The Bank for International Settlements was supposed to be wound up after World War Two. That was agreed at the Bretton Woods conference in 1944, partly because the International Monetary Fund was being established, and partly because the BIS – based in Basle, just over the border from Germany – was perceived to have got altogether too cosy with, and protective of the interests of, the other side.

But the BIS – originally set up to handle reparations settlements and related issues – survived. These days it provides a variety of useful services to central banks around the world, provides a venue for various central bank meetings, and employs some interesting people and publishes some stimulating research. The BIS was once largely a North Atlantic affair, but these days even the Reserve Bank of New Zealand is a shareholder.

Prior to the financial crisis and 2008/09 financial crisis, the then head of the BIS Monetary and Economic Department, Bill White, was one of the few prominent establishment voices foreshadowing serious problems ahead. Inflation targeting, he argued, was one of the causes of the looming problems. Few national central bankers were at all receptive to his views (not all of which, by any means, were correct).

These days, the head of the Monetary and Economic Department is Claudio Borio, a long-serving BIS economist who, individually and with co-authors, has published a series of papers on matters financial and macroeconomic that have also tended to challenge the current “establishment view”. Over the last few years he – and the BIS – have been sceptical of case for official interest rates being as low as they’ve actually been, arguing that economic outcomes might even have been better if interest rates had been higher, and that monetary policy should be driven more by considerations around ‘financial cycles” than by (the outlook for) inflation. There is a lot of work resting behind these arguments, and even if I don’t end up agreeing with many of the conclusions, Borio’s articles and speeches are well worth reading for anyone interested in the issues (a recent accessible example is here, which I might back and write about substantively at some point)

The prompt for this post was a column that appeared in the (UK) Daily Telegraph a few days ago, in which their economics columnist Ambrose Evans-Pritchard sought to tie together the BIS/Borio views – which would have argued for a much tougher approach to monetary policy in recent years (at least on conventional definitions) – with the New Zealand Labour Party’s (and the new government’s) desire to amend our Reserve Bank Act. The article, which various readers sent me, appears under the somewhat flamboyant heading “Apostasy in New Zealand spells end of global central bank era” (the article is behind a paywall, but if you register you can get one article per week free).

It begins

The cult of inflation targeting began in New Zealand in the late Eighties. We may date its demise to a remarkable ideological pivot in the same country thirty years later, and with it the end of central bank ascendancy across the world.

Which would not, I’d have thought, be how Grant Robertson (or his senior colleagues in the new government) would have thought about what they appear to be proposing for New Zealand. They aren’t proposing to change the inflation target range itself (or even, so far as we’ve heard, move away from the explicit midpoint added in 2012), but argue that in adding a requirement (details to be advised) that the Reserve Bank pay explicit attention to the maintaining something near “full employment” (long-run sustainable rate of unemployment), they are simply converging on the international mainstream. In particular, they cite Australia and the United States.

And if pushed about what difference such a focus might have made had it been in the Reserve Bank Act in the past, Grant Robertson has suggested that the Reserve Bank would have been less likely to have tightened (as much) in 2014 – the shortlived, ill-fated, tightening cycle that proved unwarranted by inflation developments. In other words, if anything (and no one can be sure that different words, but same Governor, would have made a difference), it would have been towards having interest rates a little lower, a little sooner, than otherwise. In other words, the diametrical opposite of the approach that Claudio Borio, the BIS, (and Ambrose Evans-Pritchard) would have favoured. If anything, I suspect that the BIS view may have influenced Graeme Wheeler’s enthusiasm for raising the OCR in 2014 – with constant references to “normalising” policy.

Evans-Pritchard concludes his article

“[Western central banks] can excuse themselves for runaway asset prices, vaguely talking about the deformities of China’s Leninist capitalism, or the Confucian ethic, or some unfounded exogenous shock from Mars. It has let them cling to inflation targeting shibboleths for far too long. Premier Ardern is the canary in the mineshaft. It was the same New Zealand Labour Party back in the Eighties that pioneered so much of what we think of as globalisation [I’m really not sure where he gets that idea from], before it was gamed by the elites and began to go off the rails. The Party now wants to reassert the primacy of the democratic nation state, and to call time on the excesses – starting with a ban on home purchases by foreigners. The global axis is shifting.”

The BIS – or Evans-Pritchard – might (or might not) be right about the politics or the economics globally. But nothing we’ve seen or heard from the new Minister of Finance – or his colleagues – suggest that they have anything in mind for New Zealand monetary policy, or the mandate of the Reserve Bank of New Zealand, that steps outside the international mainstream at all. That might disappoint some – who actively prefer higher interest rates without first securing the productivity growth and investment demand which would sustain higher real interest rates – but what those people wish for is nothing like what Labour’s words suggest we in New Zealand are likely to be delivered.

Of course, the first big decision about monetary policy for the new government is who should be the next Governor. Individuals matter at least as much, arguably more, than the details of formal mandates. In almost all other countries, political leaders themselves get to appoint directly the head of the nation’s central bank. Obama appointed Janet Yellen, Scott Morrison (Australia’s Treasurer) appointed Phil Lowe, George Osborne appointed Mark Carney, euro-area heads of government appointed Mario Draghi, and so on. It is the way democratic societies typically work – actually, non-democratic ones come to that. But not New Zealand.

Here, unless he changes the Act, the Minister’s hands are tied. He will have to appoint as Governor someone nominated by Reserve Bank Board. All the Board members were appointed by the previous government, the advert for the job was framed under the previous government, all the Board members have endorsed the conduct of monetary policy (and the performance of the Bank more generally) in recent years, none has much experience in central banking, financial regulation, and none has any public accountability. And yet they will decide who will, single-handedly (for the time being) wield the levers of macroeconomic policy. It is a gaping democratic deficit – even if you don’t think actual policy should be run even a little differently in future. The Government could easily change those provisions, and bring New Zealand into line with standard international practice. It requires a simple amendment to the Reserve Bank Act, deleting six words.

Strong candidates for Governor aren’t exactly thick on the ground. But if the Minister were to make a change, or even to make suggestions to the Board, one of the people he shouldn’t go past actually works at the BIS. David Archer currently holds a senior position at the BIS, but until 2004 had spent a decade as first Head of Financial Markets, and then as Head of Economics (including carrying the title of Assistant Governor) at the Reserve Bank. He fell out with Alan Bollard and made his escape.

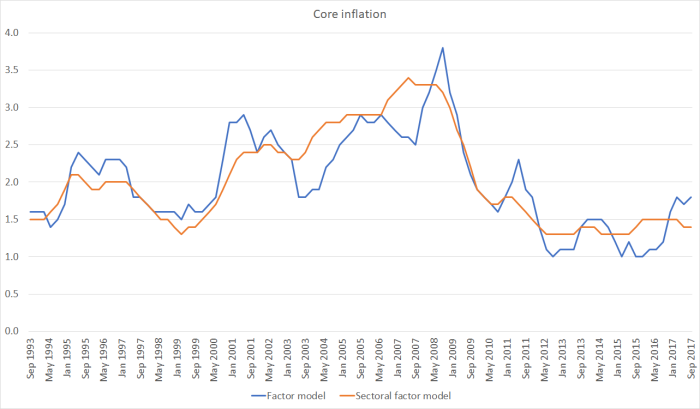

I worked closely with (and for) David across a couple of decades. Up that close you see both the strengths and weaknesses. David has a reputation as something of an “inflation hawk”. That was perhaps most obvious over 2003/04, when he was right – interest rates were too low for too long, and as a result core inflation got away on us (see the chart in yesterday’s post). But such reputations (“hawk” or “dove”) usually don’t mean very much – smart people will sometimes differ on how to read any data, and at different times the same person will end up on the different side of those debates. David’s greatest strength in my view is a high degree of intellectual curiosity, a demand for rigour, but an openness to debate, to challenge, to exploration of alternative views and ideas. It certainly isn’t the only quality one needs in a Governor, but it is an important one – perhaps especially in a single-decisionmaker system, but also as the Reserve Bank recovers from the Wheeler years. He is the sort of person who attracts capable people – again something the Bank will need in the coming years.

There are drawbacks, or gaps, as there are with all the possible candidates. David hasn’t had much involvement in bank regulation or supervision – now a big part of what the Bank does – and was (rigorously) sceptical of the Reserve Bank getting actively involved in discretionary supervision and regulation. I’m not sure how his views on these issues may have evolved over the years, but what could be counted on would be a rigorous and systematic approach to the application of the law, and to recommendations on any possible changes to the law. And, of course, he has now been away from New Zealand for 13 years – that brings the upside of extensive international contacts, but the downside of reduced familiarity with New Zealand (and the way the Bank’s own role in the public sector has evolved). That people here still recognise his potential value was seen in Treasury’s choice of him as one of the external reviewers of the recent (as yet unseen) Rennie review – Treasury is currently fighting to keep Archer’s comments secret.

David wouldn’t be a candidate for the status quo. If the Minister of Finance is really content with the status quo, he might as well just stick with the Board-led process, likely to end up appointing Deputy Governor Geoff Bascand. But whether around decisionmaking structures, transparency and accountability, and monetary policy goals themselves, all the public indications have been that the government is looking for change, and a lift in the overall performance of the Bank. If so, Basle might well, on this occasion, be one of the possible alternative places to look for someone to take on this very influential, powerful, role.