The New Zealand Initiative starts their discussion of the implications of immigration for house prices in a quite reasonable manner.

Rising house prices is an increasingly discussed topic. Fast growing populations, particularly in urban areas, have increased the mean demand for housing. Migration is a major contributor to urban population growth. In an ideal world, the underlying market systems would automatically adjust, such that as demand for accommodation rose and prices increased, developers built more houses. Likewise, cities would invest in infrastructure to accommodate more people.

However, that house prices have not stopped rising for a number of years means New Zealand has not reached this ideal place, and the system is not geared to cope with demographic shifts. The effect is most acute in Auckland, where about a third of the country’s population lives.

Thus far, I imagine everyone is on much the same page. It was consistent enough with the lines from the Introduction that I quoted earlier in the week

Economists consider housing to be affordable when the median multiple is 3 or lower. In 2013, Auckland’s median multiple was 6.4, and in 2016 Demographia put it at 9.7. The Initiative’s housing research blames restrictive planning policy and resistance to urban development. However, against a policy-induced, near-fixed supply, additional demand for housing must contribute to rising prices.

It is pretty much ECON101: if the supply of something is largely fixed, at least in the near-term, and there is an increase in demand (especially an unforecast increase in demand), the price will increase. Quite how much will depend on the elasticity of demand. And the immigration contribution to population growth (and demand for accommodation) has been really large over the last 25 years, just as the land-use restrictions enabled by things like the Resource Management Act appear to have become more constraining. The Initiative regularly, and rightly in my view, inveighs against those restrictions. Without them, higher demand wouldn’t result in higher (real) prices for houses and urban land.

I also get that the Initiative favours large scale non-citizen immigration, but what I don’t get is why they won’t just be straightforward and say something like, “in the presence of land use restrictions, we recognise that high rates of immigration have been markedly increasing house and land prices, especially in Auckland. But our best professional judgement is that the longer-term gains to New Zealanders from high immigration are sufficiently large, that we should overlook the distortions and arbitrary wealth redistributions that the high house prices, associated with high immigration have resulted in”

Perhaps there is a case to be made along those lines. It is, mostly, implicitly what the Initiative is saying. But they won’t come out and say it directly, and instead have tried to shelter behind a short piece from a couple of MBIE-funded academics, Cochrane and Poot, who attempt to interpret the existing evidence to suggest that really immigration isn’t much of a factor in (Auckland) house prices at all.

MBIE is responsible to the ministers for immigration and housing (and, of course, has institutional bureaucratic incentives to maintain a large scale immigration programme). Both ministers were presumably coming under pressure a year or so ago, and so MBIE commissioned Bill Cochrane and Jacques Poot to do a short review of the existing literature on immigration and house prices, and to draw some conclusions about what might have been going on in the last few years (as distinct, say, from the last 25). That report was released in April 2016. Some of it also appears to have been motivated by political concerns around non-resident purchases of New Zealand residential property, but as Cochrane and Poot note, the existing data don’t shed much light on that issue at all.

The New Zealand Initiative summarise the conclusions of the Cochrane and Poot report, with no sign of any caveats or concerns, as follows

Economists Bill Cochrane and Jacques Poot surveyed available evidence on the impact of net migration in New Zealand, and suggest migrants are not to blame for Auckland’s housing woes, rather New Zealanders are.

Personally, I hope no one wants to blame individuals at all – migrants or New Zealanders. The issues are about policy and big picture forces, not about individuals acting in their best interests given those policies.

What is important to bear in mind is that there is a handful of formal studies that everyone tries to make sense of. The Reserve Bank – which historically has no dog in the fight about whether or not immigration is “a good thing”; they just want “the facts” – has produced several studies over the years, each of which suggested really quite large impacts on house prices as a result of unexpected changes in migration. And, on the other hand, Stillman and Mare produced a paper suggesting, using quite different techniques, that the effects are quite small. That is the formal relevant New Zealand literature. There is also a variety of results across these papers on which flows might have matter more (eg NZ citizens vs foreigners, arrivals vs departures etc). On my reading the studies aren’t very conclusive: many people who’ve thought the issues through probably think the various RB estimates seem a bit large (up to 10 per cent increases in national house prices for a one per cent change in population) and the Stillman and Mare ones are a bit small.

