Yesterday’s announcement from the Minister of Finance that he was reappointing Adrian Orr as Governor of the Reserve Bank was not unexpected but was most unfortunate. I was inclined to think another commentator (can’t remember who, so as to link to) who reckoned that it may have been Robertson’s worst decision in his five years in office was pretty much on the mark.

When Orr was first appointed, emerging out of a selection process kicked off by the Reserve Bank’s Board while National had still been in office, it seemed to me it was the sort of appointment that could have gone either way. I captured some of that in the post I wrote the day after that first appointment was announced, and rereading that post last night it seemed to at least hint at many of the issues that might arise and come to render the appointment problematic at best. Some things – a good example is $9.5 billion of losses to the taxpayer – weren’t so easy to foresee.

The timing of the reappointment announcement itself was something of a kick in the face for (a) critics, and (b) any sense that the better features of the new Reserve Bank legislation were ever intended as anything more than cosmetic. The Reserve Bank is tomorrow publishing its own review (with comments from a couple of carefully selected overseas people) of monetary policy over the past five years. Adding the statutory requirement for such a review made a certain amount of sense, but if there is value in a review conducted by the agency itself of its own performance, it was only going to be in the subsequent scrutiny and dialogue, as outsiders tested the analysis and conclusions the Bank itself has reached. But never mind that says Robertson, I’ll just reappoint Adrian anyway. Perhaps the Bank has a really compelling case around its stewardship of monetary policy – and just the right mix of contrition and context etc – but we don’t know (and frankly neither does Robertson – who has no expertise in these matters, and who appointed a Reserve Bank Board -the people who formally recommend the reappointment – full of people with almost no subject expertise).

But, as I say, the reappointment was hardly a surprise.

It could have been different. I’ve seen a few people say it would have been hard to sack Orr, but I don’t think that is so at all. No one has a right to reappointment (not even a presumptive right) and Robertson could quite easily have taken Orr aside a few months ago and told him that he (Orr) would not be reappointed, allowing Orr in turn the dignity of announcing that he wouldn’t be seeking a second term and would be pursuing fresh opportunities (perhaps Mark Carney would like an offsider for his climate change crusades?) Often enough – last week’s FEC appearance was just the latest example – Orr’s heart doesn’t really seem to be in the core bits of the job.

There are many reasons why Orr should not have been reappointed. The recent inflation record is not foremost among them, although it certainly doesn’t act as any sort of mitigant (in a way that an unexpectedly superlative inflation record in a troubled and uncertain world might – hypothetically – have).

