Arguments have run around for years about New Zealand’s relatively low national savings rate, Australia’s relatively high national savings rate, and the Australian compulsory private savings system.

Doesn’t NZS just contribute to New Zealand’s “savings problem” and haven’t the Australians shown the way to boost national savings?

A universal age pension will have reduced private savings, relative to a benchmark system in which there was no state age pension at all. But it won’t have done so for everyone. Many people never earn enough to have saved any material amount for retirement. For them, the absence of something like NZS would simply mean they went on working until they no longer physically could, and would then rely on family and private charity. GDP might be higher, but savings rates probably wouldn’t be materially different. And at the other extreme, it seems unlikely that Graeme Hart or others on the “rich list” will save one cent less because they too may receive a modest universal pension payment at 65.

But it makes a difference for people in the middle. The knowledge that, in retirement, the state will provide an annual income of around $25000 per couple makes a huge difference to how much a family earning $100000 might need to save to support their desired consumption in retirement. Whether it lowers national savings isn’t possible to tell a priori – that depends on what the government does. If we had no NZS, would government savings – and accumulated government debt – be higher, lower or no different?

But the choice isn’t universal NZS or no age support at all. Some argue for means-testing for NZS, as was done from the mid 80s until the late 1990s. There could be some real fiscal savings to be made from no longer paying NZS to upper income or wealthier people. But to get material savings the system has to start abating NZS payments at relatively modest levels of other income/assets, and the people who are likely to be affected will alter their behaviour accordingly. A lot of fiscal savings can be made, but only with the probability of further discouraging many middle income people from saving for their own retirement. Again, it won’t make a difference to anyone with really high wealth/income, but for someone who was planning to provide themselves with, say, $30000 per annum on top of NZS it could make a real difference – both to planned savings, and to a willingness to stay in the workforce beyond 65.

I also asserted yesterday that our NZS system probably discouraged private savings less severely than systems in many other OECD countries. In many countries, people receive state pensions that are calculated based on the earnings of the individual concerned (sometimes lifetime average earnings, sometimes only the later years’ earnings). A person with average lifetime earnings of say $80000 will get a state pension materially higher than someone whose lifetime earnings averaged $40000. In New Zealand, no matter how much you’ve earned over your life, the state pension is still only around $25000 per couple. Fair or not, the point here is just that in New Zealand if you want more than the basic $25000 you have to provide it for yourself. In many other systems, the state provides it, but the state has not funded that cost as the prospective liability has accumulated. So our system probably deters private savings – among those with the capacity to save materially – less than many of the schemes in other countries do.

Ah, but what about compulsory private schemes? Australia is one of the few that has been in place for quite a long time. And, of course, it is a scheme directly relevant to many New Zealanders, given the extensive New Zealand migration to and from Australia.