In her Treasury working paper on macroeconomic performance in 2014, Julie Fry summarised her take as follows:

On balance, the available evidence suggests that migration, in conjunction with sluggish supply of new housing and associated land use restrictions, may have had a significant effect on house prices in New Zealand.

Cochrane and Poot read, or report, things a bit differently. But it is important to remember that their mandate was to focus on the “last few years” – whereas the New Zealand Initiative generalise it to apply to our longer-term house price issues. And it is certainly true, that if we look at the big swing in overall PLT immigration in the last few years, a substantial chunk of that was about New Zealanders (net) not leaving at such a great rate, rather than about a change in immigration policy (ie the bit that governs foreign arrivals). Their summary is as follows (emphasis added):

Overall we find that the literature and the available data on population change suggest that visa-controlled immigration into New Zealand, and specifically into Auckland, in the recent past has had a relatively small impact on house prices compared to other demand factors, such as the strongly cyclical changes in the emigration of New Zealanders, low interest rates, investor demand and capital gains expectations. Consequently, changes in immigration policy, which can impact only on visa-controlled immigration, are unlikely to have much impact on the housing market.

There is quite a lot to unpick there.

First, it is a specific observation about the “recent past” – when immigration policy (affecting foreigners) didn’t change much, and New Zealanders’ behaviour did.

Second, to talk of “investor demand and capital gains expectations” as distinctive factors is rather disingenuous. Presumably, investor demand was partly a response to increased underlying demand for accommodation, and capital gains expectations partly a response to the actual interaction of increased demand pressures in the face of restricted supply?

Third, if interest rates – which aren’t some random variable, but have been low for a reason – were a major independent factor, we wouldn’t have seen Auckland house prices rising so much more rapidly than those in most of the rest of the country (bits that mostly haven’t seen the same population pressures).

Fourth, the policy sentence is, literally, a non sequitur. It simply doesn’t follow from what went before. If immigration policy hadn’t been changed in the period they looked at – and it mostly hadn’t – it gives you no empirical basis for concluding that a future change in immigration policy would have no effect on house and land prices. In fairness to the authors, in their text they elaborate, and highlight the lags in the process, and that short-term variations in immigration policy aren’t a very reliable means of managing overall net PLT flows. I totally agree with them on that, and oppose such short-term immigration management, but it is a quite different issue.

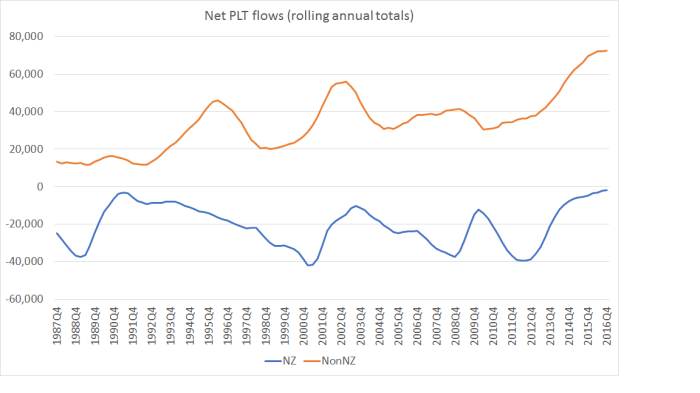

But even over Cochrane and Poot’s own period, it isn’t clear that they have the emphasis right. Here are net PLT flows with New Zealanders and non New Zealanders shown separately.

Over the period from around 2006 to around 2013 most of the variability was in the New Zealand citizen net flows. And specifically, from around 2012 to 2014 much of the pickup in PLT inflows was the change in New Zealanders’ behaviour – nothing about immigration policy – but over the last couple of years, there has also a huge increase in the net inflow of non-citizens, almost all of which is visa-controlled. It all represents additional demand for accommodation.

