There wasn’t going to be a post today but then someone sent me the link to a super-soft interview the Herald’s Liam Dann had done with Reserve Bank Governor Adrian Orr. Had the Bank’s own PR consultants been scripting the interview it would scarcely have been softer (in fact, they might have advised a couple of serious questions to give the resulting interview a bit of credibility).

Orr will by next week have been in office for 11 months, wielding vast amounts of policymaking power singlehandedly, and yet we’ve still not had a single speech on either of his main areas of responsibility; monetary policy, and the regulation of much of the financial system. But there is still time to play the tree god line (that’s the Herald headline: “Orr embraces the forest god”).

I’ve written about this silliness before. Extracts

The latest example was the release on Monday of a rather curious 36 page document called The Journey of Te Putea Matua: our Tane Mahuta. Te Putea Matua is the Maori name the Reserve Bank of New Zealand has taken upon itself (such being the way these days with public sector agencies). It isn’t clear who “our” is in this context, although it seems the Governor – himself with no apparent Maori ancestry – wants us New Zealanders to identify with some Maori tree god that – data suggest – no one believes in, and to think of the Reserve Bank as akin to a localised tree god. Frankly, it seems weird. These days, most New Zealanders don’t claim allegiance to any deity, but of those of us who do most – Christian, Muslim, or Jewish, of European, Maori or any other ancestry – choose to worship a God with rather more all-encompassing claims.

But the Governor seems dead keen on championing Maori belief systems from centuries past. In an official document of our central bank we read

A core pillar of the evolving Māori belief system is a tale of the earth mother (Papatūānuku) and the sky father (Ranginui) who needed separating to allow the

sun to shine in. Tāne Mahuta – the god of the forest and birds – managed this task after some false starts and help from his family. The sunlight allowed life to flourish in Tāne Mahuta’s garden.

This quote appears twice in the document.

All very interesting perhaps in some cultural studies course, but what does it have to do with macroeconomic management or financial stability? Well, according to the Governor (in a radio interview on this yesterday) before there was a Reserve Bank “darkness was on our economy”. The Reserve Bank was the god of the forest, and let the sun shine in. Perhaps it is just my own culture, but the imagery that sprang to mind was that of people who walked in darkness having seen a great light. But imagine the uproar if a Governor had been using Judeo-Christian imagery in an official publication.

On the same page we read

Many of these birds feature on the NZ dollar money including the kereru, kaka, and kiwi – core to our belief system and survival.

I’m a bit lost again as to who “our” is here. I’m pretty sure I’m like most New Zealanders; I never saw a bird as “core” to my “belief system”. Perhaps the Governor does, although if so we might worry about the quality of his judgements in other areas.

As I say, it is an odd document. There are pages and pages that have nothing whatever to do with monetary policy or the financial system. Some of it is even quite interesting, but why are we spending scarce taxpayers’ money recounting stories of New Zealand general history? …. There is questionable history,….highly questionable and tendentious economic history, and overall a tone (perhaps comforting to today’s liberal political elite) that seems embarrassed by the European settlement of New Zealand. There is lots on the difficulties and injustices that some Maori faced, and little or nothing on the advantages that western institutions and society brought. Reasonable people might debate that balance, but it isn’t clear what the central bank – paid to do monetary policy and financial stability – is doing weighing in on the matter.

As I noted earlier, in a radio interview yesterday the Governor claimed that prior to the creation of the Reserve Bank ‘darkness was on our economy’, that the Reserve Bank had let the sunshine in, and that Australia and the UK had somehow turned their backs on us at the point the Bank was created. In fact, here it is – Reserve Bank as tree god – in the document itself.

The Reserve Bank became the Tāne Mahuta of New Zealand’s financial system, allowing the sun to shine in on the economy.

I think there was a plausible case for the creation of a central bank here, but to listen to or read the Governor you’d have no idea that New Zealand without a Reserve Bank had been among the handful of most prosperous countries in the world. Here from the publication, writing about the period before the Reserve Bank was created

The infrastructure funding was further hindered by the banks being foreign-owned (British and Australian) and issuing private currency. Credit growth in New Zealand was driven by the economic performance of these foreign economies, unrelated

to the demands of New Zealand. Subsequent recessions in Britain and Australia slowed lending in New Zealand when it was most needed.

