There have been a couple of interesting polls that caught my eye lately on the government’s handling of specific issues.

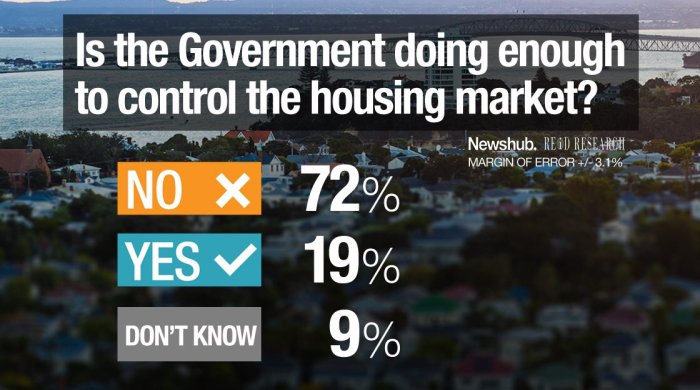

The first was from Newshub on housing

Taking the wording literally, the last thing I’d want is the government “controlling” the housing market. They (this government and its predecessor) have done quite enough to mess it up as it is. It looks as though real house prices nationwide will have risen by around 50 per cent in both the previous Labour-led government’s nine years in office, and in the current National-led government’s nine years in office – a bit more in the earlier government’s term (which included a 10 per cent fall in nominal house prices in 2008) and a bit less in the current government’s term.

We simply didn’t have today’s problems before governments (central and local) took powers to “plan” – something that seems to have worked about as well as Eastern European planning more generally did during the Communist decades. But I don’t suppose the respondents were interpreting the question quite that literally. It looks like an overwhelming expression of a sentiment that something (probably quite a lot) needs to be done.

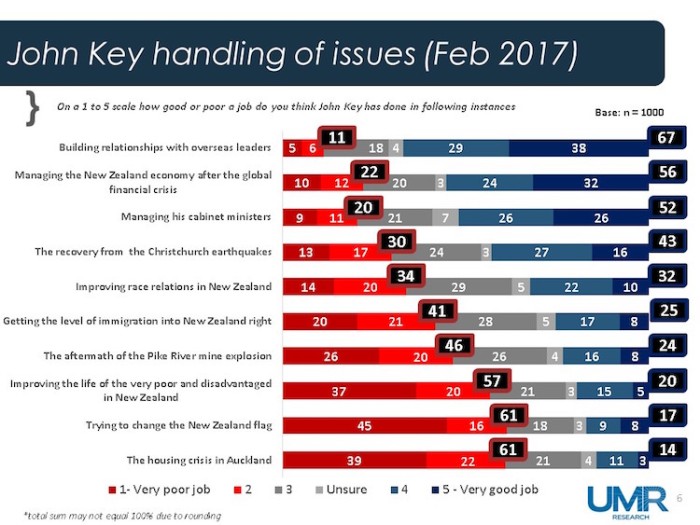

At the time of John Key’s early resignation from Parliament last month, there was some UMR polling reported on how well Key had handled various issues. On most of the issues, we can probably treat it as a proxy for how the government had handled those issues. This was the main graphic.

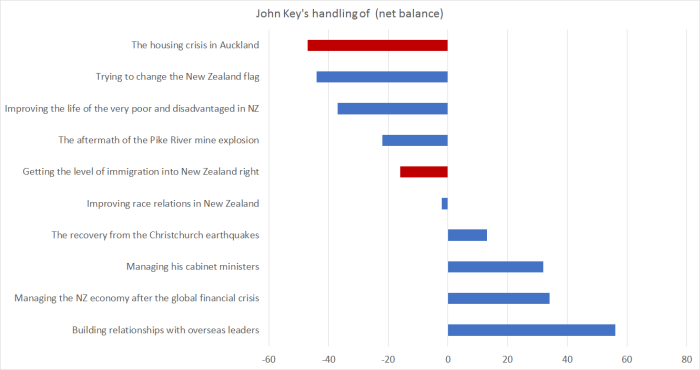

I found it a bit easier to read if I converted it into a chart of net balances – the difference between of those saying “good” or “very good” and those saying “poor” or “very poor”.

In some areas, Key rated very well, as one might expect (he did after all lead his party to three election victories). Relationships with foreign leaders scored as highly as you might expect from someone who seemed generally to be regarded as “the sort of person you want to have a beer with”. And if the government didn’t do anything much in the wake of the “global financial crisis”, arguably it didn’t have to – after all it was mostly a North Atlantic crisis, and when the crisis ended there, so did the worst of the backwash in the rest of the world. But if you are in office, you tend to get the credit.