Cochrane and Poot note that much of the increase in non-citizen net arrivals has been from people without approval to stay permanently (ie students, and people on work visas).

the growth in inward migration has been particularly in temporary visa-controlled immigration (e.g. international students, temporary workers – including working holiday makers), as could be seen in Figure 9. The latter types of international migration flows are likely to have had a quantitatively smaller impact on house prices and to have contributed little to house price increases observed recently. The lesser demand on the housing market of temporary migrants has been shown with respect to students by BERL (2008). Generally, research on the differential impact on housing markets between those arriving and staying on temporary visas, compared with those arriving on, or subsequently obtaining, permanent visas still needs to be undertaken.

Most students probably aren’t buying a house. Most work visa arrivals aren’t either. But they all need a roof over their head, and add to the overall demand for accommodation, especially in Auckland. The authors play down this effect, noting that rents have increased much less than house prices have, but as I’ve illustrated previously, this divergence can be explained by the substantial fall in interest rates. When long-term interest rates fall, rental yields should be expected to fall. Absent population pressure, and in the presence of a well-functioning housing supply market, nominal yields should probably have fallen. Presumably expected demand for accommodation from students and short-term workers influences the willingness of investors to bid for properties, in turn pushing house price upwards. Population pressures don’t affect prices simply dependent on whether or not the new arrivals (or non-departures) choose to buy rather than rent.

One of the big challenges in modelling house prices is the so-called endogenity issue. A thriving city might see rising wages, and new people being drawn to that city. In the context, is it the immigration or the general prosperity that is raising house prices (given supply restrictions – real house prices tend not to rise for long without them)? It is an important in the short-term, but I’m less convinced that it is over longer-term horizons – eg the sort of 25 year period over which our immigration inflows and land-use restrictions have been interacting. Perhaps prosperity draws additional migrants in, but it simply isn’t likely that house prices would have risen much and for long on prosperity alone, without the additional people.

An ideal test – for economists anyway – would probably involve repeated surprise changes in long-term immigration policy. We could do a clean test if, say, every few years a random number generator decided how many residence approvals to grant to non-citizens each year. This year it might be 45000 (the actual target), another years 75000, another year 10000, and so on. We could then study the response of house prices in the wake of that clearly exogenous change in policy.

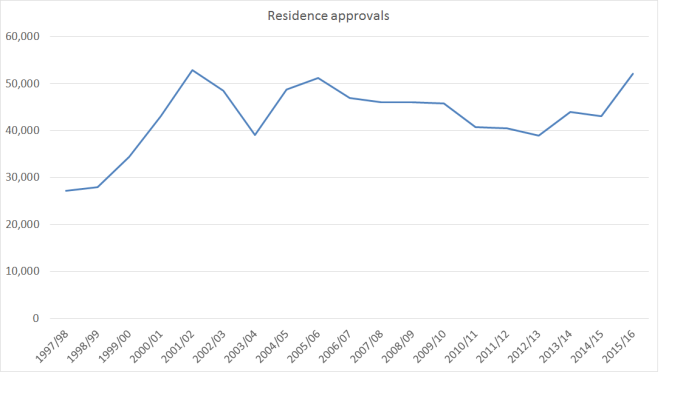

When it comes to New Zealand immigration policy, there simply haven’t been those sorts of changes researchers could study – other perhaps than the gradual opening up from the late 1980s to the mid 1990s, a one-time event. Here is the chart of residence approvals each year that MBIE provides the data for, back to 1997/98.

There hadn’t been a change in the target for 15 years until the very small cut announced late last year. And the actual variability in the approvals granted from year to year is mostly cyclical, and endogenous – dipping a bit when our unemployment rate was high, and then recovering lately. Econometricians use various clever tricks to try to deal with endogeneity, but the fact remains that at a policy level there have been hardly any exogenous changes at all. Just a very large net inward flow, varying a little from year to year, as a result of substantially unchanged policies. Trying to correct for endogeneity using recent data in particular might be a fool’s errand

Those residence approvals over 19 years added up to 817231 people. As I showed yesterday, the data suggest that perhaps 60 per cent of foreign arrivals settle in Auckland – that would be around 490000 people. Not all of them stay, of course, but even if only 80 per cent stay in the long term that is still almost 400000 people, adding to the demand for accommodation in Auckland in 19 years, as a direct result of immigration policy. Yes, there is lots of variability in the NZ citizen flow – Cochrane and Poot’s point – but over that 19 years, around 160000 New Zealand citizens (net) left Auckland for overseas. Again, as Cochrane and Poot point out, there has been considerable natural increase in Auckland’s population too. But immigration policy – visa-controlled almost all of it – will have boosted Auckland’s population in that time by almost 400000 people. And in a country – and city – which as they acknowledge does not have very responsive housing/land supply, that simply cannot have done other than put considerable pressure on Auckland house and land prices.

