Going through some old papers to refresh my memory on capital gains tax (CGT) debates, I found reference to a note I’d written back in 2011 headed “A Capital Gains Tax for New Zealand: Ten reasons to be sceptical”. Unfortunately, I couldn’t find the note itself, so you won’t get all 10 reasons today. But here are some of the reasons why I’m sceptical of the sort of real world CGTs that could follow from this year’s election. Mostly, repeated calls for CGTs – whether from political parties, or from bodies like the IMF and OECD – seem to be about some misplaced rhetorical sense of “fairness” or are cover for a failure to confront and deal directly with the real problems in the regulation of the housing and urban land markets.

Anyway, here are some of the points I make:

- in a well-functioning efficient market, there are typically no real (ie inflation adjusted) expected capital gains. An individual participant might expect an asset price to rise for some reason, but that participant will be balanced by others expecting it to fall. If it were not so then, typically, the price would already have adjusted. In well-functioning markets, there aren’t free lunches. It also means that, on average, capital losses will be pretty common too, and thus a tax system that treated capital gains and losses symmetrically wouldn’t raise much money on average over time. A CGT is no magic money tree. And there is no strong efficiency argument for taxing windfalls.

- if you thought, for some reason, that people were inefficiently reluctant to take risk, there might be some argument for a properly symmetrical CGT. In such a system, the government would take, say, a third of your gains, but would also remit a third of your losses (the overall risks being pooled by the state). The variance of an individual’s private after-tax returns would be reduced, and they might be more willing to take risk. But, in fact, no CGT system I’m aware of is properly symmetrical – there are typically tough restrictions on claiming refunds in respect of capital losses (one might only be able to do so by offsetting them against future gains). There are some reasonable base-protection arguments for these restrictions, but they undermine the case for a CGT itself.

- All real world CGTs are based on realised gains (and losses to an extent). That makes it not a pure CGT, but in significant part a turnover tax – if you never trade, you never pay (“never” isn’t literal, but tax deferred for decades discounts to a very small present value). And that creates lock-in problems, where people are very reluctant to sell, even if their circumstances change or if a new potential owner could make much more of the asset, for fear of crystallising a CGT liability. In other words, introducing a CGT introduces a new inefficiency to asset markets, making it less likely that over time assets will be owned by the parties best able to utilise them.

- Basing a CGT on realised gains will also, over time, bias the ownership of assets subject to CGT to those most able to avoid realising the gains. A long-lived pension fund, or even a very wealthy family, will typically be better able to count on not having to sell than, say, an individual starting out with one or two rental properties, or some other small business, where changed circumstances (eg a recesssion or a divorce) might compel early liquidation. Large funds are also typically better able to take advantage of loss-offsetting provisions. The democratisation of finance and asset holding it certainly isn’t.

- CGTs in many countries exclude “the family home” altogether. In other countries, they provide “rollover relief”, enabling any tax liability to be deferred. Most advocates of a CGT here seem to favour the exclusion of the family home, even though unleveraged owners of family homes already have the most favourable tax treatment in our system. Again, a CGT applied to investment properties but not owner-occupied ones would simply trade one (possible) distortion for another.

- In practice, most of the arguments made for a CGT in New Zealand have to do with the housing market. But, on the one hand, all major (and minor?) parties claim that they have the fix for the housing market (various combinations of RMA reform, infrastructure reforms, changes to immigration, restrictions on foreign ownership, state building programmes or whatever). If they are right, there is no reason to expect significant systematic real capital gains in houses. If anything, real house prices should be falling – a long way, for a long time. Of course, prices in some localities might still rise at some point, if unexpected new opportunities appear. But “unexpected” is the operative word. Enthusiasm for a CGT, at least at a political level, seems to involve a concession that the parties don’t believe, or aren’t really serious about their housing reform policies.

- Oh, and no one I’m aware of anywhere argues that a realisation-based CGT applied to (a minority of) housing has made any very material difference to the level of house prices, or indeed to cycles in house prices.

- In general, capital gains taxes amount to double-taxation. Think of a business or a farm. If the owner makes a success of the business, or product selling prices improve, expected profits will increase. If and when those profits are achieved, they would, in the normal course of affairs, be subject to income tax. The value of the business is the discounted value of the expected future profits. It will rise when the expected profits rise. Tax that gain and you will be taxing twice the same increase in profits – only with a CGT you tax it before it has even happened. Of course, at least in principle, there is a double deduction for losses, but as noted above utilising losses (whether of income, or capital) is a lot more difficult. If you think that New Zealand has had less business investment than might, in some sense, have been desirable, you might want to be cautious about applauding a new tax that would fall heavily on those who took business risks and succeeded.

