There has been a line run in many quarters over recent years suggesting that wage inflation is surprisingly low. There was a bit of that tone in several articles on such issues in the Sunday Star-Times yesterday, and it even appeared in the Leader of the Opposition’s speech last week

For many New Zealanders, incomes are struggling to keep up with the rising cost of living.

We’ll probably see more such stories when the next round of labour market statistics are released later this week.

As I’ve noted in various posts over a couple of years now (including recently), I’m not at all convinced by this story.

My preferrred measure of wage inflation is the Statistics New Zealand analytical unadjusted Labour Cost Index series. The LCI is designed to be stratified – comparing wage inflation for the same jobs (and so not facing the compositional issues the QES measures have) – and the “analytical unadjusted” refers to the idea that these are straight wage measures, not ones that attempt to adjust for individual job productivity changes (as the headline LCI numbers do). The series is only available back to the 1990s, but here is the history.

Nominal wage inflation has picked up a little, but is still well below what people got used to in the five years or so prior to the last recession. But so is inflation for goods and services.

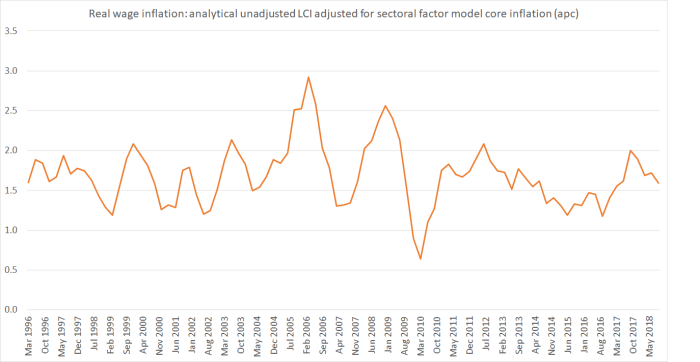

Here is the same wage series adjusted for the Reserve Bank’s sectoral factor model measure of core inflation (I could have used the headline CPI – the averages don’t change materially, but there is a lot more “noise” in the CPI itself).

Two things caught my eye:

- first, each and every year real wages (on aggregate across the economy) have risen – even in the depths of the last recession. It won’t have been (and won’t be) true for every individual, but it is true – at least on these measures (generated by our national statistics agency, and the official agency best placed to tell us about core inflation) – across the economy as a whole.

- second, real wage inflation this decade looks to have averaged not materially different to what we experienced in the late 1990s and 00s. There were individual years where faster wage inflation was recorded, but if there is a systematic weakness in real wage increases this decade compared to what went before, the difference is pretty small. And notwithstanding talk – in those SST articles – that the current labour market is “as good it gets” actually the unemployment rate is still above the lows of the 00s.

All of which is a little strange, because economywide productivity growth has slumped (to basically zero in recent years). Here is a chart of estimated labour productivity back to 1995 when the LCI series starts. I’ve shown it in logs, so that a less steeply rising line accurately illustrates a declining growth rate of productivity.

There is a bit of short-term noise in the series, but the key story is pretty easily visible: growth in labour productivity has been slowing, mostly recently to nothing. All else equal, it should be a bit surprising if there are persistent gains in economywide real wages when there is little or no productivity growth.

Of course, the other consideration that affects economywide potential is the terms of trade. If the terms of trade increase then even if there is no growth in real labour productivity, the overall pot is bigger and – all else equal – it is likely that over time wages will rise to some extent to reflect that improvement. It is a mechanical process, or a certain one, and there is a variety of possible channels, but in an economy that experiences considerable terms of trade variability it isn’t a factor that can simply be overlooked.

I’ve attempted to take account of the terms of trade in this chart, which I ran in post last month.

This chart compares how wages have been rising relative to the increase in nominal GDP per hour worked (the latter measure including both productivity and terms of trade effects). A rising line – as New Zealand has experienced (on these data) this century – suggests that wages have been rising at a faster rate than the earnings potential of the economy. That difference – perhaps 13 percentage points over 17 years – adds up to something quite significant. On its own – taken in isolation – it is neither something necessarily good nor something necessarily bad. There are distributional changes in any economy over time. But it is something that could not continue at the same rate indefinitely (this isn’t a statement of ideology or sophisticated economic argumentation, but simply a matter of basic arithmetic).