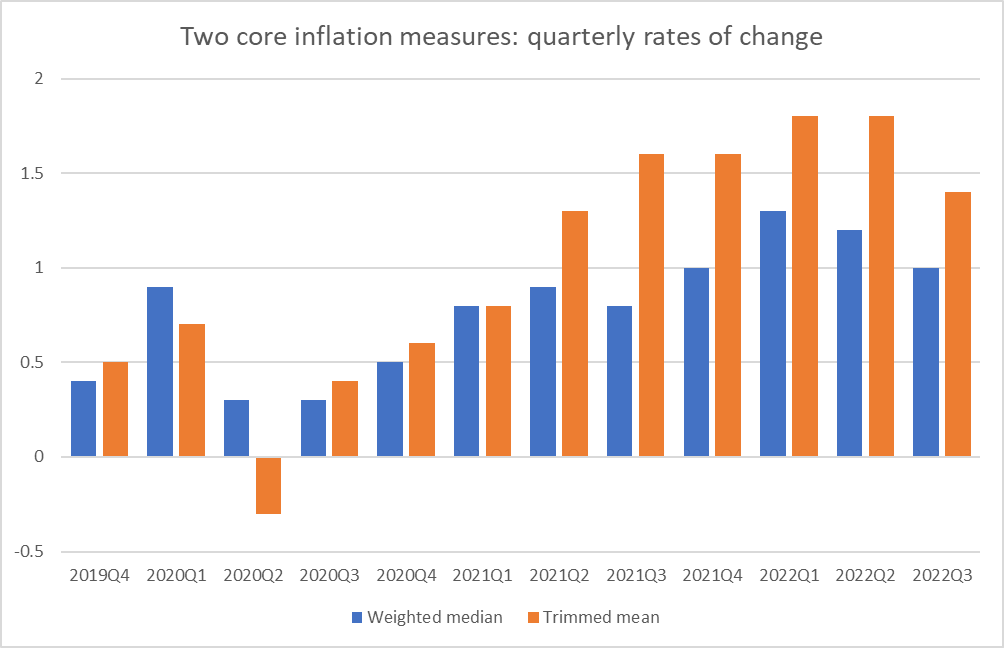

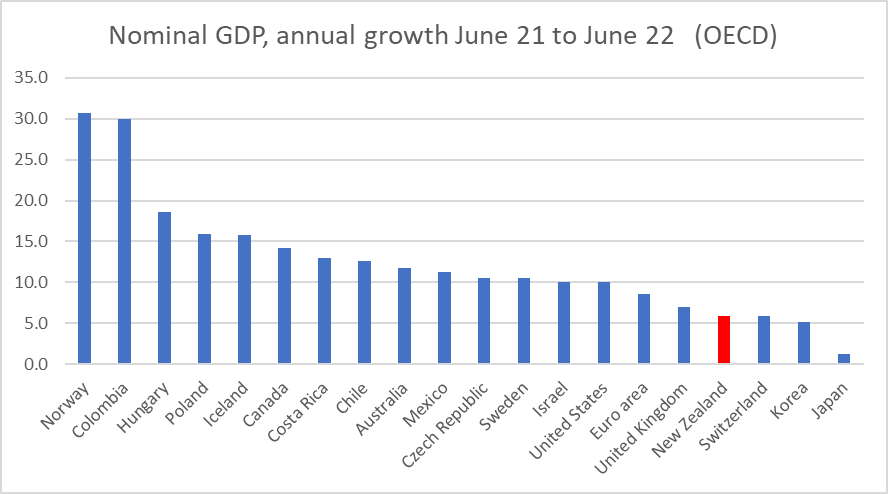

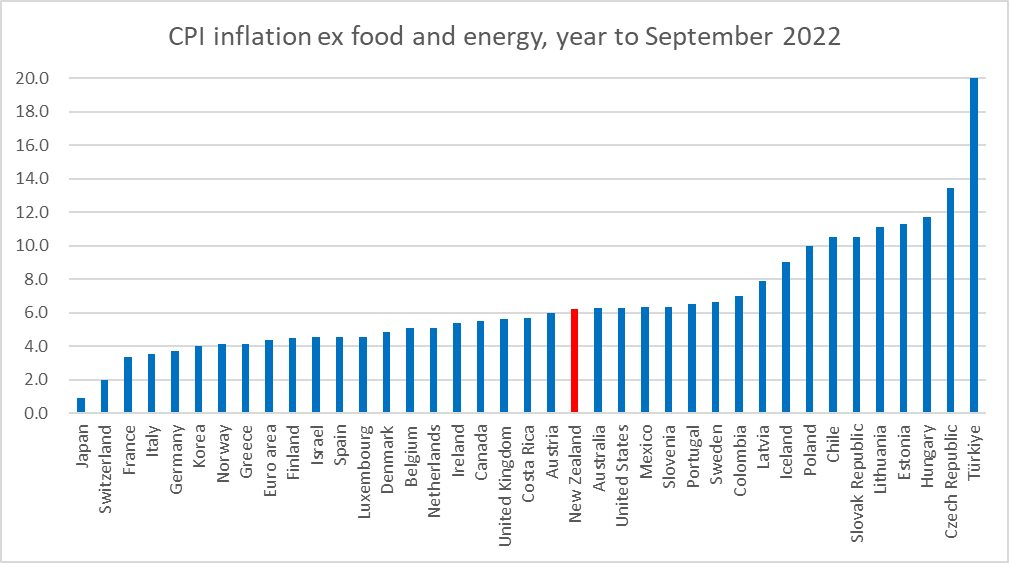

There is nothing good, admirable, or even “less bad than most” about the inflation record. This chart is from my post last week

A whole bunch of central banks made pretty similar mistakes (and the nature of floating exchange rates is that each central bank is responsible for its country’s own inflation rate). Among the Anglo countries, we are a bit worse than the UK and Canada and slightly less bad than the US and Australia. Among the small advanced inflation targeters – a group the RB sometimes identified with – we have done worse than Switzerland, Norway, and Israel, and better than Sweden and Iceland. In a couple of years (2021 and 2022) in which the world’s central bankers have – in the jargon – stuffed up badly, Orr and his MPC have been about as bad on inflation as their typical peers.

You could mount an argument – akin to Voltaire on the execution of Admiral Byng – that all the world’s monetary policymakers (at least those without a clear record of dissent – for the right reasons – on key policy calls) should be dismissed, or not reappointed when their terms end, to establish that accountability is something serious and to encourage future policymakers to do better. You take (voluntarily) responsibility for inflation outcomes, and when you fail you pay the price, or something of the sort. Inflation failures – including the massive unexpected wealth redistributions – matter.