I’m still not sure why the New Zealand Initiative wants to avoid simply acknowledging that.

It is not as if this view is some contrarian Reddell-ite view held by no respectable or serious person. Read the speeches and reports of the Governor of the Reserve Bank and his staff, or those of the Treasury. Look at the analysis and reports of the IMF and the OECD – both generally supporters of immigration. It isn’t even treated as contentious that immigration has played a material role in house price inflation, in places where land use restrictions are in place. Go across the Tasman, and listen to the Reserve Bank of Australia for example – a nice recent example is here – or look at the IMF/OECD reports on Australia too (with a similar mix of rapid population growth and land use restrictions). When supply is substantially restricted and demand for housing increases, house/land prices will rise. Population growth is a key source of additional demand, and immigration – whether exogenously influenced, or endogenous to the economic cycle – is a huge component of population growth, especially in Auckland.

Flows of New Zealanders matter just as much as those of foreigners, and are often much more variable in the short-term (because less controlled by policy). Immigration policy – affecting foreigners – can’t sensibly attempt to stabilise housing market pressures in the short-term, but it can – and does – make a huge difference to housing demand over the medium-term. In a system with quite tight land use controls, that affect over the last couple of decades has been almost entirely deleterious – driving up house and land prices, and skewing wealth from the young to the old, the have-nots to the haves, and so on. Yes, we should fix land use regulations, but don’t pretend – as the Initiative tries to in this report – that knowing continuation of high rates of non-citizen immigration, in the presence of those land use restrictions, isn’t knowingly allowing urban house and land prices to be driven progressively further upwards, in Auckland especially, but not of course exclusively.

Spot on again, Michael.

LikeLike

Michael an outfit called Global Financial Data have compiled Seven Centuries of Real Estate Prices for the UK. https://www.globalfinancialdata.com/gfdblog/?p=3994

On nominal prices they have this to say.

“The only time when housing prices declined dramatically and hit their nadir was in the 1340s. And why was that? Because the Bubonic Plague decimated the population, reducing it by around one-third. Since there were fewer people, but no decrease in the stock of housing, prices and rents collapsed, falling more than at any time in history, even after 2008.”

And for real prices they say this.

“The real question, however, is whether housing prices increased more rapidly than inflation in general and by how much. The graph below adjusts British Housing Prices for inflation. The result is quite different. Again, housing prices tumbled as a result of the Bubonic Plague in the 1340s.

After that, however, housing prices remained relatively stable, after adjusting for inflation. In 1940, housing prices were no greater than they had been six hundred years before when the Bubonic Plague had struck. Since then, the story has been different. Housing prices have risen much faster than inflation”

Restrictive planning practices were introduced with the Town and Country Act of 1947.

If this data can be trusted it seems to indicate that a significant reduction of population with a fixed quantity of housing supply results in significant reductions in house prices. So surely we can assume if population increases by a significant amount and housing supply is unresponsive then houses prices will rise?

LikeLike

Thanks Brendon

Fortunately that aren’t many such truly exogenous shocks, concentrated over such a short time, but it is a sobering (if commonsense) result. It is a clean test – no fewer houses than before the population shock – whereas say in Akld there have been lots and lots of houses built in the last 20 years; just not nearly enough, and on land which is valued based on the regulatory restrictions.

I’m not sure who really doubts that a big increase in the population, interacting with the land use laws, is a big part of the reason why house/land prices have increased so much in Akld (or Sydney or…….). In the NZI case, it is just that they want the emphasis to go on fixed the regulations, not changing immigration. For that to be compelling – given the apparent difficulty of changing regulation – there needs to be a pretty compelling case that NZers as a whole are getting medium to long term gains from non-citizen immigration. That is what they attempt in the next chapter of the report. I’m not convinced they come even close to succeeding, or even to countering my analysis suggesting that large scale immigration may actually be making us poorer.

LikeLike

The largest anchor in terms of land restrictions is a severe height restriction due to 57 sacred mounts surrounding a very tiny CBD around the harbour. The Unitary Plan has delivered lowrise and low density to most of central Auckland due to Visual height limits called the viewshaft. This creates a 30 to 40km gap between a central high rise core and the 18 level metropolitan cities of Manukau, New Lynn, Albany and Sylvia Park. That gap is expensive and infrastructure costs become severely prohibitive in terms networking intercity rail or roading options.

Len Browns intercity rail from Britomart in the city to Mt Eden which is still an easy walking distance is now costing close to $4 billion. $4 billion and it does not even solve traffic congestion from the City to Mt Eden because Mt Eden is a low density suburb full of $2 million dollar single houses without even a decent shopping mall.

LikeLike

Economics 101, when Demand Exceeds Supply, expect price increases. Clearly demand has been rising and supply has been incredibly hard.

LikeLike

hmm; if demand for accommodation services increases and there is no additional supply, rents should accelerate rapidly; but it would seem a lower discount rate has been the main driver of historical house price increases; yet, investing in a rental property must carry a degree of risk which is unlikely to change that much through time; however, current gross rental yields are near six month deposit rates which are akin to the theoretical risk free asset; the plug? capital gain expectation I guess – perhaps partly driven by the anticipated flow of people but maybe more by an anticipated flow of money into a market that seems ‘as safe as houses’…..

LikeLike

Real rents have risen, even as real interest rates have fallen a long way

https://croakingcassandra.com/2015/11/23/what-has-been-happening-to-private-rents/

I’m unconvinced lower interest rates are an important driver of house prices: after all, there has been a huge corss-regional divergence in house prices even as interest rates have been falling, and interest rates have been low partly because global trend productivity growth/population growth (twin drivers of investment demand) have been trending down.

LikeLike

hmm; that is fair; meant to say agree with the young v old and outsider v insider issue; on the latter, I almost tripped over a pile of marketing brochures advertising reverse mortgages outside a high street bank the other day – get it while you can…(!!)

LikeLike

When you rent out a garage separately, it is counted as 2 dwellings. Therefore house rents out for $600 plus garage for $400 equals average rent of $500 a week even though the rent received is actually $1,000 a week. Average rents can be very misleading as the bond centre records each rent paid as separate dwellings usually referenced separately as unit 1 and unit 2.

LikeLike

I spoke to a lady that rents out her property for $350 a night through Air BnB. She reckons she gets 95% occupancy. Weekly rent data that economists use from the bond centre does not include Air BnB rentals as these are ad hoc rentals and do not lodge bonds with the bond centre. Air BnB launched 12 months ago and have already signed up 17,000 residential property for International and domestic tourists. Not available for weekly bonded rents and therefore weekly rents are up the proverbial creek.

LikeLiked by 1 person

Good point. This hasn’t come up before. It’s a huge challenge in places like San Fransisco. Of course the motels are all filled with beneficiaries.

LikeLike

Good analysis as usual. Honestly I’m disillusioned with the economics profession in general, they seem to come to whatever conclusion they are paid to arrive at irrespective of the facts and economics 101. I read the Cochrane and Poot research when it was released and thought it was somewhat sloppy and completely lacking in objectivity. Also even if you take their view that the increase in prices is due to factors such as “investor demand and capital gains expectations”, the pool of investors is also expanded by new arrivals who also have capital gains expectations.

Supply and demand are two sides of the same coin. I’ve often heard people argue that non-citizen migration isn’t a factor in the housing crisis, but simply that there are not enough houses being built. Or that migration isn’t a factor in the constant gridlock in Auckland, but rather the problem is that not enough roads are being built etc. If for whatever reason the supply is not responding quick enough, then yes the spike in demand (of which non citizen migration is a big part) is driving up housing prices and contributing to traffic congestion and other infrastructure woes. Of course Bill English would say that these are “good problems to have”. That isn’t to say that Labour party policies will be much better. Isn’t their current policy to have housing prices stay the same ? I’m not sure who that is supposed to appeal to, certainly not investors who want to continue to enjoy capital gains and certainly not people trying to buy their first house who would like prices to drop to a more affordable price to income ratio.

LikeLike

“Good problems to have” – “problem of success” – next thing, Michael, you might be called a “conspiracy theorist”;

https://www.tvnz.co.nz/one-news/new-zealand/because-think-he-john-key-describes-nicky-hager-conspiracy-theorist

LikeLiked by 1 person

The definition of a migrant also includes kiwis that have been overseas for more than 12 months and in the last 12 months returning kiwis number 30k and they inevitably end up in Auckland looking for work

LikeLike

In net terms, 3000 NZers left Auckland last year (on the PLT definition) Certainly fewer than in earlier years, but there is no actual inflow of NZers.

LikeLike

Yes but those that leave come from all over NZ but those coming in end up in Auckland as per your earlier analysis that point to a staggering 98% end up in Auckland in the last 3 to 4 years.

LikeLike

The Auckland gridlock has more to do with the 18 million inbound and outbound tourist traffic at the Auckland Airport.

LikeLike

But the 3000 outflow figure is the net of those NZers leaving AKld (having been living there til then) against the NZers returning to NZ and intending to settle in Akld.

In terms of internal migration, there has been a slow but steady net outflow of NZers from Akld to the rest of the country for the last 20 years (altho we don’t get post-2013 estimates until next year’s Census results are reported).

LikeLike

There was not one mention in the NZ Initiative report, nor in Michael’s blog article above, nor in any comment, of the role of commercial banks as money creators, and the affect that this has on house prices.

Up until the 1980’s, NZ house buyers obtained their mortgages from building societies, trustee savings banks and the Post Office Savings Bank (POSB). None of these financial institutions were money creators. rather, they were true financial intermediaries that took in money from savers, aggregated it, and lent it to borrowers. These financial institutions made their modest incomes from the margins between the interest rates that they paid savers and the interest rates that they charged borrowers.

Incredibly, to this day, this is what all high schools that teach economics, all polytechnics that teach economics, and all universities, teach their students is what commercial banks do.

However, this is NOT what commercial banks do. Commercial banks are money creators, not financial intermediaries. When a commercial bank grants a loan, it does so not by lending out its depositors’ money, but by creating a new deposit in its borrower’s bank account, simply by typing the amount of the loan principal into its depositor’s bank account.

During the 1980’s, financial deregulation brought about the demise of the trustee savings banks and the POSB, and commercial banks were quick to take advantage of the new ‘financial environment’. That period marked the beginning of the present massive increase in house prices relative to real incomes, from a ratio in 3:1 (in Auckland’s North Shore where I live) to 12:1 and climbing — until the inevitable crash!

Why is it that economists such as Michael Reddell, Olivier Hartwich of the New Zealand Initiative, and Shamubeel Eaqub, not to mention all the boffins in the NZ Treasury and the RBNZ, fail to acknowledge that the very nature of the present banking system is the root cause of the problem? Could it possibly be because they were all taught BS at university and have spent their working lives mingling with people similarly taught untruths?

LikeLike

Peter,

Can’t claim to speak for the others you name, but while totally agreeing that “banks create money”, I still don’t see that as in any way the root cause of the house price problem. I won’t attempt a lenghty defence, but we know that in cities without tight lad use restrictions, we don’t see house prices, and price to income ratios, skyrocketing, but rather stable low ratios. And those places have the same banking system we do, Australia does, and the rest of the US does.

LikeLike

Michael, if banks didn’t create ex nihilo the money that they lend, where would the money have come from to have enabled all those house buyers to bid up the price of houses to the ridiculous extent that they have?

How could it have been done with recycled savings?

It is my contention, and also that of Adair Turner and numerous other economists, that there simply wouldn’t have been sufficient saving available to lend for this to be possible, had banks not been permitted to create ex nihilo their loan principals.