Here is another way to look at the issue. The chart shows the OECD’s relative unit labour cost measure of New Zealand’s real exchange rate, in this case back to 1980.

I’ve broken into two the period since liberalisation in 1984. In both periods – although especially the earlier one – there has been plenty of variability in the real exchange rate. But the average in the second half of the period has been far higher than in the first half. Since standard theory tells us to have expected exchange rate overshoots temporarily as part of getting inflation down, I could quite legitimately have focused simply on, say, the 10 years after 1991 and compared them to the more recent period. My point is not that any single point of comparison is somehow the “right” one, simply that in an economy where productivity growth has lagged behind that in most of the rest of the advanced world, there is something anomalous about a real exchange rate as high as ours have been. Since this is a unit labour cost measure, it fits nicely with the previous chart – wages and salaries have been rising faster than the economy’s earnings capacity, and to a greater extent than in many other countries. Consistent with all that, our firms (as a whole) haven’t been able to successfully increase their penetration of world markets (export shares have been flat or falling).

Not this is in any sense the fault of wage-earners, or indeed of individual firms, all of whom are mostly responding to the incentives the economy has thrown up, and how policy has tilted the playing field. This decade, some of those things were unavoidable (the earthquakes) but others were pure, deeply misguided, public policy choices. Rapid population growth generates lots of activity and demand for labour but – at least in New Zealand’s case – appears to have done nothing to improve the longer-term earnings capacity of the economy.

In the end, material living standards in any economy will largely reflect productivity growth. And yet, somewhat weirdly – but perhaps consistent with the increasing political cone of silence around that failure – as far as I could see not one of the SST articles yesterday even mentioned the productivity failure as the biggest obstacle to sustainably higher wages and material living standards. For now, we’ve been in a bit of a fool’s paradise – wages appear to have been growing faster than economic capacity. But unless something serious is done to reverse the productivity failure, it is hard to see that real wage inflation in the next decade will be able to be as high as it has been this decade. The bigger question right now shouldn’t be why wage inflation is so low, but why it is still so high.

(None of this is to rule out the possibility of some problems with the analytical unadjusted LCI data, but (a) SNZ has not pointed users to serious problems, and (b) the picture I’m painting doesn’t seem inconsistent with either the labour share of GDP data or the real exchange rate measures.)

If I understand it your dilemma is how wages have gone up but exports have not. Has it anything to do with the increase in tourism (how is tourism recorded in the stats) or a growing black market related to self-employment and increase in GST or working immigrants overstating their true income to obtain residency – a change in the nature of immigration?

LikeLike

Tourism export dollars are directly injected into domestic GDP, therefore the measure of Tourism Export GDP against total GDP is a redundant measure of performance where tourism is concerned.

LikeLike

No, that isn’t the puzzle at all. In fact, in many ways there isn’t a puzzle: given a huge shunt to demand (rapid population growth) and it is likely that wage-earners will do quite well. But that in turn undermines NZ firms’ competitiveness, and their ability to (or interest in) footing it globally, and the consequence is an economy more skewed towards producing for domestic needs (where international competition isn’t an issue) rather than tapping big competitive global markets (even if for niche products).

Re tourism, it is included in the export data (so the flat to falling export share is despite the rise in tourism in the last few years).

If there is a puzzle, it is probably one of why our political and official officeholders keep pursuing an economic strategy so manifestly (on the evidence of decades) unsuited to the NZ specifics, all egged on by too many local economists. Mostly it seems to be a triumph of ideology over experience – in some cases (but not most) with some direct financial interest thrown in. There isn’t much written about NZ, there isn’t much robust debate, so all too many people seem to take their steers from eg UK and US debates. They are quite different places/economies.

LikeLiked by 3 people

all egged on by too many local economists.

As a consumer of information (not understanding the detail, often), I look for vested interests and ideology.

LikeLike

From economists, I’d say the issue is mostly “ideology” broadly defined – combined with thinking more about generic advanced countries than about the specifics of NZ. Eric Cramptom is strongly pro-immigration in NZ, and as an immigrant non-citizen working for an organisation largely funded by big non-tradables firms you could construct a vested interest story. But I’m 100% sure it would be wrong: Eric would run the same arguments for Canada (home) if he still lived there, and works for NZI because they share his views, rather than attuning his views to the preferences of his funders.