In some areas, Key rated very well, as one might expect (he did after all lead his party to three election victories). Relationships with foreign leaders scored as highly as you might expect from someone who seemed generally to be regarded as “the sort of person you want to have a beer with”. And if the government didn’t do anything much in the wake of the “global financial crisis”, arguably it didn’t have to – after all it was mostly a North Atlantic crisis, and when the crisis ended there, so did the worst of the backwash in the rest of the world. But if you are in office, you tend to get the credit.

Of the other answers, the only one that really surprised me was the quite negative Pike River score. Perhaps more people than I appreciated really did think the mine should have been re-entered to try to retrieve the bodies?

But of course the two results that really caught my eye are the ones I’ve highlighted in red. Respondents clearly didn’t think, on balance, that John Key had done well in “getting the level of immigration into New Zealand right”, and were really really negative on how well the “housing crisis” in Auckland had been handled. Perhaps the phrasing was a bit emotive, but when 61 per cent of people thought Key had done a bad job, and only 14 per cent thought he’d done a good job, the overall message is pretty clear. The public just don’t buy the profoundly dishonest line that Key and his successor have run, that somehow unaffordable house prices (and some of the worst house price to income ratios anywhere in advanced world) are “quality problems“. They are, quite simply, a scandal, and a sign of near-total failure (economic and moral) of policy in this area. And this from a party that once prioritised home-ownership, and notions of a property-owning democracy.

Instead, we now have a governing party (notionally from the centre-right) that can’t or won’t do anything much about freeing up urban land supply, and can but won’t do anything much about cutting back the flow of non-citizen immigration that aggravates and amplifies the housing affordability problems. It looks a lot like a deliberate attempt to skew wealth towards those who already have it, away from those who don’t. I don’t suppose it is quite so deliberate, but the effect is the same.

I happened to have the 1975 National Party manifesto on my desk. They had some really flaky stuff to say about housing – a bit of that below – but at least there was some realism on this specific point.

“The first way we will do this is by admitting honestly that we cannot create a better environment when people are pouring into the country faster than anybody can provide houses – any kind of houses. Thus immigration will be cut from the current rate of 30000 per year to around 5000. This will give us the breathing space we so desperately need.”

National was in opposition then. But it would be a good line for Opposition parties this year – or for the government – even if they all think they are really serious, this time, about sorting out the dysfunctional, over-regulated, urban land supply market.

As I said, that 1975 National manifesto had some astonishing stuff on housing. I suspect it wasn’t unique to them. The Values Party – sometimes regarded as the world’s first environmental party – did rather well in the 1975 election, getting 5 per cent of the vote in an FPP election. And I doubt the Labour Party’s stance then would have been that much different. But here is what the National Party – just about to score a huge landslide victory – was promising:

National has developed a complete plan for “the cities”. And in doing so has become the first political party in New Zealand to include a serious urban development programme in its election policy.

…..

First, we will make moves to limit urban sprawl. Second, we will set out to save the beauty that already exists. And third, we will ensure that all new buildings contribute to an improved environment, at all times remembering that cities are people and that the social factors are all-important.

When a city sprawls, it destroys productive farmland and inevitably this also leads to decay in the inner city. But sprawl can be stopped. It has been done overseas and we will do it here. We will change the Town and Country Planning Act to provide legal powers to literally “fence off” the cities.

….

….the government will encourage and finance new and better forms of high density housing. This will not mean high rise apartments. We will build not just houses, but whole new communities. Ones in which people will want to live.

And so we have metropolitan urban limits, rural/urban boundaries, and all the associated restrictions that have given a land-abundant country some of the more expensive suburban and urban-periphery land around. It was bad policy then, as it is now, but for the 15 years or so after those words were written New Zealanders were protected from the worst of it because population growth was very sluggish – between the exodus of New Zealanders to Australia, and the reduced inflow of non-citizen immigrants.

What worries me now is that both main parties seem to believe, in principle at least, in freeing up urban land supply. But it remains a great deal easier to pledge allegiance to that principle, than to do something serious about it. Eight and half years into this government and very little has been done, even though the rhetoric has been roughly right since before they came to office. Perhaps a Labour-Greens government really will be different, but if one is to take that prospect seriously perhaps it would be a good to see some agreed “Housing affordabilty and land use rules”, to match the recent welcome budget responsibility rules. Not much has been heard from the Greens on this since their co-leader last year courageously advocated a substantial fall in house prices. And the Greens historically have had a lot of sympathy with lines like those in that National Party 1975 manifesto.

