Eric Crampton of the New Zealand Initiative yesterday sent out a couple of tweets drawn from some pages a reader had sent him from Wellington’s evening newspaper of 18 July 1984. The general election had taken place on the 14th and the foreign exchange market had been officially closed for a couple of days as everyone awaited resolution of the political disputes around who would take responsibility for the by-now-inevitable devaluation. The outgoing (but still caretaker) Prime Minister finally buckled and a 20 per cent devaluation was announced on the 18th. It marked the beginning of almost ten years of pretty thoroughgoing economic reforms, the legacy of which (good and ill) is still with us today.

Anyway, here were Eric’s tweets

(Click on the right-hand side of the first page and you can read a “fake news” story from 1984, how the Evening Post fell for a Michael Cullen hoax press release.)

Eric’s tweets sent me down to the garage and my box of old newspapers from (in)auspicious days. I didn’t have that particular one, but I did find one from a couple of days earlier. In that paper there was an advert for a competition offering as a prize a microwave with a retail value of $1495 – $4800 in today’s money. Whether you run with Eric’s microwave advert or mine, there is no doubt some things are dramatically cheaper (in real terms) than they were then. Of course, for many technology items that will be true everywhere; it isn’t primarily a New Zealand story. Actually, flicking through that old paper it was the car prices that surprised me more: a two-year old Ford Cortina advertised for $18995 ($61000 in today’s money). The New Zealand car assembly industry then really was very heavily protected.

Eric notes “we forget too quickly what a mess the place was in”, which reads a little oddly when he did not, I gather, come to New Zealand for another 20 years. But setting that quibble to one side, and taking on board my own youthful enthusiasm for most or all of the reforms being done at the time (most of which still seem right and/or necessary), I think that with the benefit of hindsight the picture is rather more mixed than perhaps Eric suggests.

On the macro side, the problems were all-too-evident. Fiscal imbalances were large and the balance of payments current account deficit was large. If debt levels (government and external) weren’t that high by the standards which too much of the advanced world has since become used to, they were a huge departure from New Zealand’s post-war experience. Inflation was partially suppressed by a series of freezes – although Muldoon had lifted the price freeze a few months earlier – supported by a series of interest rate controls, which were undoing the partial financial liberalisation of the 1970s. Outside the control of any government, the terms of trade had been trending down for 20 years, and New Zealand material living standards and productivity had been falling behind those nearer the upper ranks of the OECD group. We were still in the construction phase of that disastrous set of wealth-destroying government sponsored energy projects known as “Think Big”. And if protective barriers were slowly being removed – for example, CER was inaugurated the previous year – it was a slow and halting journey at best. High protective barriers not only made many goods unnecessarily expensive to New Zealand consumers, but acted as a heavy tax on actual and potential New Zealand exporters. Much about the tax system was in a mess.

And yet, and yet.

The unemployment rate in June 1984 (from Simon Chapple’s work backdating the HLFS) is estimated to have been 4.4 per cent. Right now it is 4.3 per cent – and 4.3 per cent is well below the average for the last 20 years, while the 1984 was well above the comparable average.

Or house prices. I started looking to buy a first house a few months later, in early 1985. Single 22 year olds could do that sort of thing in those days. Yes, concessional Reserve Bank staff mortgages would have helped, but I recall looking at various houses in Island Bay and Newtown for about $80000. That’s less than $250000 in today’s money. The same houses now look to be perhaps $750000. That mess was created by some of the post-1984 reforms.

Or productivity. In that old newspaper I dug out of the garage I found a post-election op-ed written by Len Bayliss, then a leading New Zealand economist. Among the five major economic challenges he identified for the new government was this

Fifth – extremely poor productivity growth, and more recently GDP growth, have been the subject of a series of economic reports since 1962. As a consequence of this poor performance, other countries’ living standards have risen more than New Zealand’s.