LikeLike

PJM simple answer to a simpleton’s question, it is perceived value. When a foreign buyer decides to pay me $2million for my property, I can pay someone else $2.1 million for their house. I don’t borrow $2million. I only borrow $100k. It does not take many buyers to create a price expectation because house values are based on the last sale price. So one house a suburb sells for a higher value creates a expectation of a similar value throughout the suburb. Then people who already own houses sustain the market price as they trade between themselves. It is only those that do not have houses that need to borrow to get in.

LikeLike

PJM, you read too many conspiracy theories. Our banks, operate like any other business. They create loans, similar to any business that creates a sale. A contract exists between the bank and the borrower in a similar fashion to any business that raises an invoice, ie they create a contract between the buyer of their product and the business. That contract is always separate from the purchasing contract in a similar fashion that a bank has a separate contract with a depositor.

Like any business sales personnel can get carried away and sell more inventory than the warehouse is able to purchase and to ensure sufficient stock to deliver to the buyer. A banks loan department can also create loan contracts ahead of deposits being available but at some point the books have to balance out. If our banks do not have sufficient depositors funds locally they will source from overseas funding. It is really as simple as that.

LikeLike

And you, Getgreatstuff, as I have explained before, still don’t understand what banks actually do! Please ask Michael to explain it to you. He does understand, and has just said so, above. You really don’t need to be such an ignoramus anymore!

LikeLike

Don’t tell me you are a engineer trying to be a economist as well?

LikeLike

PJM, When a bank gets in financial trouble they call accountants. No one calls an economist to fix balance sheets.

LikeLike

Values have been climbing and everyone wonders how it is sustainable. Firstly NZ households have around $220billion of debt compared with $162 billion in depositors savings. The $60 billion shortfall is funded from overseas savings.

Nz household.value is $1 trillion plus but this valuation is derived from what the market ie ordinary people are prepared to pay for theses houses. There are a million households. People who already own homes buy in the same market so the prices are sustainable because if I can sell my house for $2million, I can buy another house more to my liking for say $2.1 million. I did not borrow $2million. I borrowed only $100k. The value is sustained because someone paid me $2 million for my property. Once I believe my property is worth $2million and the market went into reverse and someone came and offered me $1 million, I would not sell because I live there, I take the property off the market.

Therefore in order for the market to crash, there needs to be sustained loss of jobs, or sustained population decline. With international students and tourists pumping $20 billion of new money into the local economy, there is so much cash sloshing around it is very difficult to see sustained economic decline that leads to sustained job losses.

LikeLike

Getgreatstuff, in writing “Don’t tell me you are a engineer trying to be a economist as well?” you have denigrated yourself, not me.

By the way, your standard of written English is not too good. I’m an engineer, not “a” engineer!

I suggest that Michael should ask you to desist from practising ‘argumentum ad hominem’, as it lowers the tone of his excellent blogsite. Besides, it is unbecoming of someone who believes himself to be of superior knowledge and no doubt intelligence.

LikeLike

So an engineer then that dreams of becoming an economist. Better?

LikeLike

Getgreatstuff, your comment is irrelevant, and IMHO is inappropriate on this forum.

LikeLike

Ok you two. Time to stop.

LikeLike

Not housing related, Michael, but some really interesting stats on earning gaps between foreign students that moved on to PR after study and their NZ domestic student counterparts;

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11810806

And the real concern is this point made:

“The numbers may understate the earnings gap, as they cover only international students at government-funded institutions. The briefing says about 40 per cent of international students enrol at private training establishments (PTEs) which cater only for foreigners and receive no government funding.”

I wonder whether this income-gap factor has an effect on productivity, particularly in light of the further point made about these foreign student residency grants having squeezed out what they refer to as “other more valuable” residency applicants.

LikeLike

Interesting, thanks. Yes, it might well suggest a (modest) negative contribution to productivity, altho the example they used in the article – a 50 year old chief technology officer earning $120000 – didn’t strike me a necessarily hugely productive (I’d imagined that such a senior figure would be earning more than that if s/he was really good).