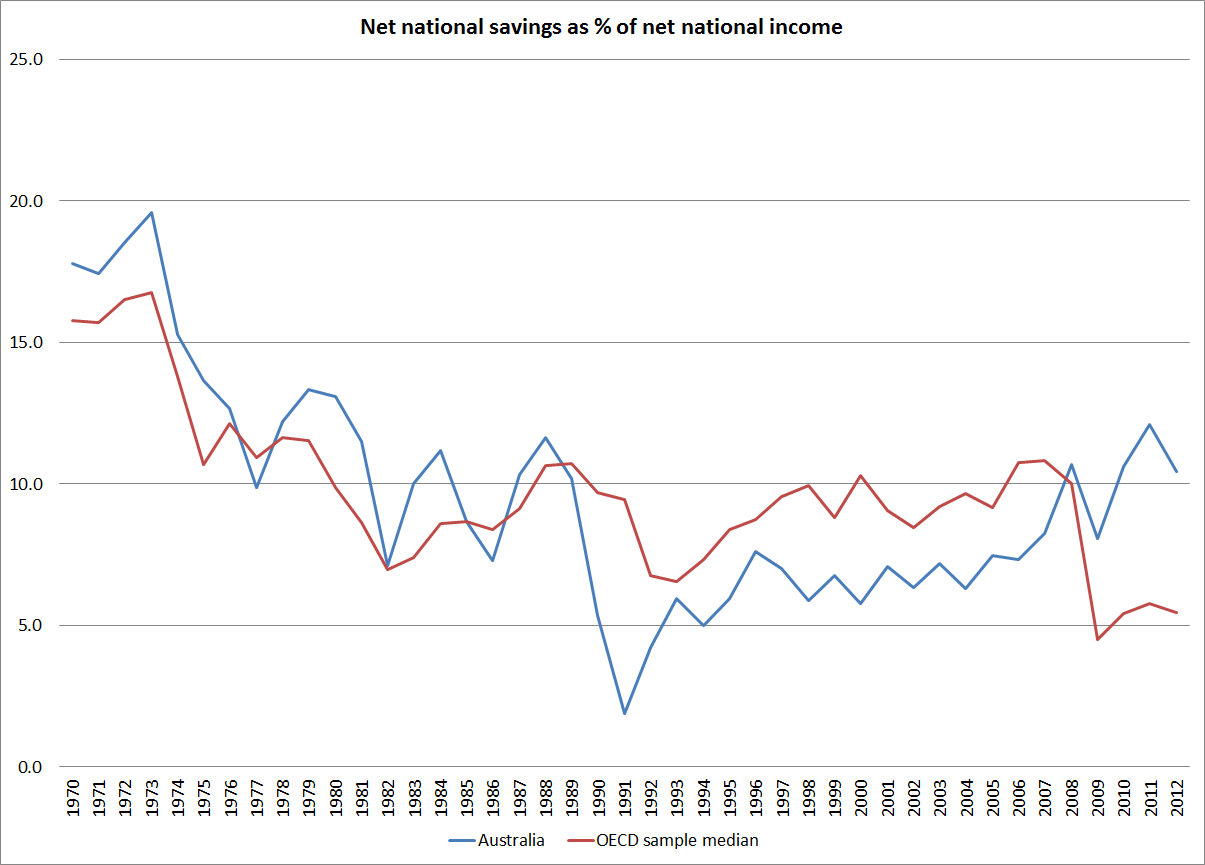

The national savings rate in Australia is relatively high – something that tantalises many in the New Zealand debate. Often the gross national savings rate as a percentage of GDP is quoted. But I don’t think it is the best measure of savings. In the rest of this piece, I will be using net national savings as a percentage of net national income. “Net” here means net of depreciation. Australia has some very capital-intensive production structures, and a high proportion of its gross income needs to be applied to cover depreciation on the capital. And “national” here means the incomes, and savings, of – in this case – Australians.

The OECD has a pretty good collection of data on these two series for around 20 member countries going back to 1970. Australia had pretty high net national savings rates right back at the start of the period, a few percentage points above the median of this sample of OECD economies. Quite why, I’m not sure, and I haven’t seen any good studies looking at that particular cross-country comparison. But what I wanted to focus on is what has happened over the period since 1970, in Australia and in other advanced economies.

Australia’s net national savings rate was at or above the level of these other countries until around 1990. But for the following 15 years, Australia’s savings rate was well below those in the other advanced economies, and lower than it had been in the 1980s. It is only with the huge terms of trade boom from the middle of the 2000s that Australia’s national savings rate surges up again. As the terms of trade falls away forecasts suggests the national savings rate will drop too.

How does compulsory private savings fit in this picture. David Gruen, former Deputy Secretary of the Australian Treasury, gives us the summary history:

The compulsory superannuation system began with industrial award-based superannuation, agreed by the Government of the day and the Australian Council of Trade Unions as part of the 1985 Prices and Incomes Accord. A 3 per cent superannuation contribution was paid by employers into employees’ individual accounts in nominated superannuation funds, rather than being paid as a wage rise.5

The coverage of award superannuation was expanded significantly in 1992, with the introduction of the Superannuation Guarantee Levy, which required employers to make superannuation contributions on behalf of their employees, and enshrined superannuation contributions in federal legislation rather than relying on the award system.

The then Government announced plans to gradually increase the minimum contribution rate to 9 per cent by 2000-01

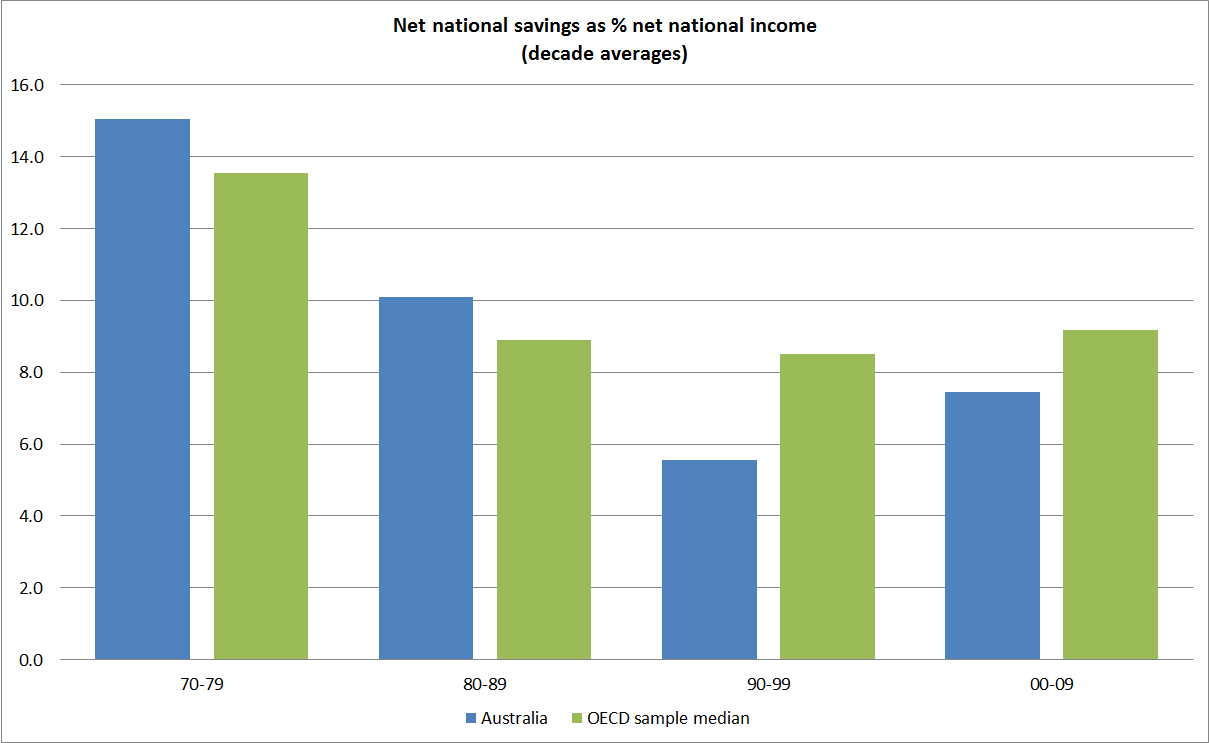

So from the mid-1980s, and particularly from 1992, Australian employees were compelled to progressively increase the proportion of their incomes put away in designated superannuation savings vehicles. And yet, at an aggregate national accounts level there is little sign of it. Not only is Australia’s national savings rate in the 1990s lower than it was in the 1980s, but it was lower relative to those in other advanced economies.

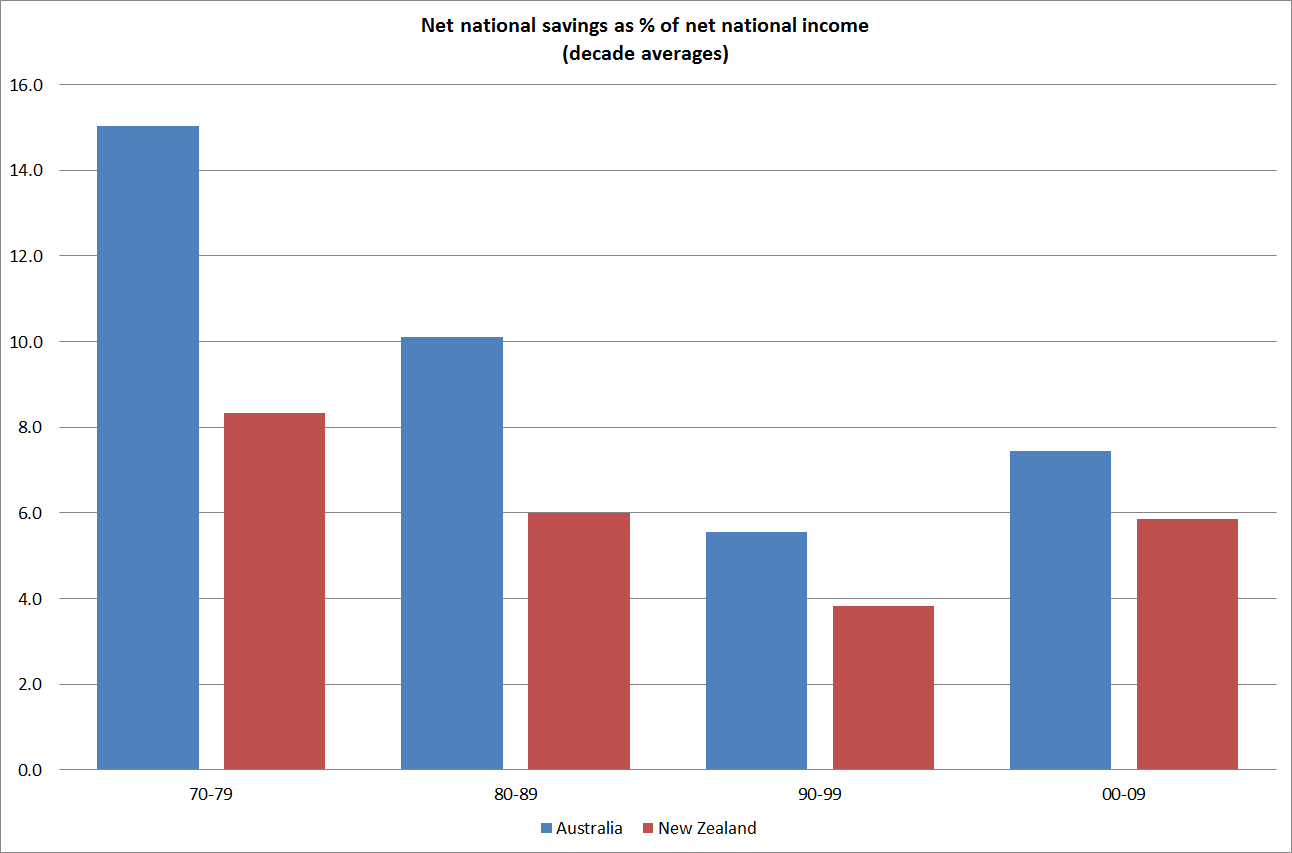

And what about the comparison with New Zealand? Again, Australia has had a higher net national savings rate than New Zealand throughout, but the gap has been smaller in the last couple of decades than it was in the first two decades. And in this comparison, it is worth bearing in mind that in the 70s and 80s, New Zealand had in place very concessional tax treatment for private superannuation vehicles, which might (if anything) have tended to boost savings rates here.

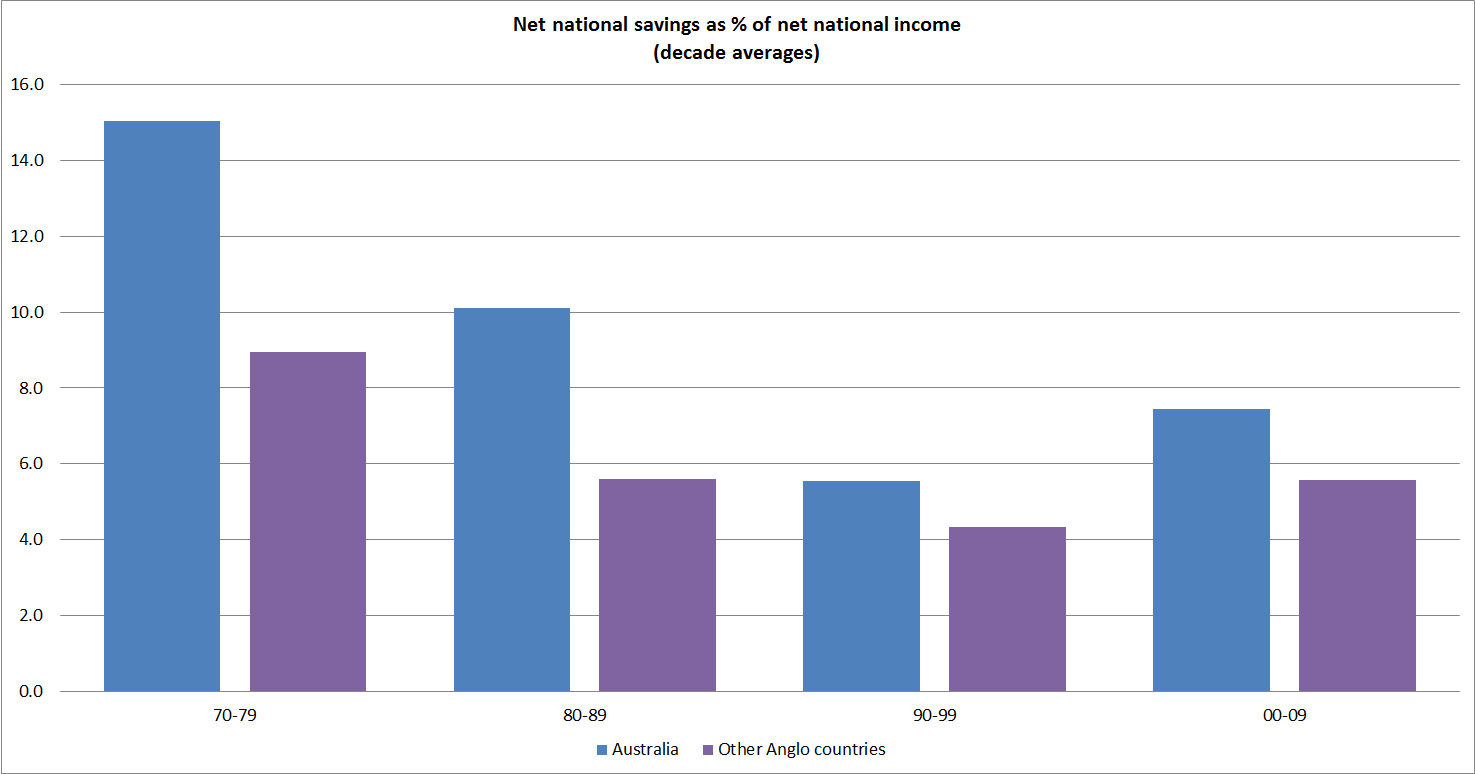

The picture doesn’t look much different if we compare Australia with the median of the other Anglo countries (Canada, Ireland, New Zealand, the US and the UK).

Several empirical studies have suggested that the compulsory savings scheme has boosted savings rates in Australia. The reported evidence has been stronger in respect of household savings than for national savings, although David Gruen (who cites these studies) is confident that the arrangements have boosted Australia’s national savings rate.

Perhaps. And. as ever, we can’t know the counterfactual. But it isn’t obvious at a macroeconomic level. There might be small positive effects that just can’t be seen at this level of aggregation – other forces would have driven national savings rates in Australia even lower, and compulsory private savings prevented those full effects being seen in the data. But it is difficult to know quite what those effects would have been, and why for example they might have affected Australia more severely than New Zealand and other advanced economies. At very least, it is hard to see that the really far-reaching changes Paul Keating established, and subsequent governments have persisted with, has been any sort of game-changer as far as Australia’s national savings is concerned[1]. And, as I noted yesterday, it is not as if the Australian arrangements have ended up fiscally cheaper than New Zealand’s either.

[1] And that is without even mentioning the distortions to private choices and balance sheets, the “subsidies” to funds managers and tax accountants, and so on. The scheme will have changed many individual balance sheets, and has probably left the household sector more leveraged than otherwise, and perhaps the Australian gross international investment position too.

I agree with the empirical studies. There is somewhat in excess of two trillion dollars there to prove it, and that sum of money is invested in stocks and bonds in a pretty professional way (i.e. in something approximating a value-based approach to investing). My own superannuation is managed by a very large, non-profit that offers excellent value for money. Overall the system works and has been beneficial to corporate Australia. There are problems with over-intermediation, it’s true, particularly around financial advisers and their “wrap” platforms, but these are being fixed (very slowly). This contrasts favourably with New Zealand where people, as a practical matter, accumulate wealth through property first and there is no real domestic funds management industry.

More generally, when I look at smallish countries which seem to do a good job of funding their investment needs – I’m thinking of Switzerland, Korea, Singapore, Taiwan, Hong Kong, Ireland, Chile – they typically have a mandatory Tier 1 component of at least 8%, with provision for more saving for top-up or other purposes. New Zealand looks like the outlier in this regard. We could do worse than copy the Australian scheme, while making a few improvements, in my view.

LikeLike

Blair

Always welcome the comments.

Just bear in mind that Australia was a relatively high savings country before the compulsory scheme was ever put in place.

I have a lot of time for David Gruen, but if the scheme had made that much difference we should see it somewhere in the macro aggregates,

Re property, someone has to own it, and NZ has no more housing per capita, no more absurdly priced, than Australia – indeed, since we are a poorer country we have a bit less house (square metres) per capita.

Michael

LikeLike

It’s true that the implementation of compulsory super didn’t show up in the gross saving aggregates. So my argument to some extent involves also believing that the savings rate would have fallen (more) without the Keating reforms. It’s probably not possible to “prove” this statistically, since so many things changed over that period; however I suspect that many who lived through the last couple of decades are of the same view.

LikeLike

Michael, since I and my wife are both over 65 and in receipt of National Superannuation, I feel I owe it to you to report that the after tax sum we will receive in the year to 31 March 2016 is $48 short of $30,000, somewhat more than your $25k.

LikeLike

all that wage inflation must have been passing me by!

LikeLike