The Minister of Finance and the Governor of the Reserve Bank today released the Remit and Charter for the new statutory Monetary Policy Committee, that takes effect from 1 April. The Remit largely replaces the Policy Targets Agreement structure in place since 1990, and future remits will be set directly by the Minister of Finance, after advice from the Reserve Bank (among others) and associated public consultation. The Charter is mostly new, governing how the MPC is supposed to operate in some key, outward-facing, dimensions. It complements various detailed statutory provisions. Even though both documents are this time agreed between the Governor and the Minister, it is clear that the Minister has taken the lead: the press release is issued by the Minister alone, and although it is now reproduced on the Bank’s website, contains various bits of political spin.

The contents of the new Remit are in many respects pretty similar in substance to the current PTA, but there are a couple of changes worth noting.

One looks like an error. In the Context section the Remit states that

“(the Act) requires that monetary policy promote the prosperity and wellbeing of New Zealanders”

That line took me by surprise so I went back and checked the new legislation. The relevant provision actually states

The purpose of this Act is to promote the prosperity and well-being of New Zealanders,

Those are two different things. The Remit – which the Governor has voluntarily signed on to – can reasonably be read as suggesting that monetary policy should be conducted with “wellbeing” in mind. The Act sets out statutory objectives for monetary policy (the things the MPC is supposed to pursue and take into account), simply stating that Parliament has put the legislation in place believing that the monetary policy goals (and other powers the Bank has, including regulation and supervision) will conduce to the wellbeing of New Zealanders. The Remit shouldn’t have been worded that way.

My second observation about the Remit is more positive (and would be more positive still if the document hadn’t been released in a format in which one can’t copy and paste extracts). It is stated that “monetary policy contributes to public welfare by reducing cyclical variations in employment and economic activity whilst maintaining price stability over the medium-term”. I like that formulation, which is much closer to what I recommended should be the statutory goal for monetary policy. Price stability is the constraint, economic stabilisation is the primary purpose. Whether or not the wording is quite consistent with the actual new legislative goal is something for the MPC, and those paid to hold them to account, to work out.

What of the Charter?

My overarching unease about the MPC is that it will be dominated the Governor. That is partly through the channel of the inbuilt management majority (and the Governor hires the other managers), and partly because of the heavy say the Governor will have in who gets appointed to the (minority) external positions.

But it is reinforced by the relentless, and explicit, drive for “consensus”. This is from the Charter

“Consensus” isn’t a recipe for getting the best answers, but for lowest common denominator answers that everyone can live with. It isn’t really a recipe for a robust examination of competing arguments and analyses either – at least unless one has exceptional people (which is always unlikely, almost by definition) – and especially when management has (a) an inbuilt majority, and (b) control of all the research and analysis resources (and of the pen in drafting MPSs etc). The risk remain that outsiders, knowing they are inevitably outnumbered, and having ‘consensus’ waved in their faces will simply go along, free-riding.

The formal transparency model chosen is likely, at the margin, to reinforce this risk. We are told that the record of the meeting will be published at the same time as the OCR announcement (2pm on Wednesday, following an MPC meeting that morning). Even allowing for various preliminay meetings, the “record” of the meeting will inevitably be heavily pre-drafted by staff who work to the Governor, and the ability of outside MPC members to get any alternative perspectives included is going to be an uphill struggle. Most central bank MPCs release minutes with something of a lag. All that said, time will tell how it works out.

One interesting provision in the Charter was this

It was interesting for two reasons. First, this provision appears to accept that significant operational decisions around monetary policy are the responsibility of the MPC. That was not (is not, in my view) clear from the legislation. If so, it is welcome, especially if it involves an expectation by the Minister that, for example, any future quantitative easing and similar decisions would also be a matter for MPC. We’ll have to see.

Presumably this provision is supposed to cover the longstanding arrangements for possible foreign exchange intervention. When I was at the Bank, the OCR Advisory Group (internal forerunner to the MPC) was the forum in which the Governor made in principle decisions on intervention, and specific timing choices etc were then dealt directly between the Governor and the Financial Markets Department.

If so, the specific provisions go much too far. Perhaps there is a case at times for not announcing foreign exchange intervention immediately in some circumstances. But there are no grounds for leaving the MPC to decide for itself when, if ever, specific information on intervention will be released (the implied movements in the Bank’s fx position come out more than a month later, and even then without comment of explanation). At present, there probably is not much practical importance attaching to this point, but the system should be started as we mean to go on. Much better to have insisted that all market intervention (size and nature, although not counterparties) should be disclosed within 10 days of such intervention. Apart from anything else, these are big financial risks the taxpayer is (given no choice in) assuming.

My final observation on the charter offers kudos to the Minister. There has been a great deal of talk about the need to seek consensus (which is still in the charter) and the claim had been made that this meant all MPC members should speak, if at all, with a single voice. Bank management championed this (self-interestedly no doubt), despite the successful examples of countries like the UK, the US, and Sweden, and a year ago it seemed that they had persuaded the Minister of their view. It was one reason why good people would probably have been deterred from applying for the external positions – facing a built-in internal majority, and with no ability to articulate in public alternative perspectives, it wasn’t obvious that the positions offered more than sightseeing (looking at the innards of how the Bank works). I’ve banged on about the issue for months, and I know others have also raised concerns.

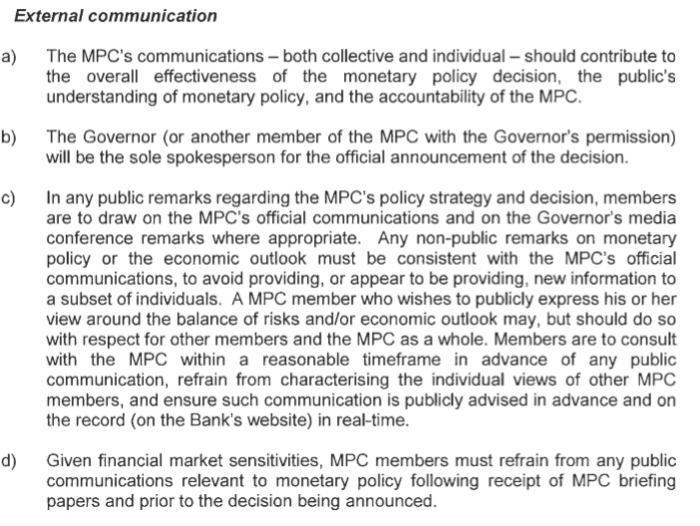

And so imagine the pleasant surprise I got when I got towards the end of the charter.

I don’t have any particular problems with (a) or (b), although I can imagine some future disputes about what does and doesn’t contribute to the “overall effectiveness” of the monetary policy decision etc, since things that might muddy the water a bit in the short-term could easily strengthen the institution, and its accountability, in the medium term. I also had no problem with (d) which is pretty much how Reserve Bank staff have operated for many years.

What caught my eye was (c), under which it appears that members of the MPC – internal and external – will be free to comment in public, expressing their own views on the economic situation, risks, and monetary policy. On monetary policy itself, they are required to draw on official communications “as appropriate” – and I’m sure they will, as appropriate. But it doesn’t bind MPC members to agree with committee decision, or to endorse all the arguments the Governor himself might offer in support of the decision. On the economy etc, they can say what they like (in substance) provided they do so politely (as people typically do in transparent foreign central banks) and let their colleagues know in advance what they’ll be saying. It is a material step forward relative to what we’ve been promised (although time will tell whether anyone, internal or external (and thus vetted for tameness by the Governor) ever utilises these provisions).

What is also interesting is some of the detail. There is now an explicit written requirement that any off-the-record private remarks about monetary policy or the economic outlook have to be consistent with official MPC communications. Presumably this also applies to the Governor (there is no suggestion it doesn’t) so if there are off-the-record expletive-laden rants at private commercial functions in future, at least they won’t be offering any insights on the economy and monetary policy. Perhaps that Rotary Club advertising the Governor as offering candid perspectives on the New Zealand economy – if you pay – will have to revise its plans? More probably, the Governor probably won’t regard himself as bound by the rules.

And then there was the final sentence. Any on-the-record remarks (occasions at which they will be made) will have to (a) notified to the public in advance, and (b) with full text on the Bank’s website in real-time. In principle, this looks fine and sensible (although it is far from what has been practised by management up til now). In practice, it will prevent MPC members giving interviews, and appears designed to ensure that the only communications are speeeches with written texts to which MPC members adhere closely. But, again, there is no suggestion that these rules don’t apply to the Governor – and his views are inevitably most market-moving. So can we look forward to an end to off-the-record speeches from the Governor on matters of substance, and to wild departures from the prepared and published text. After all, as the document says, MPC members shouldn’t provide, or look as though they are providing, new information to private subsets of people. (Personally, I suspect the document goes a little too far. It would probably be unfortunate if, say, the Governor cannot (as the document appears to suggest) give an interview to, say, Morning Report or one of the main current affairs programmes, so long as there is adequate public notification as to when and where he will be speaking.)

As I’ve said on various previous occasions, I’m pretty ambivalent about the monetary policy legislative amendments, and particularly about the MPC, which looks set to be a Governor-dominated creature, not too different in effect from what we’ve had for the last 29 years. But credit where it is due. There are some welcome aspects in the details of today’s announcement and I, quite honestly, hope the new system works better than I expect it to. Who knows, the less closed nature of the rule may even help attract a better class of candidate to consider the MPC position.

For now, of course, we are still left guessing who four of the seven MPC members will be.

It is a free lunch they are claiming to offer. I suspect few will be convinced.

It is a free lunch they are claiming to offer. I suspect few will be convinced.