Maybe, but it was never likely to happen, and it isn’t really clear it should. As I’ve noted here in earlier posts until well into 2021 the Reserve Bank’s forecasts weren’t very different from those of other forecasters, and I’m pretty sure that was also the case in other countries. Inflation outcomes now (year to September 2022) are the result of policy choices 12-18 months earlier. With hindsight it is clear that monetary policy should have been tightened a lot earlier and more aggressively last year, but last February or even May there was hardly anyone calling for that. Absent big policy tightenings then, it is now clear it was inevitable that core inflation would move well outside the target range. There are plenty of things to criticise the Bank for – including Orr’s repeated “I have no regrets” line – but if one wants to make a serious case for dismissing Orr for his conduct of monetary policy it is probably going to have to centre on (in)actions from say August 2021 to February 2022 (whereafter they finally stepped up the pace) but on its own – it was only six months – it would just not be enough to have got rid of the Governor (even just by non-reappointment). The limitations of knowledge and understanding are very real (and perhaps undersold by central bankers in the past), and even if Orr and the MPC chose entirely voluntarily to take the job (and all its perks and pay) those limitations simply have to be grappled with. Were New Zealand an outlier it might be different. Had the Bank run views very much at odds with private forecasters etc it might be different. But it wasn’t.

I am, however, 100 per cent convinced that Orr should not have been reappointed. I jotted down a list of 20 reasons last night, and at that I’m sure I’ve forgotten some things.

I’m not going to bore you with a comprehensive elaboration of each of them, most of which have been discussed in other posts. but here is a summary list in no particular order:

- the extremely rapid of turnover of senior managers (in several case, first promoted by Orr and then ousted) and associated loss of experience and institutional knowledge

- the block placed – almost certainly at Orr’s behest – on anyone with current and ongoing expertise in monetary policy nad macroeconomic analysis from serving as an external member of the MPC

- the appointment as deputy chief executive responsible for macroeconomics and monetary policy (with a place on the MPC) of someone with no subject expertise or relevant background

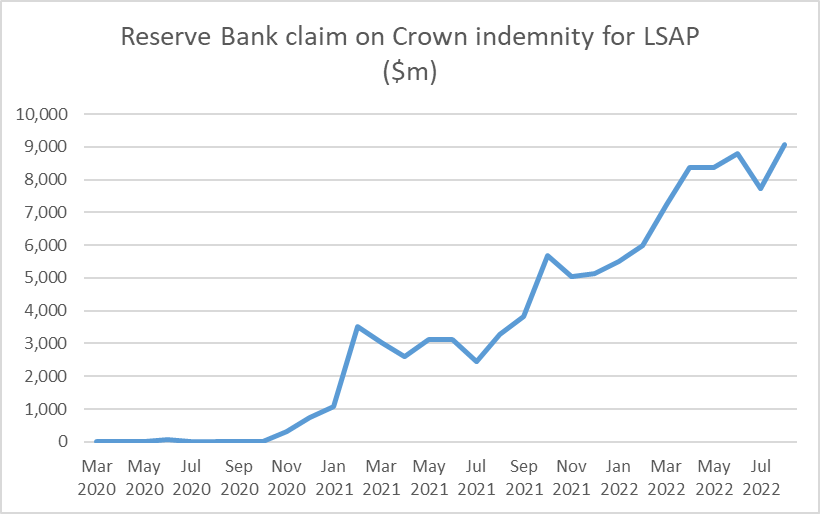

- $9.5 billion of losses on the LSAP – warranting a lifetime achievement award for reckless use of public resources – with almost nothing positive to show for the risk/loss

- the failure to ensure that the Bank was positioned for possible negative OCRs (having had a decade’s advance warning of the issue), in turn prompting the ill-considered rush to the LSAP

- the failure to do any serious advance risk analysis on the LSAP instrument, as being applied to NZ in 2020

- the sharp decline in the volume of research being published by the Reserve Bank, and the associated decline in research capabilities

- the way the Funding for Lending programme, a crisis measure, has been kept functioning, pumping attractively-priced loans out to banks two years after the crisis itself had passed (and negative OCR capability had been established)

- lack of any serious and robust cost-benefit analysis for the new capital requirements Orr imposed on banks (even as he repeatedly tells us how robust the system is at current capital levels)

- repeatedly misleading Parliament’s Finance and Expenditure Committee (most recently, his claim last week that the war was to blame for inflation being outside the target range), in ways that cast severe doubts on his commitment to integrity and transparency

- his refusal to ever admit a mistake about anything (notwithstanding eg the biggest inflation failure in decades)

- the fact that four and a half years in there has never been a serious and thoughtful speech on monetary policy and economic developments from the Governor (through one of the most turbulent times in many decades)

- Orr’s active involvement in supporting and facilitating the appointment of Board members with clear conflicts of interest (Rodger Finlay especially, but also Byron Pepper)

- his testiness and intolerance of disagreement/dissent/alternative views

- his often disdainful approach to MPs

- his polarising style, internally and externally

- all indications are that he is much more interested in, and intellectually engaged by, things he isn’t responsible for than for the things Parliament has charged him with

- organisational bloat (think of the 17-20 people in the Communications team or the large number of senior managers now earning more than $400000 pa)

- the distraction of his focus on climate change, but much more so the rank dishonesty of so much of it – claims to have done modelling that doesn’t exist, attempts to suppress release of information on what little had been done, and sheer spin like last week’s flood stress test. It might be one thing for a bloated overfunded bureaucracy to do work on things it isn’t really responsible for if it were first-rate in-depth work. It hasn’t been under Orr.

