In September last year, former Bank of England Deputy Governor Sir Paul Tucker published a substantial discussion paper suggesting paying a sub-market, or zero, interest rate on some portion of the huge increase in bank deposits at the central bank that had resulted (primarily) for the large-scale asset purchase programmes central banks had been running (in the Bank of England’s case since the 2008/09 recession, but in some countries – including New Zealand and Australia – just since 2020).

In late October, I wrote about Tucker’s paper, and you will get the gist of my view from the title of that post, “A Bad Idea”. The Herald’s Jenee Tibshraeny picked up on that post and the following day ran an article on the Tucker tiering proposal, with sceptical quotes from several people including me. There was a difference of view in those quotes. As in my post, I argued that such an approach could be adopted without impeding the fight against inflation but should not be adopted, while others (as eminent as the former Deputy Governor, Grant Spencer) suggested that not only that it should not be done, but could not (ie would tend to undermine the drive to lower inflation).

The essence of my “it could be done” line was the same as Tucker’s: monetary policy operates at the margin, and so what matters for anti-inflationary purposes is that the marginal settlement cash balances receive the market rate, not that all of them do. There was precedent, in reverse, in several (but not all) countries that ran negative policy rates, where the central bank applied the negative rate only to marginal balances, while continuing to pay a higher rate on the bulk of balances (thus supporting bank profits, although the argument made at the time was that doing so would help support the monetary transmission mechanism).

So far, so geeky. But it turns out that after Tibshraeny’s first article, the Minister of Finance sought advice on the Tucker proposal, not just once but twice (first from The Treasury and then later from the Reserve Bank). In yesterday’s Herald, she reports on the two documents she got back from an Official Information Act request to the Minister. She was kind enough to provide me with a copy of the material she obtained.

The Treasury advice, dated 6 December 2022, does not explicitly say that it was in response to a request from the Minister, but it seems almost certain that it was. Treasury is unlikely to have put up advice off its own bat on a matter that is squarely a Reserve Bank operational responsibility without formally consulting with the Reserve Bank and including some report of the Reserve Bank’s views in its advice. We can assume the Minister asked Treasury for some thoughts, and Treasury responded a few weeks later with four substantive pages.

I don’t have too much problem with The Treasury’s advice on a line-by-line basis. Their “tentative” view was that some sort of tiering arrangement could be introduced without undermining the effectiveness of monetary policy.

There were a couple of interesting things in the note nonetheless. For example, it was good to have this in writing

and it was also interesting to read that “in previous discussions with the Bank they have indicated that they would consider introducing a zero-interest tier if the OCR were negative”.

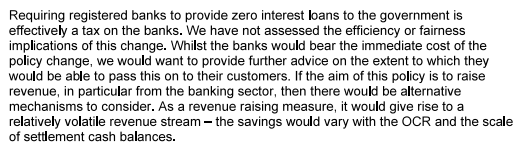

Treasury highlighted that a zero-interest tier in the current environment (large settlement cash balances, fairly high OCR) would be in effect a tax on banks with settlement accounts.

but strangely never engage with the question as to whether it would be appropriate for the Reserve Bank to impose such a tax (or whether they had in mind special legislation to override the Reserve Bank on this point).

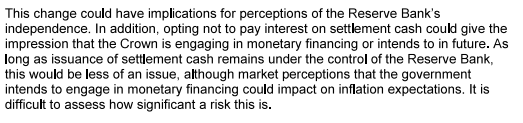

They also note some potential reputational issues

but could have added that these might be particularly an issue if New Zealand was to adopt such an approach in isolation (they neither mention, and nor have I seen, any indication any other authorities have seriously considered this option).

The Treasury note ends recommending not that the issue be closed down and taken no further, but that if the Minister wanted to “pursue this option” he should seek advice from the Reserve Bank and they offered to help draft a request for advice.

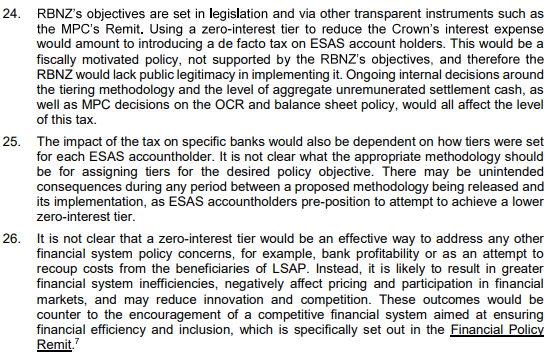

And so the Minister turned to the Reserve Bank for further advice, and on 2 February 2023 they provided him four pages of analysis (plus a full page Executive Summary which is more black and white than the substantive paper itself). The Bank seems pretty staunchly opposed to the tiering idea, but on occasions seems to overstate its case. And, remarkably, they never even attempt to engage on the question as to whether the market-rate remuneration of the large settlement cash balances created by their LSAP (and Funding for Lending) programmes are any sort of windfall gain to the banks (a key element of Tucker’s argument).