- Perhaps double taxation of expected business profits doesn’t bother you. But trying reasoning by analogy with wages. If the market value of your particular skills has gone up, your wages would be expected to rise. When they do you will pay taxes on those higher wages. But by the logic of a CGT, we should capitalise the value of your expected future labour income and tax your on both that “capital gain” and on the later actual earnings. Fortunately, we abolished slavery long ago, but in principle the two cases aren’t much different: if there is a case for a CGT on the value of a business, it isn’t obvious why one shouldn’t have one on the value of a person’s human capital.

- (I should note here, for the purists, that there are other concepts of double-taxation often referred to in tax literature, none of which invalidate the point I’m making here.)

- Real world CGTs also tend to complicate fiscal management? Why? Because CGT revenue tends to peak when asset markets and the economy are doing well, and when other government revenue sources are performing well. CGT revenue doesn’t increase a little as the economy improves and asset markets increase, it increases multiplicatively. And then dries up almost completely. Think of a simple example in which real asset prices had been increasing at 1 per cent per annum, and then some shock boost asset prices by 10 per cent. CGT revenue might easily rise by 100 per cent in that year (setting aside issues around the timing of realisations). And then in a period of falling asset prices there will be almost no CGT revenue at all. Strongly pro-cyclical revenue sources create serious fiscal management problems, because in the good times they create a pot of money that invites politicians to (compete to) spend it. If asset booms run for several years, politicians start to treat the revenue gains as permanent, and increase spending accordingly. And if/when asset markets correct – often associated with recession and downturns in other revenue sources- the drying up of CGT revenue increases the pressure on the budget in already tough times. It is easy to talk about ringfencing such revenue (mentally, if not legally) but such devices rarely seem to work.

None of this means that I think there is no case for changes in elements of our tax system as they affect housing. The ability for business borrowers to deduct the full amount of nominal interest, even though a significant portion of that interest is simply compensation for inflation (rather than a real cost), is a systematic bias. It doesn’t really benefit new buyers of investment properties (the benefit is, in principle, already priced into the market) but it is a systematic distortion for which there is no good economic justification Inflation-indexing key elements of our tax system is highly desirable – at least if we can’t prudently lower the medium-term inflation target – and might be a good topic for a tax working group. In the process, it would also ease the tax burden on people reliant on fixed interest earnings (much of which is also just inflation compensation, not a real income).

Of course, at the same time it would be desirable to look again at a couple of systematic distortions that work against owners of investment properties. Houses are normal goods and (physically) depreciate. And yet depreciation is no longer deductible. Perhaps there was a half-defensible case for that when prices were rising seemingly inexorably – but even then most of the increase was in land value, not in value of the structures on the land – but there is no justification if land reform and (eg) new state building is going to fix the housing market. Similarly, when the PIE system was introduced a decade or so ago, it gave systematic tax advantages to entities with 20 or more unrelated investors. Most New Zealand rental properties historically haven’t been held in such entities. There is no good economic justification for this distinction, which in practice both puts residential investment at a relative tax disadvantage as a saving option, and creates a bias towards institutional vehicles for holding such assets. Institutional vehicles have their own fundamental advantages – greater opportunities for diversification and liquidity – but it isn’t obvious why the tax system should be skewing people towards such vehicles rather than self–managed options. As noted above, any CGT will only reinforce that bias. Funds managers, and associated lawyers and accountants, would welcome that. It isn’t obvious why New Zealand savers should do so.

I see that there are more than 10 bullet points in the list above. I’m not sure it covers all the issues I raised in my paper a few years ago, but it is enough to be going on with.

And in all this in a country where we systematically over-tax capital income already. I commend to readers a comment on yesterday’s tax post by Andrew Coleman, of Otago University (and formerly Treasury). As Andrew noted:

Somehow, New Zealand’s policy advising community decided it would restrict most of its attention to the ways income tax could be perfected rather than question whether income taxes (which are particularly distortionary when applied to capital incomes) should be replaced by other taxes. It is almost as if we have the Stockholm Tax Syndrome – fallen in love with a system that abuses us.

A broad-based capital gains tax would just reinforce that problem.

