the Governor have to say to these people when he meets them?

• This passage in the speech seemed particularly ill-judged:

Central bankers have found the post Global Financial Crisis (GFC) years to be a very challenging time for conducting monetary policy. High expectations have been placed upon central banks at a time when the economic, financial and political interlinkages in the global economy seem more complex, and where monetary policy has become the fall-back policy to promote a strong global recovery.

Few people will have much sympathy with highly-paid powerful officials bemoaning how difficult their job has been in recent years, as the Governor seems to. He has options.

Many of the problems central banks in other countries have faced relate to running into the near-zero lower bound on nominal interest rates. New Zealand (and Australia) have not yet got anywhere near that floor. There is no evidence of “high expectations” having been placed on the Reserve Bank of New Zealand – indeed, the dismal inflation track record, with no obvious adverse consequences for the Bank, might suggest a central banking equivalent of the “soft bigotry of low expectations”. The Governor complains that “monetary policy has become the fall-back policy to promote a strong global recovery”. Most New Zealanders would have settled for a strong domestic recovery, but we just have not had one. It has been the weakest domestic recovery for many decades, despite the record terms of trade, and the boost to demand from a Christchurch-led building boom.

In a sense, the whole point of discretionary monetary policy is to allow monetary policy to promote strong bounce-backs when demand falls away and recessions happen. With hindsight it is clear that lower policy interest rates over the last five years would have given us both a stronger recovery, and a medium-term trend in inflation nearer the inflation target. There were no policy obstacles to doing so. I’m not suggesting there are no puzzles in the global events of the last few years, but if you have trouble reading the future, just look out the window and respond to the best estimates of the medium-term trend in inflation. Core inflation has been below target midpoint since December2009, and not once – not for a single quarter – has the OCR been cut below the level that prevailed back then.

• The Governor repeats a claim that “our economy has generated better growth…than many other advanced economies”. As I have documented on several occasions, and in several ways, while our total GDP growth has been relatively high, that is only because our population growth has been much faster than most. Growth in GDP per capita, or in any of the productivity measures, has been no better than mediocre, even relative to other countries’ weak performances. Quite why we have done so badly is still a bit of a puzzle, but endless repetition of an alternative wished-for story does not make it true.

• Somewhat puzzlingly the Governor claims that “some local commentators have predicted large declines in interest rates over coming months that could only be consistent with the economy moving into recession”. Actually, it isn’t only local commentators, but set that to one side. With core inflation measures so low, and no evidence adduced that core inflation measures are about to rise materially, it would be quite easy to make the case for a 2 per cent OCR right now. There was never any need for the OCR to have been raised at the start of last year (from 2.5 per cent) and core inflation pressures and measures are weaker now than they were then. At present, with the threat from a weakening Chinese economy increasing, the risk is that having held the OCR too high for too long materially increases the chances of a couple of quarters, or more, of negative GDP growth. And the Governor needs to get some perspective on the scale of short-term interest rate falls that tend to happen in real recessions: 700 basis points over the 1991 recession, 550 basis points in the mild 1997/98 recession, and 575 basis point OCR cuts in 2008/09. Against that background, arguments as to whether the OCR gets to 2.5 per cent or 2 per cent, from a recent (ill-judged) peak of 3.5 per cent, are interesting but bear no relationship to what any serious recessionary threat might require.

There are many more points I could make. There are puzzling sentences like “having the scope to amend policy settings, however, is a key strength of the monetary policy regime”. I’m not sure when anyone last suggested a regime in which policy settings could not be amended, but perhaps I missed something. But I’ve probably taxed readers’ endurance enough already.

New Zealand deserves a lot better than this: better policymaking and better quality analysis and communication of the issues. And, of course, it is increasingly past time for reform of the governance of the Reserve Bank, to put considerably less power in the hands of one imperfect individual, the Governor (any Governor).

Meanwhile, what does the Governor say to any of those 146000 unemployed people he meets?