I’m all for liberalising the urban land market. But there needs to be a lot more realism about the prospects of substantial change. I don’t favour cutting our immigration targets mainly for house price reasons – in principle at least, that problem could be better dealt with in other ways – but given the scale of the housing problem, the clear public discontent over housing unaffordability, and the much greater ability for governments to adjust immigration targets than to put in place new planning laws, it simply seems reckless – and frankly ideological – not to wind back quite substantially our target rate of non-citizen immigration. For the Greens, who put a lot of emphasis on the physical environment, and for Labour – historically the party of the working class New Zealanders – it should really be a natural policy call. I’m not sure why it seems not to have been so far. Perhaps it is just fear of being tarred as somehow like Trump or Le Pen or whoever, even though our rate of legal immigration is typically far higher than those in almost any OECD country (a bit ahead of even Canada). But even if your own natural biases are somehow pro-immigration, surely it is now past time to take a hard look at the New Zealand experience: New Zealanders’ incomes haven’t been boosted by large-scale immigration, and housing for their children is rendered ever-more unaffordable by the toxic mix of planning restrictions and rapid population growth. It is well past time to be cutting the immigration targets quite severely.

Of course, not everyone agrees. I notice that the New Zealand Initiative has a new report out, Manifesto 2017 , outlining in very upbeat style their recommendations for what the next government should do. It is 80 pages long, and I might offer some thoughts when I’ve read it, but I did do a quick search of the document for references to immigration policy, especially in light of the very recent Initiative report on that topic (which I reviewed in a series of posts). There wasn’t much, but I did find this

Our report The New New Zealanders argues few countries have as successful

migration and integration policies as New Zealand. It is yet another aspect of New Zealand to be proud of and celebrate.

If only it weren’t for those pesky unaffordable house prices, and levels of productivity that languish far behind those of other advanced economies. It would good, just once, to see the evidence of the “success” – for New Zealanders – of our immigration policy.

In passing, this weekend has brought up the second anniversary of my move to become a stay-at-home parent, and thus the effective second anniversary of this blog. I’ve been thankful for all the readers and the various comments/challenges various of you pose at times. A while ago my 13 year old son asked me how long I’d keep going with the blog. I responded that it might be two years or it might be 30 years, depending on whether I still had things to say, still had readers, and whether doing the blog came at an opportunity cost, to other things I might want to do, that outweighed the fun and stimulus I’ve had from continuing to do it. There are rare days when I wonder if I still have much to say, that hasn’t been said 10 times already. Then again, the other day I found a list on my desk dating back to 2015 of various topics I could usefully cover. Many of them I still haven’t got to, and indeed I noticed this morning a book in a pile by my bed that I’ve been meaning to write about since I began. So, for the time being at least, I’ll keep on as I have been.

They would be okay for the next few years, but once you get even 10 years out from here, there would need to be a lot of other expenditure cut to keep spending to around 30 per cent of GDP, even if (a) the two parties resume NZSF contributions soon, and (b) investment returns proved to be pretty good. I’m genuinely puzzled how they propose to square that circle.

They would be okay for the next few years, but once you get even 10 years out from here, there would need to be a lot of other expenditure cut to keep spending to around 30 per cent of GDP, even if (a) the two parties resume NZSF contributions soon, and (b) investment returns proved to be pretty good. I’m genuinely puzzled how they propose to square that circle.

In both countries the current unemployment rate is around 1.5 to 1.7 percentage points higher than it was in the year or so prior to the global downturn. And neither country was troubled by a domestic financial crisis, nor did they run out of room to use conventional monetary policy. The monetary policy authorities should have been able to do better. If I look across the monetary areas in the OECD (again replacing individual euro area countries with the region as a whole), the only places with a worse record on this score – unemployment rates now compared to the pre-recession levels – are:

In both countries the current unemployment rate is around 1.5 to 1.7 percentage points higher than it was in the year or so prior to the global downturn. And neither country was troubled by a domestic financial crisis, nor did they run out of room to use conventional monetary policy. The monetary policy authorities should have been able to do better. If I look across the monetary areas in the OECD (again replacing individual euro area countries with the region as a whole), the only places with a worse record on this score – unemployment rates now compared to the pre-recession levels – are: