(For anyone who followed a link looking for my post on the National Party and the PRC, it is here)

A few days ago one of my posts included the chart showing that there has been very little labour productivity growth in New Zealand for most of this decade. A commenter asked

A question for you on the productivity flat line. Is it reflective of levels of investment? How does the productive capital stock per worker look over the last decade?

And so today I’ll try to step through some of the data that sheds a bit of light on that question. As background, it is worth bearing in mind that for decades New Zealand business investment as a share of GDP has been relatively low by OECD country standards, especially once one takes account of our relatively fast population growth rate. The biggest exception was that outbreak of government-inspired wastefulness, Think Big, in early-mid 1980s. Not all investment captured in the national accounts statistics is “a good thing”.

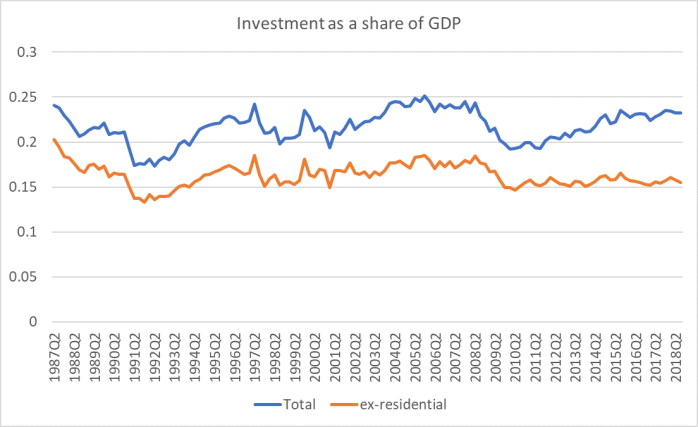

First, some flow data. Here is investment as a share of GDP (using quarterly seasonally adjusted data).

Lots of houses repaired (Canterbury) and built (nationwide) but once you set residential investment spending to one side. the remaining investment as a share of GDP has been very subdued indeed, not really much higher than during the recession at the end of last decade.

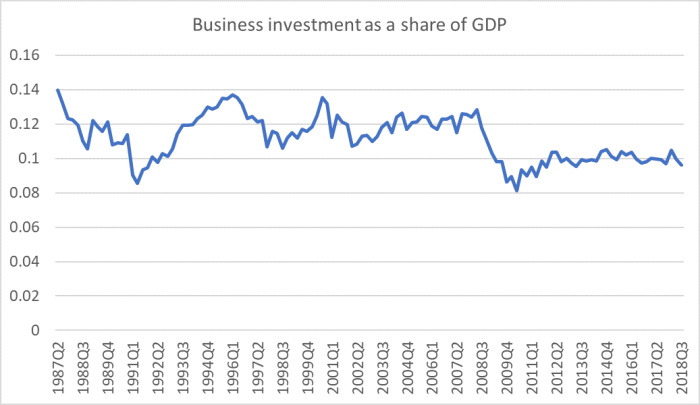

There isn’t an official published series of business investment, so I use the same proxy the OECD does: start from total investment and subtract residential investment and government investment spending. There is a small overlap there (some government residential investment spending), but with that caveat noted here is the proxy for business investment as a share of GDP.

The only times this business investment proxy was lower than at present was in the depths of the two serious recessions (1991 and 2000-10). And yet over recent years, our population was growing consistently faster than at any time in recent decades. Businesses tend to invest when there are prospective profitable opportunities – especially when financing conditions aren’t unduly constraining. Presumably, those opportunities just haven’t been there in New Zealand in recent years.

