If I go on finding myself agreeing with Graeme Wheeler, there won’t be much point writing about OCR announcements. But, as it happens, he has only three more to deliver.

I could quibble about a few details in this morning’s announcement, but the only one I wanted to highlight briefly was this proposition

Monetary policy will remain accommodative for a considerable period.

In six months and a few days, the Governor will have moved on. We’ll then have an acting Governor, with no Policy Targets Agreement, for six months. And not until this time next year will we have in place a monetary policy decisionmaker, with an agreed target, who can make moderately credible statements about possible monetary policy decisions over the medium-term. So to be strictly accurate, that sentence should probably have read something like

“If the forecasts underpinning today’s decision are roughly right, and if my successors have (a) the same target I do, and (b) the same interpretation of that target, and the same reaction function, then monetary policy will remain accommodative for a considerable period.”

But in this post, I’m backing the Governor, and one line I was particularly pleased to see was this one (emphasis added)

Global headline inflation has increased, partly due to a rise in commodity prices, although oil prices have fallen more recently. Core inflation has been low and stable.

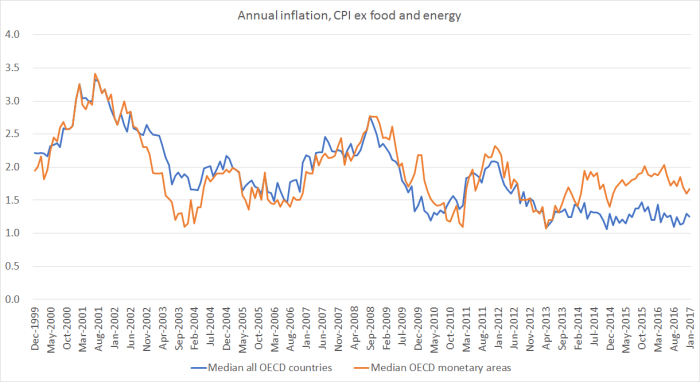

I made that point here a while ago, so I was pleased to see the Reserve Bank also highlight the point. Here is what I mean, using the OECD’s data on CPI inflation ex food and energy – the one readily available and consistently compiled core inflation measure.

I’m using monthly data, to be as up-to-date as possible, and New Zealand and Australia don’t have monthly CPI data. But the comparable quarterly chart doesn’t look materially different.

I’ve shown two lines. The first is the median core inflation rate for all individual OECD countries (with monthly data). But that includes 19 euro countries (plus Denmark) that have only one monetary policy. So the second line is the median core inflation rate for the distinct monetary policy countries/areas – ie delete the individual euro area countries, and replace them with an inflation rate for the euro area as a whole. I’d probably tend to emphasise that measure.

But on neither measure is there any sign that core inflation has been picking up at all. And although the US has been raising its policy interest rate to some extent, there have been more cuts in policy interest rates in the last 18 months or so (the sort of time it takes policy to work) than increases.

Of course, that is only actual inflation outcomes. Perhaps there is more inflation just ahead of us – a story markets seem to have taken a fancy to.

For what it is worth, international agencies still thought there was a negative output gap across the advanced world last time they looked (the OECD thought it was -1.4 per cent last time they updated their published forecasts).

The unemployment picture – another read on excess capacity and resource pressures -is a bit different. For the G7 countries as a whole, the unemployment rate is now a touch below the troughs reached at the peak of the last boom. For the OECD group as whole – even including places like Greece – it is only around 0.7 percentage points higher than at the peak of the last boom. For the median OECD country, the unemployment rate now only about half a percentage points above the average for the last boom year (2007).

Here are the unemployment rates for the largest OECD economies

The unemployment rates have been falling for some considerable time, and there has been no pick up in inflation yet. For each fall, of course, the respective NAIRUs must be getting closer, but it is probably safer to wait and see that core inflation has actually begun to rise – especially in view of the low starting level – than to simply assume that it must happen soon.

