Both the Dominion-Post and the Herald this morning devoted their editorials to monetary policy and yesterday’s announcement by Graeme Wheeler. The Herald, somewhat oddly, commends the Governor on “seeking to get ahead of the curve”. In principle, I suppose that is always what he is trying to do – it is, after all, forecast-based inflation targeting. But I’m not sure that too many people would regard one OCR cut, just beginning to reverse last year’s increases, as “getting ahead of the curve” when core inflation has been so persistently low, and the unemployment rate has remained troublingly high. A belatedly awakening might be a better description.

But I was more interested in the Dominion-Post’s thoughtful piece. Here is the heart of it:

This is more than just an abstract number. It is a signal that more was possible. It suggests that, even though growth has been robust for the past couple of years, it might have been higher, with few costs, had the bank kept rates lower. That, in turn, might have meant more jobs and lower unemployment – which, at 5.8 per cent currently, is still too high.

Was it possible to sense any of this earlier? Monetary policy is a difficult business, and reasonable people can disagree. Certainly the plunge in global oil prices, a key factor behind low inflation, was a surprise to most observers. The slump in dairy prices, too, which will likely weigh heavily on the economy, has been steeper and more prolonged than anticipated.

But other factors were perhaps not so shocking – the slow progress of the global economy, the large influx of migrants to New Zealand (in train before last year), the persistence of low wage growth and local unemployment.

Much hinges on the opaque question of the economy’s “capacity” – essentially how hot it is running. It is always difficult to tell at any given moment; the truth gets clearer in the rear-view mirror.

The bank moved swiftly last year when dairy prices soared, the housing market surged, and the economy began hitting its straps. In hindsight, it moved too fast; it turns out there was more capacity – more labour and resources – to go round than it thought.

At the least, bank governor Graeme Wheeler and his team will need to consider if they were too quick to jump then, and too slow to reverse course.

Still, they have done it now, and rightly so.

I happen to agree with the editorial, but that isn’t really my point. I’m hardly alone in lamenting the quality of a lot of public debate and media coverage of policy issues, but I was impressed that a newspaper editorial in this country could, in a calm way, highlight the uncertainties that monetary policy makers face, and the scope for reasonable people to disagree on the outlook for the economy. And that the paper could suggest, in a very moderate tone, that it might be time for some critical self-examination by the Governor and his team . It was the sort of balanced perspective that, say, those charged with holding the Reserve Bank to account, such as the Bank’s Board, might have read with profit, or which their advisers might have written. (Of course, it is an open question whether it is the sort of piece that sells more newspapers.)

I noticed media accounts of the Governor’s appearance at FEC yesterday report him again denying that he made a mistake last year, whether in raising the OCR so much or holding it up for so long. I’m not quite sure what he hopes to gain by this stance. The Governor used to tell staff that his aim was for the Reserve Bank to be the “best small central bank in the world”. One of the marks of a successful, learning, organisation is the ability to acknowledge mistakes, learn from them, and move on. I suspect that there is a more chastened attitude internally than is evident publically, but this is a powerful public organisation, and we should reasonably expect to see more evidence of an ability to acknowledge mistakes. A misjudgement about monetary policy is not the worst thing in the world – it is in the nature of the game. If anything, a refusal to acknowledge the misjudgement is more worrying, and detrimental to our ability to have confidence in the Governor, or in the single decision-maker governance framework. It might, for example, be easier for a committee to acknowledge a mistake than for an individual to do so.

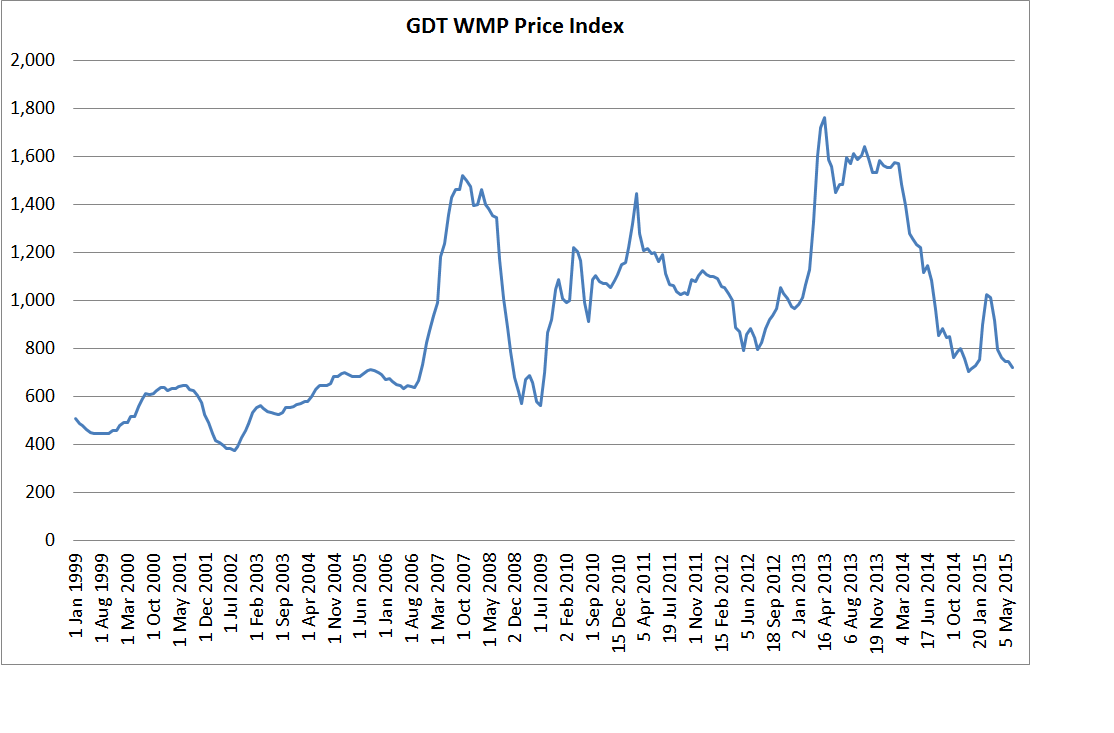

But was it a mistake? The Governor appears to put a great deal of weight on the high dairy prices at the start of last year. Even then, the Bank’s forecasts did not have export prices staying up indefinitely. But the Bank’s optimistic forecasts for dairy prices back then required something quite out of the ordinary. In the last decade, since EU policies began to change and dairy stockpiles were exhausted, global dairy prices have been much more volatile than previously (and production is much more responsive to changes in output prices and input costs). At the start of 2015 a reasonable person might not have forecast dairy prices falling quite as low as they have or for long, but they would not have assumed the persistence of anything like the WMP prices seen in 2014.

This is what the Governor had to say in the March 2014 Monetary Policy Statement as he initiated the tightening cycle

Overall, trading partner growth has seen demand for New Zealand’s goods exports remain robust. Increasing rates of urbanisation and protein consumption in China are supporting demand for many of New Zealand’s commodity exports

Consequently, global prices of New Zealand’s commodities are extremely high, particularly for dairy. Dairy prices increased substantially in the first half of 2013 and remain at those high levels.

Rising demand in New Zealand’s trading partners, and particularly China, will result in continued growth in demand for New Zealand’s exports over the projection. Export prices are expected to remain high relative to history, though ease by about 3 percent over the next year due to an assumed moderation in global dairy prices.

The Bank – and the Governor – seemed beguiled by China. A rather more reasonable approach would have been to have assumed that large fall in dairy prices were likely, even if the Bank could not be quite sure when they would occur. Forecasters have to have a specific track. Policymakers need to exercise judgement.

And context matters greatly. When the first OCR increase was put in place, the unemployment rate was still above 6 per cent, less than one percentage point off the peak during the 2008/09 recession. The recovery had not (and still has not) ever achieved the sorts of real GDP growth rates seen in earlier recoveries. And, of course, headline and core inflation were both (still) below the midpoint of the target range. Private sector credit growth was running at around 5 per cent per annum, less than the (then) rate of growth in nominal GDP.

There just was no urgency[1]. There was slack in the economy, continuing low inflation, modest credit growth. Reasonable people might have been able to differ about the first OCR increase – for what its worth, I advised against it, but I was a minority voice – but the Governor went on tightening, moving at each of four successive reviews, even as dairy prices started falling sharply and core inflation just kept on staying low. As late as December last year, the Governor was talking about the likely need for further OCR increases.

But he was wrong. His approach last year was a mistake. It appeared to be driven, at least in part, by a belief that there was something anomalous about the OCR as low as it had been, and that getting interest rates nearer the Bank’s estimate of neutral would be “a good thing”.

In one sense it shouldn’t be a great surprise that such mistakes are made. The single decision-maker system system is not well-designed to minimise the risk of mistakes (some of Alan Bollard’s early moves were also mistaken, as he later acknowledged). And the Governor does not have a strong background in monetary policy or macroeconomics, and had not worked in New Zealand for 15 years when he took up the job. Last year’s OCR adjustments were the first OCR changes he had made.

It would be better if the Governor simply acknowledged that he had made a mistake. They happen. It would be better for him, for the organisation (externally and internally – learning organisations have to create room for staff to make mistakes), and for the country which entrusts so much power to the Governor. If he is so unwilling to acknowledge a pretty clear-cut mistake, how willing is he to engage in critical self—scrutiny (or encourage it among staff) in areas where there might be rather more shades of grey?

[1] And, thus, the situation was quite different at the start of 2007 when, with unemployment already very low and core inflation very high, a lift in dairy prices, from relatively low levels, prompted Alan Bollard to raise the OCR four times in successive reviews.

Now that’s a hard-hitting essay. Good stuff.

LikeLike

Michael

Could you publish a historical figure of forecast errors, say from 1992 to date. If you do not the data, could ask the RB to send you the data. We used to debate these numbers. This is how reasonable learn from past mistakes.

Policy errors are not a simple matter. They are persistent and cost a lot to undo.

LikeLike

Weshah

I don’t have that data in one place (and I don’t think the Bank would be keen to give it to me – any one else might get it in fewer than the statutory 20 working days, altho they might just be told to compile it themselves from the MPS tables on the web). But one way of looking at the issue is to take a smooth core series, like the sectoral factor model measure, and compare it with the target midpoint (I’ve shown that chart previously). On that basis, the Bank consistently underpredicted inflation from the start of the price stability era (say 1992) through until 2008, and then has overpredicted since then. You can also see the latter errors in the deviations between forecast policy rates and actual rates over the period since 2009.

In the post 2009 period most central banks have made much the same mistake – constantly inclined to believe that things were just about to come right. The main difference with the RB is that it actually tightened on that view in two separate episodes. One tentative hypothesis is that the Bank recognised the bias in its pre-recession forecasts (which was not there for other inflation targeting countries) and (rightly) wanted to avoid that going forward. I know that was my own attitude. It may have made them too ready to tighten.

Michael

LikeLike

Thanks Michael

Essentially you are saying the forecast errors have patterns, which make them predictable by the public, hence MP is ineffective. How could the RB affect real output and unemployment in the short run if policy is ineffective? Think about a small firm (95 per cent of our firms are small) which correctly expects the RB to increase interest rate next period.

LikeLike

No, I don’t think that is what I am saying. No doubt there is an element of predictability to the deviation of inflation from the midpoint, but that realisation comes slowly, and at a real cost.

LikeLike