I’m getting tired of the subject, and readers probably are too, but I noticed that in today’s Herald Brian Fallow had reported Graeme Wheeler’s case that the Reserve Bank had not made a mistake in raising the OCR so much last year, and holding it up for so long.

I’m sure Graeme had no say in the headline “We didn’t get it wrong: Wheeler”, and perhaps Brian Fallow didn’t either. But actually the article is a compilation of individual items where the Bank did get it wrong over the last 18 months. Some of those mistakes were probably quite pardonable (in full or in part), but they were mistakes:

- The Bank did not forecast a material fall in dairy prices

- It did not forecast the fall in oil prices

- It did not forecast the extent of the net migration inflow (or, apparently, the proportion of those arriving who were (a) students, or (b) young workers.

- It did not forecast the extent of the increase in the labour force participation rate.

As I noted yesterday, dairy prices have been volatile for the last decade. Faced with dairy prices as high as they were at the start of last year, it was imprudent of the Bank to have acted on the assumption that they would stay anywhere near that high for long.

The Governor seems to have in mind some sort of version of the world where GDP growth had been around 3.5 per cent, and yet labour force growth had been much lower than it was. That would, almost certainly have been a more inflationary economy than the one we have seen. And in fact it was what the Bank was forecasting at the start of last year. But we now know that GDP growth would not have reached anything like 3.5 per cent without the growth in the population and the labour force we’ve seen. Demand just wasn’t strong enough otherwise. And, on the other hand, population growth surprises add a lot to demand.

I was also puzzled by the claims around migration. Fallow reports:

The bank says the composition of the immigrants – more single workers recruited for the Canterbury rebuild and more students – has meant that the boost to the supply-side capacity of the economy has been faster and stronger, and the effect on demand weaker, than headcount alone would historically have indicated.

