In the new government, sworn in this morning, David Parker will take up the renamed role of Minister for Trade and Export Growth.

Early in their term of office, the outgoing government adopted a numerical target for lifting exports (as a share of GDP). It was, no doubt, well-intentioned, but has provided the basis for quite a few posts here pointing out that no progress was actually being made towards that target, if anything trade shares of GDP were falling, and the pre-election advice from The Treasury was that, all else equal, the trade shares would continue to shrink. The focus on exports, in turn, seemed to prompt a willingness to use actual or implicit subsidies – be it in the film industry, export education, irrigation, convention centres, or firms like Rocket Lab – or unpriced externalities (eg around water) rather than focusing on the fundamentals in a way that might have seen firms themselves increasing taking up new foreign trade oppportunities, responding to improvements in opportunities, markets and incomes.

I stress “foreign trade” rather than just “exports”. We don’t want policy to be guided by some sort of mercantilist vision in which the purpose of economic life is to sell us much as we can to others, only to store up treasure at home. Firms export because they can, and because doing so enables owners and employees to earn incomes, which enable them to consume (including from among the abundance the wider world has to offer). Successful firms invest more heavily too, and many of the investment goods will typically be sourced from abroad. Trade is good, and generally mutually beneficial. Ideally, we would see quite a bit more of it: New Zealand firms successfully competing in wider world markets, enabling them and us to purchase more of stuff firms in other countries specialise in producing. And if New Zealand is ever to catch up again with the rest of the OECD – whether in productivity or incomes – the process of getting there is likely to involve a materially larger share of local production being exported but – especially in the transition (which could last decades) – a lot more investment. Current account deficits aren’t even problematic when they rest on firm foundations of rising productivity and market-led business investment. It was the story of 19th century New Zealand (or Australia or the United States). It was the story of emerging Singapore and South Korea.

So I really hope that the new Minister of Trade and Export Growth (who is also the Minister for Economic Development) sees his role as being at least as much about putting in place the pre-conditions for sustained stronger import growth, as about export growth. In successful economies, the two go hand in hand.

Here is how we’ve been doing over the 45 years for which we have official data.

The last few years’ data are still open for revision, but there is no credible prospect that trade shares of GDP will have been rising.

In interpreting the graph it is worth noting a few things. The first is that the peaks in the 1985, 2001, and 2009 years simply relate to unexpectedly weak exchange rates. Most of our imports and exports are priced in foreign currency terms, so when the exchange rate falls sharply there is an immediate translation effects – both imports and exports rise in NZD terms, even if the volumes haven’t changed at all. In each of those three cases – the 1984 devaluation, the slump in the NZD (and AUD) at the end of the dot-com boom, and the sharp fall in the 2008/09 recession – the exchange rate falls were pretty shortlived.

The second is to note that external trade as a share of GDP was trending up for some time. The economic policies New Zealand adopted after 1938 had tended to reduce our external trade. There was a focus on increasing local manufacturing to supply domestic markets in consumer goods (directly reducing imports), and the increased costs of that domestic protectionism undermined the competitiveness of our (actual and potential) export producers (thus, shrinking exports as a share of GDP).

But in the 1970s and early 1980s there were signs of progress, lifting both export and import shares of GDP, even though the terms of trade for New Zealand were pretty dreadful during that period. There will have been a mix of factors at work: the real exchange rate was trending lower, import protection was being reduced and, less encouragingly, there was a substantial use of export subsidies, both for non-traditional exports and (latterly) support for farmers too. One argument made at the time for that export support was to counter the adverse competitiveness effects of import protection. Better, of course, to remove both sets of interventions. And that is largely what happened over the following decade. Trade shares of GDP didn’t fall back.

It is perhaps tempting to look at the chart and conclude that taking the last few decades together there is quite a lot of variability in the series, and overall nothing very much has changed since at least the early 1980s. That’s largely true, but it is also largely the problem. Successful economies have typically experienced quite material increases in their foreign trade shares (imports and exports) in recent decades. New Zealand hasn’t. New Zealand – or foreign – firms simply haven’t found the profitable opportunities here to take advantage of. Even services exports are now only around the same share of GDP that they first reached in 1995. Amazingly (I hadn’t previously looked at this number), services imports as a share of GDP have been lower in the last year than at any time in the past thirty years.

Not exactly a picture of a successfully internationalising economy.

I don’t find these outcomes – worrying as they should be, as symptoms of our economic failure – that surprising. It is very difficult for firms to compete successfully internationally from such a remote location, based on anything other than location-specific natural resources. Not impossible, but very difficult. And so it shouldn’t surprise us that there aren’t many of them. For whatever reason, in the global economy personal connections on the one hand and integrated value/supply chains on the other have become increasingly important. The last bus stop before Antarctica – a long way even from the next to last bus stop – just isn’t a propitious place, no matter how skilled New Zealand workers might be, and how innovative and entrepreneurial New Zealand firms might be.

It is also difficult to successfully compete internationally from here when (a) real interest rates and, in turn, the real cost of capital, for New Zealand investors have averaged so much higher than those in the rest of the advanced world. Those real interest rate gaps have shown no sign at all of closing (and they have little or nothing to do with monetary policy). People push back sometimes arguing that interest rates can’t make that much difference. They do, through two channels. First, the standard approach to identifying an appropriate discount rate for project evaluation starts from a risk-free interest rates. Ours are, and consistently have been, well above those in other advanced countries (something like a 150 basis point margin is a reasonable approximation of the average difference). And, second, high real interest rates here have been accompanied, causally, by a persistently high real exchange rate, out of line with our deteriorating relative productivity. In combination, that mix makes investment here harder to justify, and particularly makes investment in the tradables sector harder to justify. Combine that with the disadvantages of distance and it is no real surprise the foreign trade shares of GDP haven’t increased. Successful economies have an abundance of new profitable opportunities in which their firms, or foreign firms investing there, take on the world. It has happened to only a very limited extent here.

But what concerns me is that the new government appears, at this stage, to have no more of a strategy than the outgoing government did for turning around the dismal productivity performance, or the static (or shrinking) foreign trade shares. There have been encouraging hints of a recognition of the issue: in her speech to the CTU yesterday, the incoming Prime Minister referred both to a need to “boost our productivity” and to the need to gear the economy more towards “value-added exports”. But it isn’t clear that they have any real idea of how to get from here to there. There was nothing any more encouraging in James Shaw’s speech to the same audience. Or looking through the areas prioritised in the agreements Labour has signed with New Zealand First and the Greens. If anything, the risk looks to be that the tradables sector will shrink further.

- The new government plans to adopt measures that will reduce the size of the export education sector. To the extent that involves a removal of implicit subsidies I think (as I noted yesterday) that is a step in the right direction.

- The new government plans to phase out government subsidies for irrigation schemes. From what I’ve seen, that is welcome too.

- The new government is clearly heading in the direction of reducing exploration for oil and gas in New Zealand and its territorial waters.

- The new government is clearly intending to take a more aggressive stance around emissions reductions, including moving towards the inclusion of agriculture in the ETS.

- The new government seems likely to move more aggressively on increasing water quality standards faster,

- And the new government is planning to increase minimum wages – already high, by international standards, relative to median wages – quite considerably over the next few years.

- The new government is planning (or hoping for) a major acceleration in housebuilding activity.

You might agree or disagree with some or all of those measures individually. But every single one will put the tradables sector under more pressure, to some extent or other.

Take minimum wages for instance. I recommend you read Eric Crampton’s piece (which I largely agree with). Here is the Prime Minister’s take.

I know most businesses want a fair set of employment policies. They know that we need decent wages if they are going to have customers for their products. They know that we need to boost our productivity, and low wages are a barrier to that because they discourage investment in training and capital. They know that we need a government that invests in skills and education.

I simply don’t buy into baseless claims that paying people well means there will be fewer jobs. In fact, the overwhelming weight of evidence is that strong wages for all working people help to boost growth and create jobs.

Wishful thinking at best. We all, I imagine, want a country in which strong economic performance and strong wage growth goes hand in hand, but there is little or no credible evidence that, at an economywide level, one can get that sort of lift in performance by, say, mandating higher minimum wages. It is putting the cart before the horse. And if it worked anywhere, surely New Zealand should be the prime example, given that we already have high minimum wages relative to median wages (a policy maintained and extended by the previous National government).

And here is Shaw

And our whole intent will be to flip climate policy from being seen as a threat and a cost, to being seen as an opportunity and an investment in the future.

And, as I say, that means we’ll be creating tens-of-thousands of new jobs, paying decent wages, for workers and families all over New Zealand.

Not just high-tech city jobs, but out in the regions as well.

Here’s one example: trees.

We are going to plant hundreds of millions of trees to soak up New Zealand’s greenhouse gas emissions.

These trees, we’re going to plant them in the cities. We’re going to plant them in the towns. We’re going to plant them in in the National Parks. We’re going to plant them in the regions.

That’s going to be tens of thousands of jobs. That means lower unemployment. Lower poverty. Lower crime. Cleaner rivers. More native species.

It would be worth doing even if we weren’t saving the world.

One pictures the seas parting and New Zealanders walking together across the Red Sea to the promised land.

Whatever the merits of mass tree-planting – which until now firms have not regarded as economic – it doesn’t exactly seem like a high productivity industry. And in the short-term (trees take decades to come to maturity) resources that are used planting trees can’t be used for anything else.