LikeLike

I can’t for the life of me think of any reason why immigration should always be positive.There is no parallel in the natural sciences?

LikeLike

I have a question.

When say a person in china books a tour via a Chinese tour agent and pays a Chinese airline for their flight, pays Chinese owned hotels for the accommodation, Chinese owned tour buses and Chinese owned shops how do we know how much of that money actually arrives in our nations bank accounts?

This is not a question particularly aimed at the Chinese for it is the same equation for Japanese, Koreans and others before them.

Apart from having to pay local expenses and avoid paying high wages and payroll taxes the balance might never feature in our stats as far as I can tell.

AirNZ have the same deal Money they make outside of NZ isn’t necessarily accountted for here.

LikeLike

WeChat payments in NZ goes through a NZ based subsidiary and has to be banked in NZ.

LikeLike

Chinese owned hotels, tour buses and shops in NZ have to collect GST and pay to IRD.

LikeLike

Antony, I’m still bothered by tourism. How do we measure a tourist’s activity and assign it to exports? Take my holiday last year as an example: we spent on airfares and then at hotels, restaurants and car hire. All expenditure eventually can be tracked back to our NZ bank accounts – so our money was exported and another way of looking at it would be we imported various experiences from abroad. The NZ dept of stats could track our foreign exchange and deduce the value imported. However how does the NZ dept of stats track tourists – clearly airport charges are an export but how can they tell if a customer buying a burger is a tourist or a local? They can measure demand for NZ dollars but how do they know it is tourism?

If you increase tourism in NZ you increase demand for services but usually low wage services – hotel cleaners, restaurant staff, car hire, etc. OK the demand for these low wage shift workers will increase their wages but the median wage will end to decrease.

Does anyone have a link to an explanation as to how the export value of tourism is measured?

LikeLike

here is a link that will take you to some material on how tourism is measured (exports, and contribution to GDP)

https://tia.org.nz/resources-and-tools/insight/making-sense-of-the-numbers/

LikeLiked by 1 person

What’s the name of that Wechat subsidiary?, does it publish accounts?

LikeLike

Wechat appears to be a payment facilitator.

It’s not responsible for the payment of PAYE, GST, or income tax to IRD by the principal or the recipients of such payments

Recent examples in the Herald and Stuff demonstrate the amounts assessed by IRD against these operators usually disappears and they go bankrupt. NZ has great difficulty getting its hand on the green

LikeLike

WeChat is a payment facilitator but must operate separately in NZ as a NZ company with a NZ bank account. They have sole branding rights in NZ and in Australia to use the WeChat brand issued by WeChat China. In China it is a rather substantial company. I have met with the owners in NZ, they seem genuine with substantial monetary backing in setting up the IT infrastructure assisted by WeChat China.

NZ companies whether owned by Chinese operators or not, do have tax obligations. The IRD does pursue companies that do not meet their tax obligations quite vigorously. Therefore you cease to exist pretty quickly if you don’t pay your taxes.

Usually Chinese owners have bought existing local NZ companies and have more than overpaid the value of the businesses in their efforts to secure residency through the Entrepreneur plus immigration or investment category immigration.

LikeLike

I would guess that expectations have been rising faster than wages which is why nearly everyone seems to think they are ‘struggling’ – couldn’t have that extra overseas trip and save to buy a house, etc.

LikeLike

And the chart I meant to include in the post, but forgot to, was one making the point that wages have lagged far behind house prices – which has nothing to do with the labour market, and everything to do with the heavily regulated distorted urban land markets, which neither governing party has done anything to mix.

LikeLiked by 2 people

I nearly mentioned housing costs rising faster – the CPI is meant to include them of course but it doesn’t capture the component that is due to the massive increase in land prices!

LikeLike

Anthony, land prices were stripped out back in the 1990s when land price increases led to CPI around 19% in 1987 with the associated interest rates around 20%. Would you prefer interest rates at 20%?

LikeLike

Interest rates were that high because general inflation was fairly high and we were trying to get it down, not because of the specific way the CPI was constructed.

LikeLike

If you add back land prices then general inflation would definitely be in the double digits and also the associated interest rates hovering around land price increases rather than the 1.75% it currently is.

LikeLike

If land prices were included in the CPI then it would depend on their weighting on how much higher the CPI would be.