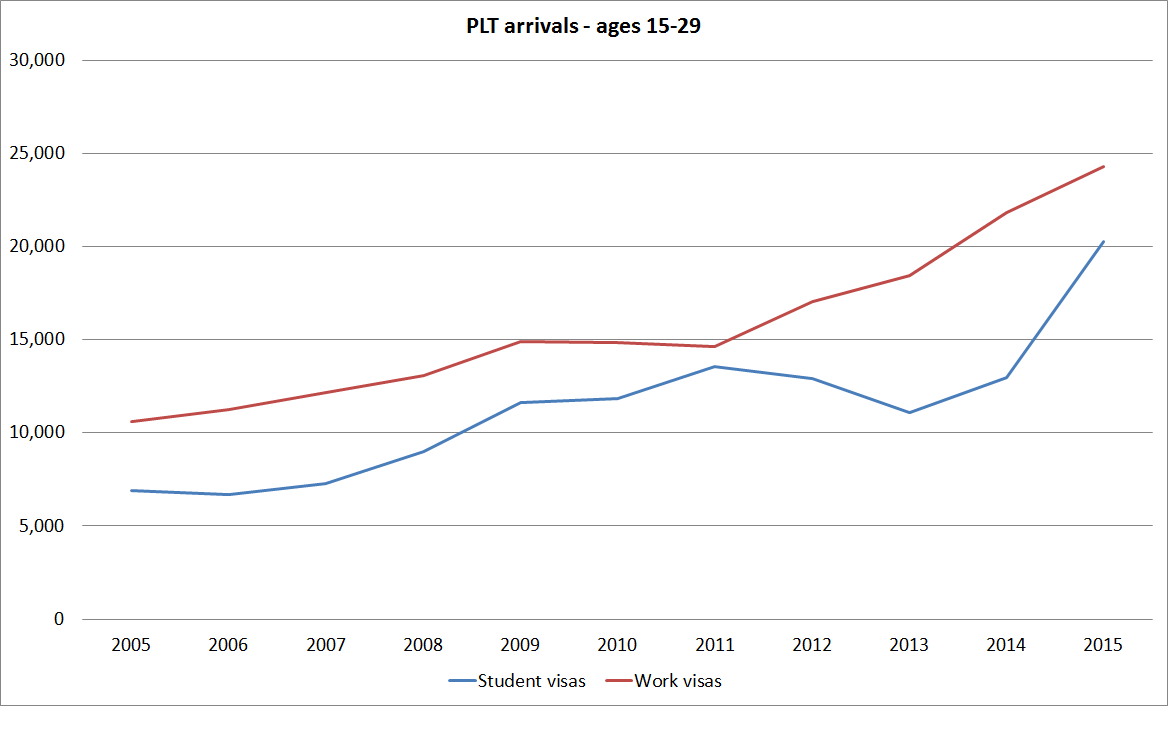

This sentence seems internally contradictory. More single workers [or presumably married ones without children] certainly have the direction of effect the Bank talks about, but more students goes in the opposite direction. Foreign students add to demand (for accommodation, for education, and for other consumption items) but generally add very little to labour supply. This chart shows permanent long-term arrivals for those in the age group 15-29. If anything, over the last year or two, the rate of increase in those of student visas has been even greater than the increase in the number of young foreign workers.

The article also reports

Combined with capital investment by business it means that it has taken a couple of years longer for the slack in the economy to be taken up and the output gap to turn positive than the bank expected when it started tightening last year.

But as I noted the other day:

- The Bank’s view of the level of excess capacity that existed 18 months ago, at the start of the tightening cycle, has been revised materially. Judging spare capacity isn’t easy, but they now think they were wrong about the earlier view that excess capacity had already been fully absorbed.

- The level of investment since then just has not been very strong. Growth in hours worked has been quite rapid over the last year, even by the standards of the previous boom, and yet investment did not reach previous boom levels. (And, of course, when the previous rates of investment were occurring there was still a lot of inflationary pressure). As our best estimate is also that productivity growth has been lousy, this story of an unexpected growth in supply capacity just does not wash.

Economic forecasting is hard, and mistakes will happen. With the possible exception of the over-optimism about dairy prices, I wouldn’t be very critical of the Bank on any of those forecasting errors. They are the sort of thing that happens.

But what I think translated the events of the last 18 months into something a little more serious (and again, it isn’t the worst monetary policy mistake ever, by a long shot) is that the Reserve Bank was under no pressure at all to have acted at all last year:

- Core inflation, on the estimates available to the Bank at the time, was around 1.6 per cent, and had been for several years

- The unemployment rate was still 6.1 per cent, not far below the sort of level it have averaged in the recession years

- Credit growth was modest

And inflation had stayed low, to that point, despite the very big and concentrated increase in residential building activity that had already occurred in Christchurch. For several years, the Bank had (quite reasonably) cited the rebuild as one of the forthcoming major pressures on resources and inflation. For that matter, there was no sign that commodity prices – which had been high for a year, while inflation stayed low – were about to rise further.

When inflation is high and resources are demonstrably stretched it is quite understandable when central banks are a little jumpy about new inflationary pressures. As I noted yesterday, Alan Bollard raised the OCR four times in succession in 2007 when dairy prices were soaring. With hindsight, those increases weren’t necessary – the 2008 recession took care of the inflation, and reversed the dairy price increases – but I wouldn’t call those 2007 increases a policy mistake.

But in 2014 the Reserve Bank did not need to act. There were no new inflationary pressures, and the Bank was under no pressure to raise rates, other than the pressure it imposed on itself. Having started raising the OCR, it was under no pressure to carry on increasing rates. It was under no pressure, as late as December last year, to be talking of further rate increases.

It was a policy mistake. They happen. They have occurred in the past, here and abroad. And policy mistakes will happen again.

Here’s roughly how, in Graeme Wheeler’s shoes, I would have answered the question “did you make a mistake?”

Yes, we did. Monetary policy aims to keep inflation over the medium-term at around 2 per cent. Doing so means we make extensive use of economic forecasts – trying to make sense of where we are now, and where things are likely to head over the next couple of years. Our forecasts were not so very different from those of other economists and agencies But we misjudged just how much pressure there was (and was going to be) on resources, and as a result we raised interest rates sooner, and further, than was really warranted.

One of the lessons people should take away from this episode is that monetary policy isn’t a precise or surgical tool. We have to make judgements about things that reasonable people can reach quite different views about. That means at times we will make mistakes. When we do, we’ll be very open about them, and correct them as quickly as we can. What I can’t promise you – and no one can – is that there will be no mistakes in the future.

I’m disappointed that we got it wrong this time – and as the chief executive and single (statutory) decision-maker I have to take responsibility for that error. Our mistakes matter for people’s lives and businesses. But you have my commitment that we are going to learn from this episode – not just about the economy, and also about our processes for making sense of, and responding to, the data.

I’d have applauded an answer like that. I suspect the wider community probably would have too.