The worst single period for productivity growth in New Zealand history was in late 1970s, but even 35 years ago people knew that the problems were much more deep-seated. Unfortunately, of course, the productivity gaps are now larger than they were in 1984. On OECD estimates of real GDP per hour worked, in 1984 we were close to the levels in Iceland, Ireland, and Finland. These days, we are far behind each of them. We were only about 10 per cent behind the UK in those days, and now they are about 30 per cent ahead of us. Things might not be in such a “mess” nowadays – disorderly macro imbalances and weird interventions – but the economic bottom line still makes sorry reading. No champion of change in 1984, told all the policies that would be adopted and the huge measure of macro stability achieved, would have predicted that we’d have drifted further behind by 2019.

Perhaps especially if they’d been given the additional information of what would happen to New Zealand’s terms of trade over the subsequent decades – the turnaround (outside any government’s control) starting just a couple of years after the reform period got underway.

The devaluation in July 1984 was a huge part of the economic narrative at the time. There was a strongly-held consensus, among local officials, local commentators (it is explicit in that Len Bayliss article) and international agencies, that the New Zealand real exchange rate had become persistently out of line with fundamentals, and that a substantial and sustained depreciation would have to be a significant part of putting the economy on a better-footing. It was, among other things, a repeated and urgent theme of the numerous meetings I attended, as a junior note-taking official, in late 1984.

And here are the two OECD measures of New Zealand’s real exchange rate.

I’ve marked the 1984 devaluation. In real terms, it proved very temporary indeed. It would be great if really strong and sustained productivity growth had supported a structural increase in the real exchange rate. But that, of course, hasn’t been the story. Once we got through the disinflation period – when it was reasonable to expect some temporary periods with a high real exchange rate – it seems to reflect the same sort of domestic demand pressures that have given us persistently among the very highest real interest rates in the advanced world.

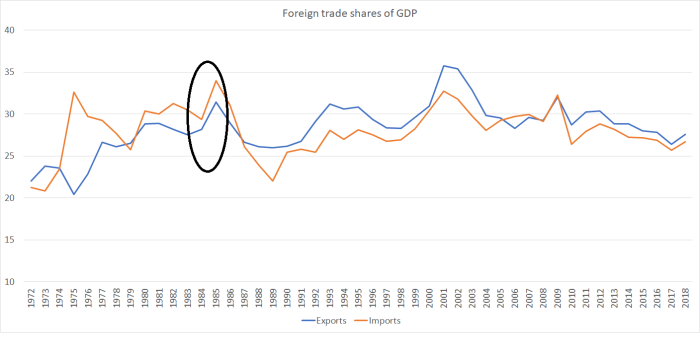

And then there is foreign trade. A narrative at the time was the heavy protection had resulted in New Zealand’s foreign trade shares of GDP falling, or failing to grow. The overvalued exchange rate (see above) further impeded the prospects of potential export industries, probably only partly offset by the various (highly questionable) export incentives and subsidies.

And yet

I’ve circled the data for the years to March 1984 (latest actuals when the devaluation happened) and for the year to March 1985. There was, as you would expect, a short-term boost to the nominal trade shares on account of the devaluation, but of course that didn’t last. But if we take the subsequent 33 years together, there is just no sign of foreign trade having become more important to the New Zealand economy (as it happens, exports as share of GDP in the year to March 2018 were almost identical to those in the year to March 1984). Only one other OECD country has not seen the export share of GDP increase over that time.

I don’t want to kick off a futile debate about whether the reforms should have been done. I’m still squarely in the camp that most should have been. But, equally, nothing is gained by pretending to a degree of economic success we haven’t achieved. We’ve shared – with every market economy (and probably the non-market ones too) – the rapid declines in the cost of various technology goods and services. All of our own doing, we’ve managed to bring about, and sustain, an impressive level of macroeconomic stability. But, equally all of our own doing, we’ve managed to rig the housing market against the current (and next) young generation, and despite reducing or removing all manner of protective barriers (and even getting other countries to do something similar for stuff New Zealand firms exports), foreign trade shares are no higher now than they were on that momentous day in 1984. And, as for productivity, poor – and rightly alarming – as it was then, all indications are that it is worse now, and there are no signs of those gaps beginning to close.

The New Zealand economy isn’t in some disorderly mess at present. But if it is perhaps more orderly, it is failing nonetheless.

{kind=link}