Brining the economy to a halt to try to stop rapidly rising land prices would have at least focused attention on the issue! Past governments may well have made some much needed reforms by now!

LikeLike

Bank Interest rates at 10% forced a economic recession in NZ in 2008 to 2010. House prices fell. There was a bloodbath in property. No one bought property when prices fell. The economy was in freefall. How did that fix anything other than the thousands of mum and dads and businesses that just went bankrupt?

LikeLiked by 1 person

“nothing to do with the labour market, and everything to do with the heavily regulated distorted urban land markets,”

doesn’t it equally have everything to do with immigration? Hugh Pavletich’s position is that after hurricane Katrina many people came to Houston but Houston managed, however Houston is on prairie, not an ismus with dairy land around.

Is there no political will to deal with land bankers?

LikeLike

I think you are greatly exaggerating Getgreatstuff. Of course some houses still sold and I certainly don’t recall any massive increase in bankrupticies. Householders should have been fine if they could continue to pay their mortgage even if they had no equity – and interest rates dropped when the recession hit, not rose!

I recall a lot of people being relieved that the property market took a breather. Unfortunately it also meant that John Key quietly shelved his promise to make much needed reforms to reduce house prices.

LikeLike

Anthony, you have a very short memory because 60plus financial instructions went bankrupt with the loss of $6 billion in mum and dad investments. I sat at the front row seat as house after house went into bankruptcy dealing with the separation of families. You may have missed the bankruptcy and mortgagee pages that had hundreds of mortgagee sales. Remember the NZ Apprentice where the star of the show Serepisos who owned $500million in property could not even give away his properties. No one wanted it.

LikeLike

Correction: Financial institutions.

LikeLike

More casual mis-information from GGS

According to wikipedia there were 67 Finance Company failures – between 2006 and 2012 – some occurring before the GFC. The net loss was $3 billion – with South Canterbury Finance accounting for 1 third of that

Having observed the passing parade that occurred the MAIN cause of the losses were due to the tired old action of borrowing short and lending long

That’s apart form the fraud of Petrecivich and Hotchin

LikeLike

Gone or frozen now is around $5 billion of investors’ money _ money belonging to people who perhaps sunk their life savings or retirement nest eggs into finance firms, or who took out second mortgages on their homes in the hope of making a little bit more than they would at the bank.

https://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=10527280

LikeLike

Companies’ registrar Neville Harris pulled no punches in his scathing report to the Parliamentary Commerce Committee on the incineration of the best part of $6 billion worth of more than 100,000 investors’ funds in New Zealand’s own home-grown finance sector crisis.

https://www.pundit.co.nz/content/finance-failures-%E2%80%93-our-6-billion-blame-game

LikeLike

Iconoclast, as you can see, $6 billion is not my comments but by specialists in the area. I can’t help it if parliament gets a white washed version of events to downplay the hurt and humiliation engineered by RBNZ trigger happy actions.

LikeLike

GGS: In the Herald Petricivich artlcle Mary Holm states – not that I consider her an authority

“They have broken the golden rule of (NOT?) lending money out long-term and borrowing short-term.”

Which particular authority and article states $6 billion?

LikeLike

Iconoclast, you really should read before commenting. I repeat the reference. There is another for $5 billion.

Companies’ registrar Neville Harris pulled no punches in his scathing report to the Parliamentary Commerce Committee on the incineration of the best part of $6 billion worth of more than 100,000 investors’ funds in New Zealand’s own home-grown finance sector crisis.

https://www.pundit.co.nz/content/finance-failures-%E2%80%93-our-6-billion-blame-game

LikeLike

I thought mass immigration was to counter all the leverage and debt in the system.

LikeLiked by 1 person

Net wealth in NZ has ballooned to $1.4 trillion. Debt growth has been rather muted compared to asset growth.

LikeLike

Housing was taken out of cpi in 1999. After the glass steigal act of 1935 was abolished. The economy only prosperes now if house prices inflate. There is no link also between economic growth and credit expansion based on interest rates. Prof Richard Werner has proved this. The only way credit gets into the system is asset backed credit creation by banks to which they can manipulate there capital ratios.

LikeLike

You will have noticed the “head biscuits” either change the formula or change the name if its not working for them

Example Oranga Tamariki, Census “what census”, change immigration formula, remove housing from CPI

LikeLike