You may, like me, be intrigued by the stories emerging from Australia about falling house prices. The fall in nationwide house prices isn’t that large – still less than we experienced in New Zealand in 2008 – but (a) the economy isn’t in a recession, and (b) there is little sign yet that the falls are about to end soon. Lower house prices would seem likely to mostly be “a good thing” – cheaper goods and services typically are – and the banks are well-capitalised to cope with even some serious combination of bad economic times and falling house prices. But on the other hand, whatever was causing this particular fall, I’d heard little to suggest that land-use rules were being substantially liberalised in Australia (any more than in New Zealand), so I’ve been – and remain – quite sceptical about the idea that Australian house prices would fall sharply and stay down. And, of course, of anything similar in New Zealand.

Time will tell, but out of curiosity I decided to dig out a few numbers. The first was a comparison of residential investment as a share of GDP. This chart is in nominal (current price terms).

And this is in real terms (which isn’t strictly kosher and is an approach frowned on by SNZ, but some analysts do it anyway).

There are differences between the two charts, but the bit that caught my eye was that New Zealand has been devoting a larger share of GDP to house-building (and additions and alternations etc) than Australia for almost the entire decade.

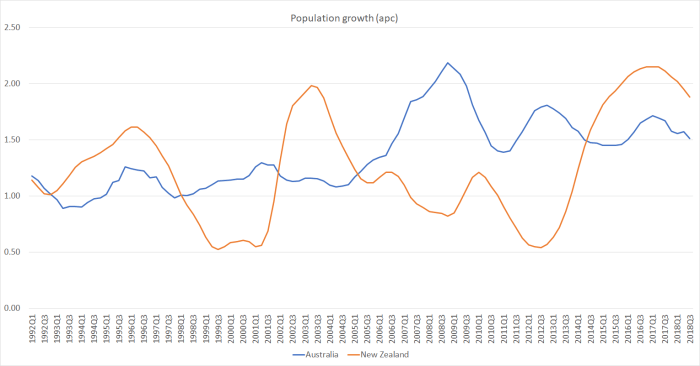

Population growth is one of the biggest determinants of how much accommodation will be demanded. Here is annual population growth in the two countries.

Over the last four to five years, our population growth rate has run quite a bit ahead of Australia’s. All else equal, one percentage point faster population growth requires something like two percentage points of GDP larger share of residential investment (the net stock of residential dwellings – themselves depreciated – is well above 100 per cent of GDP).

At least two other things complicate comparisons. First, a big chunk of residential investment spending in New Zealand for several years after the Canterbury earthquakes was about repair and rebuild, not adding to the housing stock (relative to the pre-quake situation) at all. There was nothing comparable in Australia, and so all else equal one should have expected a larger share of resources devoted to housebuilding here than in Australia. And the other relevant factor is that intensification often involves the demolition (and loss) of existing dwellings: even in normal (non-quake) times not all new dwelling approvals add to the housing stock.

New Zealand has a reasonably long-running quarterly series on the estimated number of private dwellings. I could only find the comparable Australia series back to 2011. But this is what trends in the number of people per dwelling look like over the last few years.

On the face of it, that is a pretty startling difference. (I did find reference to some Australia census data suggesting that in 1991 population per dwelling in Australia was also around 2.7.)

A declining ratio of people per dwelling is what might one expect in functioning house and land markets. After all, both countries are getting richer, birth rates are lower than they used to be, people are living longer (ie a larger share of life after kids have left home), lifelong marriage from an early age doesn’t seem to be becoming more a thing. But it – a fall in the ratio – is much harder to achieve when regulatory obstacles mean house prices are driven sky-high. Then people squash together a bit more.

Another way of looking at the last few years of that chart is that over the seven years to September 2018 Australia had population growth of 11.8 per cent and the stock of dwellings increased by 12.7 per cent. In New Zealand, over the same period, the population is estimated to have risen by 11.6 per cent and the stock of dwellings increased by only 8.6 per cent. For the entire housing stock – slow-moving at best – that is a really big difference.

I haven’t mentioned (a) the large share of apartments built in Australia in recent years (which some look on favourably – the Reserve Bank here always used to tout that record – and others are more inclined to mutter about future potential urban slums etc), or (b) differences in credit conditions on the two sides of the Tasman (responsible, on some tellings, for the recent weakness of the housing market).

But looking across the numbers I’ve presented here, and bearing in mind that there has been little or no effective liberalisation of land use laws in New Zealand (or a fix to the construction products market), it is hard to see any good reason to expect that we will see any material or sustained drop in house and urban land prices here.