- much the same could be said of Orr’s evident passion for all things Maori – in an organisation with a wholesale macroeconomic focus, where the same instruments apply to people of all ethnicities, religions, handedness, political affiliation or whatever. What “analysis” they have attempted or offered has been threadbare, at times verging on the dishonest.

- the failure to use the opportunity of an overhaul of the RB Act to establish a highly credible open and transparent MPC (instead we have a committee where Orr dominates selection, expertise is barred, and nothing at all is heard from most members)

And, no doubt, so on. He is simply unfit to hold the office, and all indications are that he would have been so (if less visibly in some ways) had Covid, and all that followed (including inflation), never happened.

But the crowning reason why Orr should not have been reappointed is that doing so has further politicised the position, in a most unfortunate way.

In the course of the overhaul of the Reserve Bank Act, Grant Robertson introduced a legislative requirement that before appointing someone as Governor the Minister of Finance needed to consult with other parties in Parliament (parallel provision for RB Board members). It was a curious provision, that no one was particularly pushing for (in most countries the Minister of Finance or President can simply appoint the Governor, without even the formal interposition of something like the RB Board), but Robertson himself chose to put it in. The clear message it looked to be sending was that these were not only very important positions but ones where there should be a certain measure of cross-party acceptance of whoever was appointed, recogising (especially in the Governor’s case) just how much power the appointee would wield. That provision never meant that governments could not appoint someone who happened to share their general view of the world and economy, but there was a clear expectation that whoever was appointed would be sufficient to command cross-party respect for the person’s technical expertise, non-partisan nature, dispassionate judgement and so on. Robertson simply ignored Opposition dissents on a couple of the Board appointees. That was of second order significance, but it is really significant in the case of the Governor. It isn’t easy to dismiss a Governor (and rightly so) so for a Minister of Finance to simply ignore the explicit unease and opposition of the two main Opposition parties in Parliament is to make a mockery of the legislation Robertson himself had put in place so recently. The Opposition parties are being criticised in some places (eg RNZ this morning) for “politicising the position/appointment” but they seem to have been simply doing their job – it was Parliament/Robertson who established the consultation provision – and the consultation provisions, if they meant anything, never meant giving a blank slate for whomever the Minister wanted to offer up, no matter the widely-recognised concerns about such a nominee. No one has a right to reappointment and when it was clear that the main Opposition parties would not support reappointment, Robertson should have taken a step back, called Adrian in and told him the reappointment could not go ahead, in the longer-term interests of the institution and the system. If you were an Orr sympathiser, you might think that was tough, but….no one has right to reappointment, and the institution matters.

And, of course, now the position of the Governor has inevitably been put into play, with huge uncertainty as to what might happen if/when National/ACT form a government after the election next year. (And here is where I depart from National’s stance – I never liked the idea of a one year appointment, made well before the traditional pre-election bar on new permanent appointments. We want able non-partisan respected figures appointed for long terms (it is the way these things work in most places), not for each incoming PM to be able to appoint his or her own Governor.)

A few months ago, anticipating that Orr would probably be reappointed, I wrote a post on what an incoming government next year could do about the Bank. The key point to emphasise is that a new government cannot simply dismiss a Governor they don’t like (or nor should they be able to). I saw a comment on a key political commentary site this morning noting that the process for dismissal isn’t technically challenging, which is true, but the substantive standards are quite demanding (the Governor can be dismissed only for specific statutory causes, and for (in)actions that occurred in his new term (which doesn’t start until March)). Generally, we do not want Governors to be able to be easily dismissed (in most countries it is even harder than in New Zealand). More to the realpolitik point, any dismissal could be challenged in the courts, and no one would (or should) want the prolonged uncertainty (political and market) such actions might entail. Moreover, senior public figures cannot just be bought out of contracts.

We still don’t know – and perhaps they don’t either – how exercised National and ACT would be about any of this were they to form a government next year, but unless Orr was himself minded to resign (as the Herald’s columnist suggests might happen) things would have to be handled carefully and indirectly (perhaps along lines in that earlier post of mine) to change the environment and the incentives around the institution. Most of those changes should be pursued anyway, to begin to fix what has been done over the last few years And if Orr were to be inclined not to stick around for long, perhaps an offer of appointment as High Commissioner to the Cooks Islands might smooth his way?