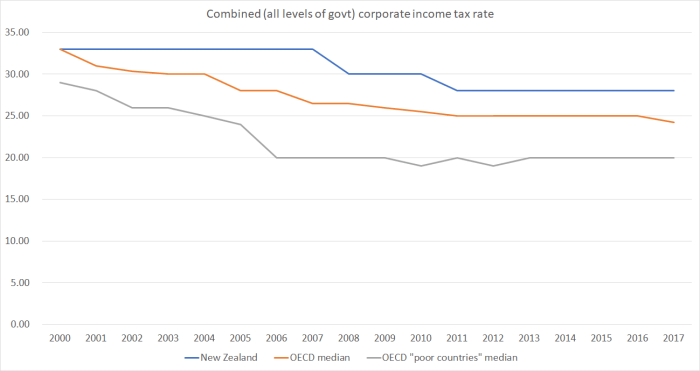

Of the “poor” OECD countries, only Mexico and Portugal now have higher company tax rates than we do. Whereas most of the “poor” countries are closing the income/productivity gaps to the richer OECD countries, Mexico and Portugal (and New Zealand) aren’t. I’m not suggesting it is the only factor by any means, just highlighting the choice that the more successful converging countries have been making.

Of the “poor” OECD countries, only Mexico and Portugal now have higher company tax rates than we do. Whereas most of the “poor” countries are closing the income/productivity gaps to the richer OECD countries, Mexico and Portugal (and New Zealand) aren’t. I’m not suggesting it is the only factor by any means, just highlighting the choice that the more successful converging countries have been making.

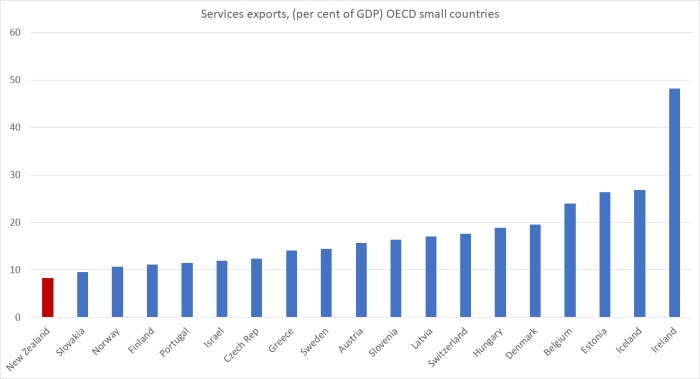

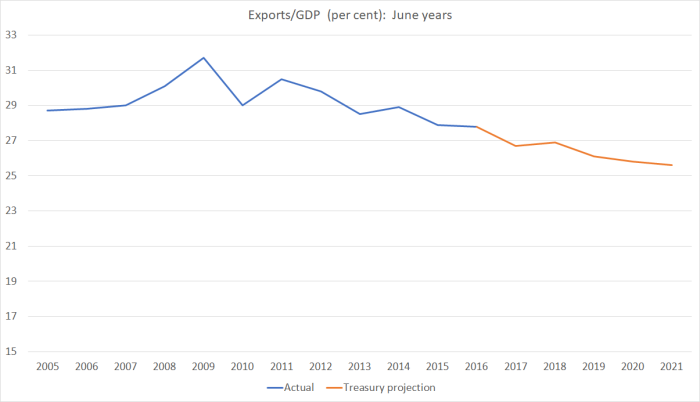

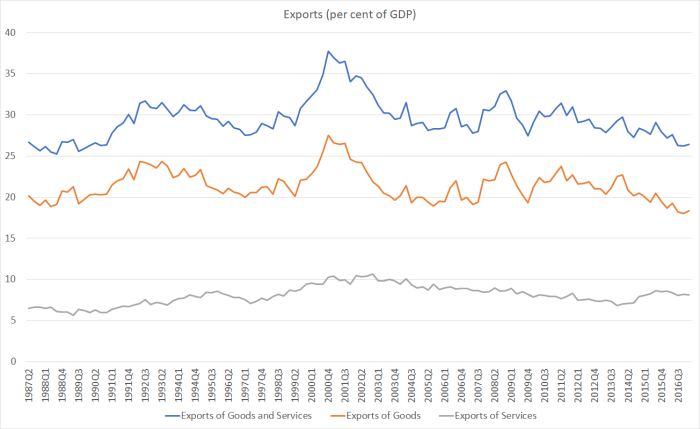

It is easy for one’s eye to go to those peaks in 2000 – at a time when the exchange rate had fallen sharply – but even much more recently the trends haven’t been favourable. Even the vaunted services exports are lower now as a share of GDP than they were 10 years ago, or than when the government came to power. The Minister talked of “high-tech value-added manufacturing” as the future, but then overall goods exports are lower as a share of GDP now than at any time in the last 30 years.

It is easy for one’s eye to go to those peaks in 2000 – at a time when the exchange rate had fallen sharply – but even much more recently the trends haven’t been favourable. Even the vaunted services exports are lower now as a share of GDP than they were 10 years ago, or than when the government came to power. The Minister talked of “high-tech value-added manufacturing” as the future, but then overall goods exports are lower as a share of GDP now than at any time in the last 30 years.