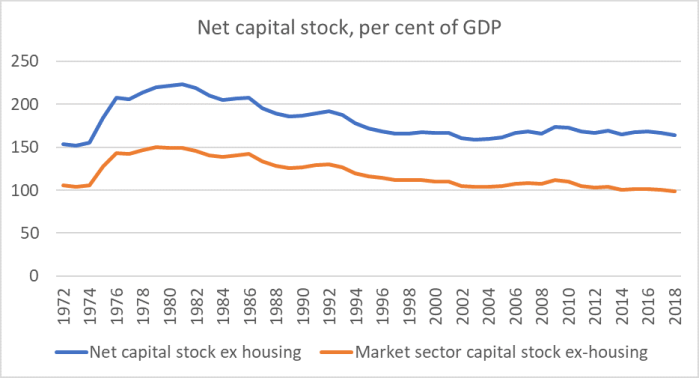

My commenter’s question was about capital stocks. Statistics New Zealand publishes net (of depreciation) capital stock data. The upside is that there is a good long time series, but the downside is that it is annual data so that the most recent observation is for the March 2018 year.

Here are a couple of stock series, expressed as percentages of nominal GDP.

(I don’t know what accounts for the sharp lift back in mid-70s, but you can see the Think Big effect in the early 80s.)

(I don’t know what accounts for the sharp lift back in mid-70s, but you can see the Think Big effect in the early 80s.)

Those were nominal (current price) series. If we want to look at the capital stock relative to real variables (eg hours worked) we need to use the constant price data instead. Here is the real capital stock, ex housing, per hour worked.

I’m not quite sure what to make of the entire chart – I’m a little surprised there wasn’t more growth in the 1990s – but for the more recent period it is certainly consistent with the (very weak) productivity picture.

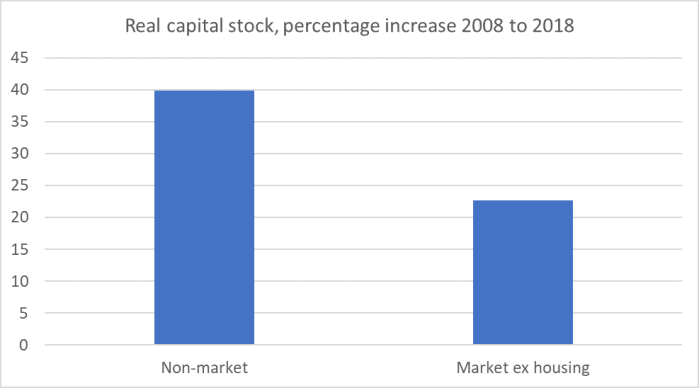

Perhaps as sobering is this simple chart, showing the percentage increase in the real capital stock from the year to March 2008 to the year to March 2018.

Pretty significant growth in the non-market component (the bits not subject to market tests, either at the evaluation stage or in operation, and basicially set by government – central or local) relative to the growth in the market sector non-housing capital stock. Firms operating in more-or-less competitive markets just don’t seem to have seen the remunerative projects to invest in. That isn’t in any fundamental sense the “cause” of our really weak productivity growth, but it will be a reflection of the same factors.

On my telling, the persistently high real exchange rate is, in turn, a significant proximate part of that story.

Tempted to ask many questions that would be revealing of my economic ignorance rather than helping to explain poor productivity in NZ.

So starting with your graph of business investment as a percentage of GDP, if I’m understanding this correctly for every dollar we earn we invest one cent. The implication being if we invested more and did so sensibly then we would be rewarded by increased productivity – making us wealthier.

Is it worth while considering who invests and why they invest? 50 years ago in the UK discussion about investment meant medium and big firms buying forklifts or cranes or building new factories. Now in NZ I see very few factories but plenty of very small businesses and self-employed contractors. So an example of investment would be my son-in-law buying a trailer and a new van for his house maintenance business. Clearly he did so because he wants to be more productive and if he is successful he will employ more staff and pay himself more. If this is typical NZ investment then recent factors keeping investment low will be the age of owners of small businesses and lack of capital for young ambitious business owners. The 75 year old who received $4k for a recent highly skilled repair to by bathroom is unlikley to invest capital in his business (in fact he takes two days off this week to go fishing) meanwhile my son-in-law in his thirties cannot easily borrow from the bank, they prefer mortgages or loans to businesses where the owner has property as security.