But much of what they say is reasonable. From the full paper

There is no real doubt that it can be done, and they draw comparisons between regimes in some other countries, more common in the past, where some (legally) required reserves were not remunerated at all.

I largely agree with them on this

departing from them on that final sentence of paragraph 25 (any tier could, and sensibly would, be set on the basis on typical balances held prior to any announcement or consultation document), and in the first sentence of paragraph 26 (since, from the Bank’s perspective, benefits from the LSAP are supposed to be a good thing – the Governor repeatedly champions them – not bad).

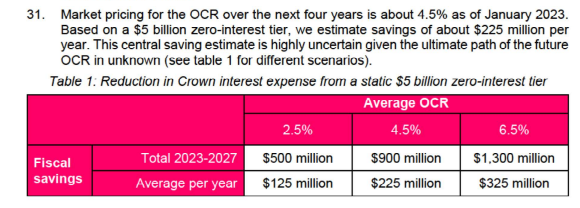

The Bank attempts to play down the amounts at stake, suggesting any potential gains to the Crown (and thus, presumably, costs to those subject to the “tax) would be modest. But they include this

I guess when your MPC has thrown away $10bn of taxpayers’ money, $900m over four years doesn’t seem very much (and these calculations are materially biased to the low end of what could be raised without adversely affecting monetary policy) but…..$900m over four years buys a lot of operations, or teacher aids, or whatever things governments like spending money on.

It is also a bit surprising that although the Bank notes that such a tiering tax would be likely to be passed through to customers, they provide no substantive analysis as to how or to what extent, and thus what the likely incidence of such a tax would be. It isn’t that I disagree with the Bank, but the analysis isn’t likely to be very convincing to readers not already having the same view as them (tiering is a bad idea).

They make some other fair and important points, notably that hold a settlement account with the Reserve Bank would be likely to be less attractive if doing so was taxed, in turning providing an advantage to non-settlement account financial institutions (broader settlement account membership is generally a good thing, conducive to competition and efficiency). But then they over-egg the pudding. This line is from the Executive Summary – and draws on nothing in the body, so has the feel of something a senior person inserted at the last minute

One of the points commentators on central banks often have to make to less-specialist observers is that banks themselves have no control over the aggregate level of settlement cash balances. Individual bank choices – to lend or borrow more/less aggressively – affect an individual bank’s holdings but not the aggregate balances in the system. And thus banks cannot materially impede future LSAP-type operations since there is no reason why the Reserve Bank’s purchases need to be constrained only to entities that already hold settlement accounts at the Bank. If the Reserve Bank buys a billion dollars of NZ government bonds at premium prices from overseas investors/holders, the proceeeds will end up in NZ bank settlement accounts whether the local banks like it or not. Same goes for, say, large fiscal operations like the wage subsidy. What might be more accurate – and I made this point in my original post – is that a tiering model carried into the future might motivate local banks to lobby harder against renewed LSAPs. From a taxpayers’ perspective that would probably be a net benefit, but one can see why the Reserve Bank might have a different view.

While I don’t really disagree with the thrust of either the Reserve Bank or Treasury advice neither could really be considered incisive or decisive pieces. Perhaps the Bank’s piece was enough to persuade the Minister (although there is no indication in the OIA material or in Tibshraeny’s article that the Minister has abandoned interest). A tiering regime of the sort discussed in the RB/Tsy advice would be an opportunistic revenue grab, representing either an abuse of Reserve Bank power or a legislative override of monetary policy operational independence, with truly terrible signalling and precedent angles. It could be done – so could many many bad things – but it shouldn’t.

(If you want a typically-passionate opposing view, try Bernard Hickey’s column yesterday, from which I gather he has removed the paywall.)

Big mistakes were made. The LSAP was unnecessary, ill-considered, risky, and (as it turns out) very expensive. The Funding for Lending programme continued all the way through last year was almost incomprehensible (if cheaper and less risky). Mistakes have consequences and they need to be recognised and borne, not pave the way for still-worse compensatory fresh interventions.

I’m going to end repeating the last couple of paragraphs from my original post

It is, perhaps, a little surprising that neither set of official advice shows any sign of engaging with Tucker’s paper itself, or with the author, a very well-regarded and experienced figure.