Lower unemployment is a worthwhile goal, and I really liked the new PM’s line

we have unemployment stuck stubbornly at 5% when it should be below 4%

but (a) deviations of unemployment from long-term sustainable levels are mostly a matter of monetary policy (so find the right Governor/commitee, and specify the mandate well) and (b) however many trees you plant, higher minimum wages will almost certainly come at some cost – perhaps not that large – in higher long-term sustainable unemployment rates. And for all the complacency there has been in New Zealand about our unemployment rate, when I checked there were already 12 OECD countries with unemployment rates lower than New Zealand. We simply should be doing better.

Of course, the usual economist’s response when (eg) proposing stripping away subsidies is “the market will provide”. For example, a lower real exchange rate will allow some firms to expand, and other firms not yet visible to economists to emerge. But how likely is it that that provides the answer this time?

Of course, the exchange rate has fallen perhaps 3 per cent in the last few weeks since the election (against the AUD, the best guide to idiosnycratic New Zealand effects). It isn’t a large move, and may not be sustained. And even at these levels isn’t outside the range it has fluctuated within over recent years. Between a somewhat more expansionary fiscal policy (than the previous government was running), the aspiration to a big increase in housebuilding, and a continuation of the high target rate of immigration, it is difficult to see why we should expect any near-term material narrowing in the margin between New Zealand interest rates and those in the rest of the world.

Thirty years ago, Grant Spencer – then Reserve Bank chief economist, now “acting Governor” – published a book chapter in which he described pre-1984 New Zealand economic management this way

“In particular, the maintenance of high levels of aggregate demand supported a buoyant non-tradables goods sector while exporters faced more depressed market prospects”

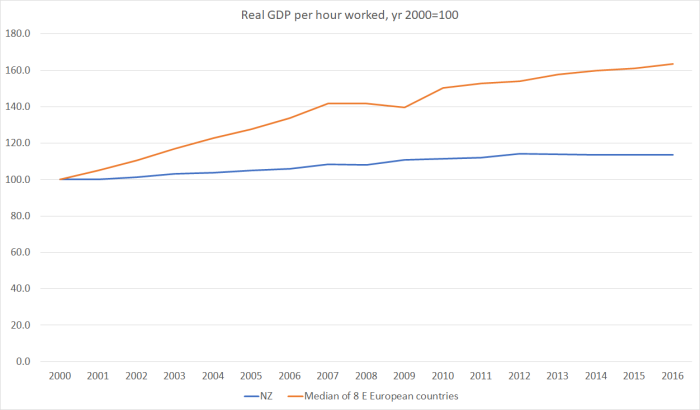

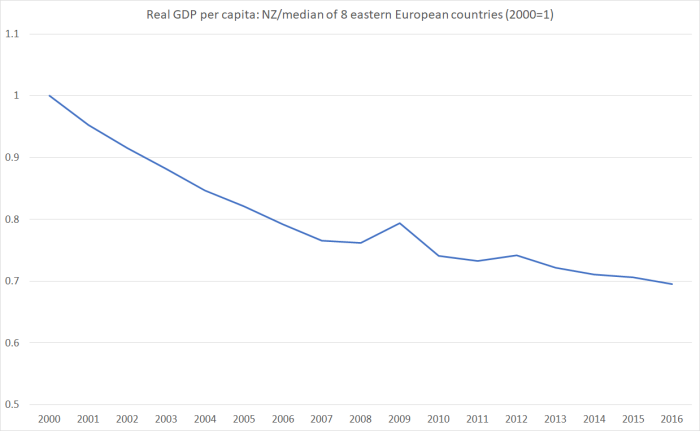

When I re-read that chapter last week, it was hauntingly reminiscent of the last few years. But it isn’t clear why the next few will be any better, unless there is sort of near-term cyclical downturn Winston Peters was warning about last week. As I’ve highlighted previously, in real per capita terms, the tradable sector of our economy is now no larger than it was 2000 – two whole governments ago. The risk, at present, is of further shrinkage.

So I do hope that the new Minister of Finance and Minister of Economic Development (and Trade and Export Growth) are turning their minds pretty quickly to how they might achieve the sort of reorientation in the economy that is generally recognised as needed, and which they – and the Prime Minister – have themselves highlighted as a matter of concern. (And, hint, regional development funds aren’t likely to be the answer either. And over the last 15 years, “the regions” have been doing better than “the cities”)

(On matters of the new government, I was interested to see Andrew Little, new Minister of Justice, observe – on Twitter and Facebook – yesterday that “As Minister of Justice-designate I want to state from that outset that “pretty legal” is no longer the standard this country operates to!”. Admirable sentiments, and I have no idea what specifics he had in mind [oh – Steven Joyce no doubt], but might I suggest that he and the Minister of Finance review how we came to have a pretty clearly unlawful appointment of a Reserve Bank “acting Governor” by the outgoing Minister of Finance. )