I’m still tantalised by the idea of only giving residency to people with a job paying more than $150K per annum (plus the refugee quota). It isn’t ideal, and probably skews choices away from relatively young people, but it goes in the direction of saying we want really/able productive people. At that sort of threshold we would probably bring in fewer people, but it would be clearer that they were ones making a signif econoinc/fiscal contribution. Perhaps it needs to be a bit age-related: start at $75K per annum for the under 30s, and move up by 25K for each five year age range thereafter, so that by 55 we’d only offer residence (and the prospect of state health care/NZS) to someone earning $200K pa.

It would also make for a cleaner market test of our universities and PTEs – they’d have to sell themselves on the educational value-add.

LikeLiked by 1 person

Nice, but without available jobs provided by industry priced at that level what’s the point of that target? We would just go back to closed shops after 5pm and tourists wandering around in ghost towns and no where to spend as the local retailers and restaurents are not able to pay workers to stay open.

LikeLike

NZ wage rates for those sorts of jobs wouldn’t be that high, of course, but (a) we’d have fewer migrants, (b) we’d be more sure of getting value from those who came, and (c) because the population would be growing less rapidly, many fewer people would be employed in, eg, building, and those people would be looking for jobs elsewhere. Some might be milking cows, some working in rest homes, some in…well, who knows where. We had early closing of shops and no restuarants open in the evenings in the great age of post-war immigration, the 50s and 60s, becuase of govt regulations, not because staff were too hard or costly to find.

LikeLike

Yes, I work in the tertiary sector and believe we have the ability to lift our international competitiveness significantly, particularly within the post-graduate and distance learning sectors – but the present government has deliberately sought to expand tertiary education export earnings in the gutter-end of the market.

LikeLiked by 2 people

Your idea tantalises me too. Note it would not stop foreigners doing low paid jobs because (a) historic obligations to some Pacific Island countries (b) Australians (c) working holidays (d) refugees (e) family members of immigrants.

When I obtained residency my younger wife and her four Melanesian children arrived with me. On balance NZ will benefit more from the five Melanesians than they will from me but there was no attempt to judge their abilities or potential only their health.

What your idea would do is kill what has been referred to as “Modern Slavery” in new Zealand (see http://www.globalslaveryindex.org ). As far as I can tell the increasing number of Slaves in NZ (from an estimated 600 to 800 in three years) is due to our immigration policy.

LikeLike

I’ve been thinking on your above proposal more and more – and I can see real benefit to NZ’s education sector. The pressure/incentive to target expansion of programmes in needed skills/knowledge areas would bring real focus to educators and education administrators. Additionally, new graduates and newly qualified trade staff would find employment post-qualification more easy – as employers wouldn’t be able to require/prefer 3-5 years experience for what are often entry level jobs. Worth thinking more about.

LikeLike

Interesting perspective. Australians don’t bother me – after all, wages are typically higher there than here, so there probably won’t be many wanting to do low wage work here, except perhaps as, in effect, working holidaymakers. Personally, I think those Pacific access quotas should be reviewed/tightened-up, partly because if we were ever to reduce the residence approvals target to around 10000 to 15000 per annum, those quotas, refugees, and non-NZ spouses of NZers would otherwise use up almost all the available places, and I really don’t have a problem with really highly skilled people coming here, esp in moderate numbers..

LikeLike

My knowledge of NZ’s interactions with Pacific Island nations is minimal. Keeping them friendly has value to NZ. I had the impression that some of them already have the majority of their population in Auckland so will further PI immigration be minimal?

I’ve always thought of refugees as a small fraction of our immigration intake but you are correct – reduce the quotas and they could be about 10% of our intake.

We can hardly stop genuine partners arriving to live with a citizen but do we need to include non-NZ spouses of NZers in immigration totals? They have virtually no impact on housing, are less likely to be taking low paid jobs and usually will be more culturally adept than most immigrants. I expect both the spouse and the NZer will be above average education / wealth. OK this does not cover step-children.

LikeLike

I think the Pacific quotas these days are mostly about Samoa,, Tonga and Fiji. As I understand it, people from the Cooks and Nuie – where the majority do now live in NZ – have NZ citizenship and can come and go as they please (so aren’t caught in the residence approvals target framework).

LikeLike