Is there any data on investment by business size? By size I mean distiguishing between a business that is owned by the boss and businesses that are owned by non-employed shareholders?

If there is a smidgen of truth in my conjecture what could the government do about it?

LikeLike

For every dollar of gross domestic product roughly ten cents in business investment. This is gross investment. Obviously there is a great deal of depreciation so net investment (additions to the capital stock are much smaller)

There probably is data of the sort you are looking for in the SNZ linked firm database. I supposed one could also go thru the accounts of listed companies (altho the biggest companies in NZ are the banks who aren’t listed here). I suppose the thrust of my argument is that we want a climate in which many more big companies, and small companies becoming big, want to invest more, whether using outside capital or retained earnings.

But, yes, financing constraints can be very real for small business. It is an information problem mainly – how can a potential lender know which small business will do well and which won’t. Without taking collateral they would have to charge such high interest rates that only the riskiest potential borrowers would be willing to borrow.

LikeLike

Thank you for correcting me. And I thought my feel for maths was great – I will have to be more careful. Certainly 10 or 11 cents per dollar seems much more rational than 1 cent.

When laymen think about business success they envisage Birmingham UK before the war, Toyota and fellow Japanese car builders and Google and Amazon in Silicon valley. All these were surrounded by large numbers of small highly competitive businesses with a continual churn of success and failure. Think big needs to be ‘think small’.

LikeLike

With comrade Jacinda Ardern stupidly stopping oil and gas exploration with no consultation and at a ideological whim, GDP and business investments will start to decline considerably in this sector. It is going to cost upwards of NZ $28 billion in lost GDP. With Shane Jones squandering $3 billion in mulching trees that are supposed to be planted and vote buying with free money handouts willy nilly, don’t expect any of that lost $30 billion to be recovered anywhere else in any new industries. What a disaster.

I guess the Jacinda Ardern solution is to pour more tourists into the regions. Our NZ engineers can get new jobs as cleaners and waiters. Jacinda’s idea of no job losses.

LikeLike

Bob Atkinson

Think big projects were long before your time. Most public reference to them is negative. However you should go and read about them. There were only 5 projects. In my view the projects themselves were “positive” in final outcomes, but were commenced at a time of financial stresses around the world, particularly the OIL CRISES of the 1970’s and the WOOL Stockpiles of the 1980’s when China, our biggest buyer of wool, ceased buying altogether

During the 1980’s many of NZ larger “Blue Sky” companies decided to venture overseas, particularly Australia, with “non-blue-sky” Fletchers expanding multi-nationally. To the best of my knowledge every one of them failed within 5 years. New Zealand does not have a successful track record of our larger companies venturing or expanding offshore. Even now we have the example of Fonterra making serious mistakes in China and Australia. Fortunately Fonterra’s mistakes are not life threatening, but certainly not inspiring. Fletchers are still pulling back to home base only to fail dismally here at home

NZ’s strength was import substitution. Roger Douglas put paid to that. Take a walk around NZ’s giant $2 shops. Bunning’s, Mitre 10, Target, Warehouse, and examine the country of origin of most of the products. They are sold at prices that would be impossible to manufacture in NZ at a profit

I am waiting for someone to suggest some original businesses that NZ could grow to international standards rather than simply pontificate about something nebulous

Reading about Think Big reveals an episode in NZ history I knew nothing about “The Maori Loans Affair” – Try reading that

LikeLike

Note: The driving force behind Think Big was the UK’s entry into the EEC and the discontinuation of the UK taking the bulk of our Meat and Butter and Lamb. Something had to be done. Yet most of the current-day commentary about think big suggest NZ would be better off if they hadn’t happened

Something had to be done – yet I have never seen anything offered up

After 40 years they’re still complaining

LikeLike

That is not an interpretation of history I’d agree with. The Think Big projects were more about a combination of the take-or-pay agreement re Maui gas that the Kirk/rowling govt entered into, combined with the 2nd oil shock and the associated surge (thought at the time by some likely to be sustained) in oil prices.