There will be a recession along eventually, ringfencing and a capital gains tax (both dubious new economic distortions) might dampen things a little, and the Reserve Bank’s capital proposals if implemented might exacerbate any downturn, but in the end if land remains artifically scarce (a bit like new cars in 1950s New Zealand) it remains hard to envisage a serious or substantial adjustment. And responsibility for that failure – and failure it is – has to be sheeted home to the political parties that vie to govern us, notably National and Labour.

> And responsibility for that failure – and failure it is – has to be sheeted home to the political parties that vie to govern us, notably National and Labour.

Responsibility? When have those greedy bumblers ever took responsibility for anything?

LikeLike

Well indeed. But then neither does the public find ways to demand it effectively – National and Labour together are as dominant (vote share) now as at any time since MMP came in.

I’m hoping for a courageous compelling (decent) effective outsider with the capacity to disrupt NZ politics. (No sign of anyone of that ilk on the horizon tho)

LikeLike

It is usually the minor parties that prop up the government that block key legislation from being passed.

LikeLike

True, but there has never been anything to stop National and Labour getting together to pass serious reforming legislation in this area. Both, in succession, have claimed they want reform and systematic liberalisation. National did v little, and Labour (early days) have done nothing.

LikeLiked by 1 person

Unlike the US that use the term Republican or Democrats or bi partisan agreement, we just have the Government and Opposition which creates a us against you type situation. Rather hard to be in opposition and to agree with the government.

LikeLike

Without being totally authoritative … but … my reading of the AU housing market is when the Banking Royal Commission got legs and APRA and ASIC came in for a lashing, the banks pulled the plug on interest only loans, and, since that date all interest only loans come up for rollover were forced into Principal and interest loans. That in its own has created the much of the changes. Land regulation isnt6 a recent force3 and will have been constant over the period.

LikeLike

It wouldn’t surprise me if credit conditions played a part, but I’m sceptical it is the main part of the story. It is hard to go past how much new building there has been (relative to population growth), and on my reading credit conditions are usually only an amplifier (up and down).

LikeLike

The amount of apartments approved dropped 49 per cent in the December quarter 2018, compared to the same period a year earlier, official figures on Monday showed

It comes as banks have clamped down on lending to investors, under pressure from the regulator and the financial services royal commission

domain.com.au/news/apartment-approvals-slump-as-investors-stay-cautious-about-falling-prices-798363/?utm_campaign=strap-masthead&utm_source=smh&utm_medium=link&utm_content=pos5&ref=pos1

LikeLike

https://www.domain.com.au/news/apartment-approvals-slump-as-investors-stay-cautious-about-falling-prices-798363/?utm_campaign=strap-masthead&utm_source=smh&utm_medium=link&utm_content=pos5&ref=pos1

LikeLike

But in a sense this makes my point (esp together with Blair’s comment). There were easy credit conditions, there were lots of new apartments (in particular) built, and as the overhang became apparent both banks and their regulators (almost inevitably) got more nervous. Credit conditions amplified the upswing and (now) the downturn.

LikeLike

The Auckland Unitary Plan has liberalised land use. It has done it in such a way that only around half of potential new dwellings would be greenfields rather than intensification of existing areas. But that is an increase nevertheless. Current estimates are that the plan enabled 336,000 commercially feasible developments throughout the city. https://www.greaterauckland.org.nz/2018/01/29/downsizing-aucklands-unitary-plan/ Not nearly enough, in my book, but definitely a step in the right direction.

And it is striking that the Auckland hit its peak in mid-late 2016 – exactly the time (October 2016) when the Unitary Plan was finally passed.

I wouldn’t normally expect land liberalisation to have an immediate effect on prices, but perhaps the market really did price-in future growth immediately prior to and during the passing of the Unitary Plan? Alternatively, there were other factors producing a temporary end to growth in the Auckland market in 2016, and in the long term, the Unitary Plan brought about a long-term end to sustained house price increases.

The UP would explain why Wellington’s prices have continued such a steep increase relative to Auckland in the last 2 years.

LikeLike

The Auckland Unitary plan has certainly made a huge difference towards making land available. Certainly more houses can be built on each site. What is holding me back from building is still the lack of consistency of the application of building standards by Council inspectors. At every step of the building process requires a Council inspection but a separate final inspection can easily override previous inspections already passed at enormous costs to remedy. eg, I had to rebuild a deck and staircase access because at final inspection as it was determined that stainless steel bolts/nuts/nails was the preferred option to galvanised steel after it had already been passed earlier by another inspector. It is not as if this was a seaside property.

LikeLiked by 1 person

I’m a bit more sceptical. My story of Wgtn (or Tauranga) is that it is mostly a catch-up (something similiar happened in the 2000s boom – Akld went up first and then in time the boom spread more widely while Akld was more subdued). To support your story we’ll have to see a sustained narrowing in the Akld/Wgtn spread. Perhaps it will prove to have happened (looking thru the cyclical effects) but it will take some considerable time to know.