Of course, when one looks at unemployment rates what does tend to stand out is how little the unemployment rates in New Zealand and Australia have come down.

In both countries the current unemployment rate is around 1.5 to 1.7 percentage points higher than it was in the year or so prior to the global downturn. And neither country was troubled by a domestic financial crisis, nor did they run out of room to use conventional monetary policy. The monetary policy authorities should have been able to do better. If I look across the monetary areas in the OECD (again replacing individual euro area countries with the region as a whole), the only places with a worse record on this score – unemployment rates now compared to the pre-recession levels – are:

In both countries the current unemployment rate is around 1.5 to 1.7 percentage points higher than it was in the year or so prior to the global downturn. And neither country was troubled by a domestic financial crisis, nor did they run out of room to use conventional monetary policy. The monetary policy authorities should have been able to do better. If I look across the monetary areas in the OECD (again replacing individual euro area countries with the region as a whole), the only places with a worse record on this score – unemployment rates now compared to the pre-recession levels – are:

- the euro area as a whole (visible in the first chart above) where they did run out of conventional monetary policy options,

- Norway, and

- Turkey, not a paragon of economic management or political stability.

Core inflation measures have been picking up a little here, as they should have after the sharp cuts in the OCR the Reserve Bank had to implement. But our unemployment record – at a time when much of the rest of the advanced world has been able to run unemployment rates back near pre-recessionary levels without (yet) seeing signs of core inflation rising – is one reason why I think the Governor is quite right not to express any bias about the direction of the next change in interest rates, however far away (and delivered by a person yet unknown) that might be.

More a question than a comment: Are you saying the higher than previous rates of unemployment from 2004-2008 are due to policy positions by the RBNZ?

LikeLiked by 1 person

The RBNZ under Allan Bollard, engineered the collapse of a very buoyant NZ economy with aggressive interest rate rises with the OCR at 9% which forced commercial lending interest rates to 12% to 15% which was way above most of our trading partners. Complete carnage in the NZ economy, decimating 2 entire industries, the building industry and the risk financing sector with a loss of $6 billion in investor funds. This was entirely engineered by the RBNZ. nZ was in deep recession way before the GFC even arrived in NZ.

LikeLike

Yes, in significant part. They are the flipside of the fact that core inflation has run significantly below target. Some of that was pure choice – which risks did the Governor choose to run (eg in thinking about tightening in 2014, and then being reluctant to change track – and some just about bad forecasting (which the Bank shared with most other forecasters). Since the Bank seems to believe the NAIRU to be around 4.5%, and the Tsy believes it is somewhere nearer 4 per cent, almost by definition the Bank could have chosen to run policy a bit looser, and in consequence the actual unemployment rate would be lower.

Perhaps it isn’t the whole story (like most, our economy was a bit overheated just prior to the recession), but I think the UK story is quite instructive. Productivity growth has also been poor there, but nonetheless they’ve seen the unemployment rate fall below the pre-recession levels without yet any significant rise in inflation. See Japan too.

We don’t know exactly where the NAIRU is, but with an ageing population it is likely to be falling. As Donal Curtin argues here http://economicsnz.blogspot.co.nz/2017/03/jobs-and-spin.html

“Or another way of putting it is that I suspect the sky would not fall if our unemployment rate went into the low 4s or even below. Sure, institutional arrangements vary, and you can’t always (or even often) say that what works in one country will work everywhere else. But there are countries, as you cans see in the table below, which have got their unemployment rates down to lower levels than ours, without inflation starting to roar away (or even raise its voice much).”

Generally our labour market regulations are pretty supportive of flexibility and, hence, low equilbrium unemployment. There are aspects that work the other way – the unemployment benefit isn’t time limited and the min wage is quite high relative to market wages (by international standards) – but in a strongly performing economy we generally have one of the lowest unemployment rates in the OECD. At present, we aren’t much below the median advanced country’s unemployment rate, even including the likes of Spain and Greece.

LikeLike