Very little of this stands much scrutiny. You’d have no idea from reading that material that the New Zealand government had made heavy and persistent use of international capital markets, such that by 1929 it – like its Australian peers – had among the very highest public debt to GDP ratios (and NIIP ratios) ever recorded in an advanced country. You’d have no idea that New Zealand was among the most prosperous countries around (like Australia and the United States, neither of which had had central banks in the decades prior to World War One). You’d have no idea that the economic fortunes of New Zealand, trading heavily with the UK, might reasonably be expected to be affected by the economic fortunes of the UK – terms of trade and all that. Or that economic cycles in New Zealand and Australia were naturally quite highly correlated (common shocks and all that). And of course – with all the Governor’s talk about how we could “print our own money” – within five years of the creation of the Reserve Bank, itself after recovery from the Great Depression was well underway, that we’d not unrelatedly run into a foreign exchange crisis that led to the imposition of highly inefficient controls that plagued us (administered by the evil twin of the tree god?) for decades. Or even that persistent inflation dates from the creation of the Reserve Bank

One can’t cover everything in a glossy pamphlet, even one that seems to purport to be aimed at adults (including Reserve Bank staff according to the Governor), but there isn’t much excuse for this sort of misleading and one-dimensional argumentation, aka propaganda.

The propaganda face of the document becomes clearer in the second half. Among the issues the government’s review of the Reserve Bank Act is looking at is whether the prudential and regulatory functions of the Bank should be split out into a new standalone agency, a New Zealand Prudential Regulatory Authority. …. There are arguments to be made on both sides of the issue, but you wouldn’t know it from reading about the Governor’s vision of the Bank as a Maori tree god, where one and indivisible seems to be the watchword. Everything is about “synergies”, and nothing about weaknesses or risks, nothing about how other countries do things, nothing about the full range of criteria one might want to consider in devising, and holding to account, regulatory institutions for New Zealand.

I don’t have any problem with officials, including from affected agencies, offering careful balanced and rigorous advice on the pros and cons of structural separation. But that is a choice ultimately for ministers and for Parliament. And among the relevant considerations are issues of accountability and governance. Neither word appears in Governor’s propaganda piece. But then tree gods probably aren’t known for accountability. New Zealand government regulatory institutions should be. If ministers and Parliament decide to opt for structural separation, I wonder how the Governor will revise his document – his tree god having been split in two.

Among the tree god’s claims about financial regulation and what the Bank brings to bear was this breathtaking assertion, prominently displayed at the head of a page (p27).

The Reserve Bank is highly incentivised to ‘get it right’ when it comes to prudential regulation. We have a lot at risk

It is an extraordinary claim, that could be made only be someone wilfully blind – or choosing to ignore – decades of serious analysis of government failure, and the institutional incentives that face regulators, regulatory agencies, and their masters.

There is nothing on the rest of that page to back the tree god’s claim. On any reasonable and hardheaded analysis, the Reserve Bank has very weak incentives to “get it right”, or even to know – and be able to tell us – what “get it right” might mean. When banks fail, neither the Reserve Bank Governor nor any of the tree god’s staff have any money at stake (at least in their professional capacity, and as I recall things, Reserve Bank staff – rightly – aren’t allowed to own shares in banks). It is all but impossible to get rid of a Reserve Bank Governor, and it is even harder to get rid of staff (for bad policy or bad supervision). Most senior figures in central bank and regulatory agencies of countries that ran into financial crises 10 years ago, stayed on or in time moved on to comfortable, honoured (a peerage in Mervyn King’s case) retirements, or better-remunerated positions in the private sector.

And when the Reserve Bank uses its powers in ways that reduce the efficiency of the financial system, or stopping willing borrowers and willing lenders writing mortgage contracts, where are incentives on the Reserve Bank to “get things right”. There are no personal consequences – the Governor and his senior staff either won’t have, or would have no problem getting, mortgages. The previous Governor got to exercise the bee in his bonnet about housing crises, and to play politics, with no supporting analysis and no effective accountability. The current head of the tree god opines that lenders and borrowers can’t be trusted – but tree gods apparently can – but when challenged produced no analysis to support his claim. That sort of system creates incentives for sure, but they aren’t to “get it right”.