I’m a bit more sceptical about the Unitary Plan. There was a little or no sign of peripheral undeveloped land prices falling – and that where the effects should have been most visible – and in a sense all the Plan could be argued to have done was belatedly catch up with another huge surge in population. That has been happening for decades: it isn’t as if people in Akld aren’t housed, but the boundaries are pushed and construction happens belatedly. Land prices don’t go to infinity (so it is not as if land supply is absolutely capped).

But this is one of those issues on which I’d love to find myself wrong.

LikeLike

The other reason I have not been building on my terrace housing and apartment dwelling zoned property is a land regulation issue. On my 697 sqm site I can build only 9 units but if I acquired my neigbours property of a similar size I can build 43 units stacked 3 levels. So now the dilemma of proceeding with 9 units or acquire the neighbour and the big IF is when he decides to sell to be able to build 43 units.

LikeLiked by 2 people

> There was a little or no sign of peripheral undeveloped land prices falling – and that where the effects should have been most visible

But why would a relaxation of constraints on what you can do on a piece of land lead to a *fall* in its price?

Or are you referring to underdeveloped land that was already zoned residential under the AUP? FWIW there is evidence of this effect:

Click to access Land%20use%20regulation,%20the%20redevelopment%20premium%20and%20house%20prices.pdf

We look at developed – not undeveloped – sites, but the model’s result can be extrapolated out to vacant lots, since we condition on the extent of site development.

LikeLike

A key difference is that the Australian price boom was driven heavily by investors and cheap credit often based on misrepresentation of borrowing ability. When that bid vapourised then property prices started falling. In New Zealand, the investor bid dried up a few years ago but has been replaced by owner-occupiers for the reason you describe above.

LikeLike

…..seems to me, supply on the fringes of Auckland has really picked up during the past year or so: Pokeno, Karaka, Hobsenville, Albany etc. – some indication the UP is working? GGS? Might be a bit of pressure here and there but the type of stock on offer is that different to established areas, seems an apples to oranges comparison…??

LikeLike

Pokeno, Karaka, Hobsonville, Albany etc, do use the Unitary Plan for more flexibility in higher density. But usually 2 level buildings that do not take advantage of some of higher level density offered by the Unitary plan. New Lynn for example is a Metropolitan city zoned for 18 level buildings but there is only 1 building cut short at 10 levels in the New Lynn city. The costs and the development risks start to escalate each additional level which tends to scare our limited resourced builders and our Australian banks. The Auckland city high rise developments tend to be funded by chinese developers with deeper pockets.

LikeLike

This used to be kiwi funded by ma and pa investors in 67 Finance companies at a peak had $7.1 billion invested which was collapsed by the RBNZ engineered by the RBNZ.

LikeLike

House prices must keep rising otherwise economic collapse. More credit needs to be created to inflate asset prices and borrow against your house to fund consumption making us all richer bwahhhh.

LikeLike

Hardly a day goes by – here’s another one

LikeLiked by 1 person

This inscrutable made $2,250,000 in one day selling NZ work visas then disappeared – do you think he will pay his taxes – is the IRD on his case

https://www.radionz.co.nz/national/programmes/checkpoint/audio/2018681217/chinese-migrant-workers-we-ve-been-cheated

LikeLike

NPL is National Personnel Limited. Its website explains it’s the brain child of brothers Kevin and Peter O’Connor. It finds contractors for construction companies.

The O’Connor brothers were also behind Poutama Training Institute, which offered basic construction training for cadets, but after cadets complained they were conned and had to sign loan agreements, the NZQA launched an investigation, and says Poutama was never registered.

You forget to mention the O’Connors. The agent does not usually make the core money as he has to organise genuine employment contracts with the hiring companies. The bulk of the $2 million would have to be paid to the hiring company. The agent makes a small percentage of the deal. Usually it works fine unless immigration does not issue the visas and that’s when the guys who paid out start complaining which puts a spanner into the works.

LikeLike

The workers usually know the risk when they paid out their respective $45k. They are fully involved in the con. But of course when things get tough they also would have found out the NZ is a soft touch when it comes to workers, laying the blame entirely on the agent and the employer who are just the facilitator.

When the money is spent. GST would be collected. That is the wonderful thing about GST in NZ. Sooner or later you spend and then you pay your tax.

LikeLiked by 1 person

Note that the $2.25 million is from China paid into an NZ account and would be spent here in NZ a nice boost to the NZ economy As part of our multi billion black market cash economy which incurs GST once you buy goods and services.

LikeLike