What should have been done was to remove protection and subsidies etc and allow the exchange rate to have depreciated considerably. If we’d done so, especially with migration policy as it was at the time, we would have been pretty positioned for the subsequent 35 years.

LikeLike

Is your advice regarding the removal of protection and subsidies contemporaneous or with hindsight

I lived through that period of the oil shocks and carless days. I don’t recall any alternative contestable solutions being offered such as removal of protection and subsidies and reduction of the exchange rate. The dominant image was NZ was hostage to an energy problem. Was the building of the Clyde Dam, expansion of Marsden Point Refinery, and expansion of Tiwai Point pot-line mistakes? Currently it appears that NZ has a looming energy problem as a result of immigration. Over the past 4 months wholesale electricity prices have fluctuated from $100 per Mw/h to over $700 per Mw/h due to shortage of water in the lakes. No publicly offered plans for the future.

I lifted much of my comment from wikipedia. There were 8 projects, 5 of which got off the ground. All targeted at energy. As compared to an omnibus total solution such as a reduction of the exchange rate which would presumably be felt across the wider economy regardless of whether they were the object, and that appeared to be NZ’s exposure to energy costs. In my experience, targeted solutions are measurable and can be re-assessed.

Are you suggesting the removal of protections and subsidies should have been applied only to these energy projects?

Right now a similar set of circumstances is playing out with the Government cancellation of NZ Oil and Gas exploration. NZIER today pronounce the cost of that decision to be $30 billion per year through to 2050. No indication of subsidies and exchange rate solutions. Just a continuation of exploration

What happened when the NZ exchange rate dropped below USD $0.50 a few years ago. Did that produce a desired investment response?

LikeLike

I was 17 in 1979/80, but there were plenty of economic policy advisers at the time who were proposing exactly the sorts of policies I referrred to. The Economic Monitoring Group of the Planning Council was one key outward-facing group (one of their reports here http://www.mcguinnessinstitute.org/wp-content/uploads/2016/11/NZPC-March-1980-New-Zealands-Long-Term-Foreign-Trade-Problems-and-Structural-Adjustment-Policies.pdf ) but the Reserve Bank and Treasury took much the same view. It was the stance of people like Don Brash (who was, I think on the Planning Council), Ian McLean (the “more-market Nat. MP), Len Bayliss (I written here previously about his confrontations with Muldoon on such issues in the early 80s) and Derek Quigley. The exchange rate was a big focus for macro -oriented people, partly reflecting the wide current account deficit, and partly the sharp fall in the terms of trade and terrible productivity indicators thru that period.

These people would have argued for a pretty comprehensive lifting of subsidies and protection (and I’d agree with them, based on best econ analysis available then).

Re oil and gas, I’m not suggesting the resource shouldn’t have been used (altho take or pay tempted govts down bad paths), and I oppose the current govt’s exploration ban.

As I noted in an earlier post, it is possible the Clyde Dam has ended up economic, but if so mostly because of the big change in immigration policy unforeseen in 1981. Even if it was economic, the process for getting it to happen reflected very poorly on the Muldoon govt.

Re the exchange rate, the fall below 50c was brief and in the middle of a severe recession and financial crisis. It was a risk event. A reasonable test would be, say, five years in which policy reforms allowed the exchange rate to fluctuate around 50c.

LikeLike

Exchange rate at 0.50% would force up the price of imports and the corresponding rise in interest rates. Foreign companies get to buy up local NZ assets and companies struggling to make a profit with rising interest rates.

LikeLike

I agree with your conclusion that the exchange rate was the main factor. I also wonder if high internal hurdle rates could be a factor. I have seen this attitude before in closely held or oligopolistic industries. If this is in fact going on, one thing that might change attitudes is to unleash more competition, so companies face risk if they choose not to invest. I believe the PC keeps making sensible suggestions about how to increase competition, which successive governments have ignored.

LikeLiked by 1 person