End of extracts. 2019 here again.

The Governor was at it again in the interview, including running his bizarre version of economic history in which “sunshine” was let in upon the New Zealand economy in 1934 (there was also the surprising claim that the banks had chosen to graft themselves into the Reserve Bank, apparently oblivious to the fact that the main banks have been around New Zealand a lot longer than the Reserve Bank).

The Governor claims his metaphor is wildly popular – except among “two bloggers” apparently (although I could give him a rather longer list of sceptics) – and I’m sure it is in some quarters. It probably sounds cool, accessible, relevant and so on. But metaphors can be used for good and for ill, and the Governor attempting to have us all think of the Bank as akin to a tree god doesn’t serve the public interest well at all, even if it happens to suit his personal campaigns.

There were plenty more questionable claims made by the Governor is the course of the interview. Some of them literally invite questions – they might be true, or they might not, we just don’t know. For example, the Governor claims that his proposed new capital requirements will be “in the pack” by international standards, but they’ve not yet shown any evidence to support this claim (especially once one takes account of their irrational distaste for cheaper Tier 2 capital, and for the high minimum overall risk weights they are planning to impose). It should be a simple matter to put the evidence and analysis out there for scrutiny, but instead apparently we are simply supposed to trust this apostle of the tree god.

Then there was the claim – made in the consulative document but not supported with one shred of serious analysis or evidence – that the Bank’s proposed capital requirements will make the economy not only safer but also more efficient. I’ve shown this chart previously

In today’s interview he explicitly asserted that New Zealand – and all other advanced economies – are to the “south-west” of that green dot. Perhaps he’s right, but you’d think there would be some support offered for these “free lunch” claims. It isn’t in the consultative document, it wasn’t in the Governor’s interview. Perhaps (at last) it will be in the Deputy Governor’s speech next week?

The interview ended with a super-soft invitation to the Governor to campaign for more taxpayer’s money, more staff, and more financial resources. Perhaps there is a case for more (actually I suspect there is). But the idea that we should put more of our scarce money in his hands isn’t as persuasive as it should be when we get repeated doses of this tree god silliness, attempts at playing politics, repeated bold claims that just aren’t supported (complete with assertions that people who disagree him haven’t read his documents – the problem is, they have), diversions onto all manner of things that just aren’t his responsibility, and a lack of serious – as opposed to superficial – transparency and accountability.

UPDATE: The interview and accompanying article might have been incredibly soft, but in many respects the sub-editors of the hard-copy Herald say it all with their headline on the front page of Saturday’s business section: “How Maori myth is guiding the Reserve Bank”. Were it so – and even I don’t think it really is – it would explain a lot about the policy and comms mis-steps……

And as a commenter overnight observed

It shows how bad things have gotten in New Zealand – not so much that he makes these examples but because no one else even thinks to challenge it. Imagine the reaction if the Bundesbank president started discussing policy in terms of Odin and Thor…. he’d get locked up…

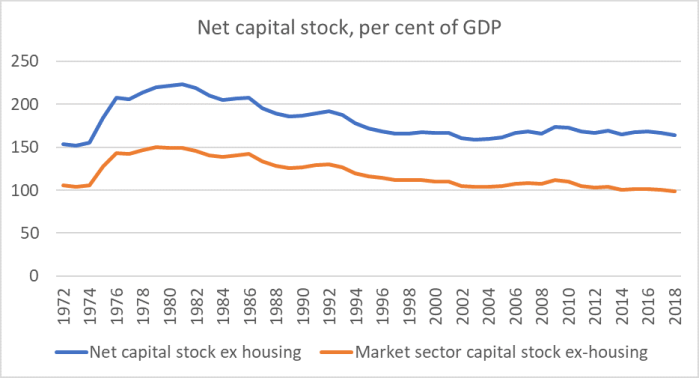

(I don’t know what accounts for the sharp lift back in mid-70s, but you can see the Think Big effect in the early 80s.)

(I don’t know what accounts for the sharp lift back in mid-70s, but you can see the Think Big effect in the early 80s.)