Once upon a time the Reserve Bank’s monetary policy was guided by a Policy Targets Agreement reached between the Governor and the Minister of Finance. These days things are different. As one of the more sensible aspects of the 2018 legislative overhaul, the new Monetary Policy Committee now works to a Remit (current one here) determined ultimately solely by the Minister of Finance. That is the way things should be: if officials are free to implement policy, the policy goals should be set by those whom we elect, in this case the Minister of Finance. At times, the Minister may put daft things in the Remit – as the current one did a couple of years back with the house price references – but that is how our system of government works (as it should).

Another sensible aspect of those reforms was a requirement that every five years or so the Reserve Bank should provide advice to the Minister on the form and content of the Remit, and that the Bank should have to undertake public consultation in bringing together that advice. These provisions seem to have been quite influenced by the Canadian model, with the very big difference being that the Bank of Canada has typically generated a large volume of research in support of each quinquennial review whereas for the first review – underway at present – the Reserve Bank of New Zealand has generated none. That is, sadly, consistent with the dramatic decline in the research output, whether on monetary policy or financial stability functions, of the Orr-led Reserve Bank.

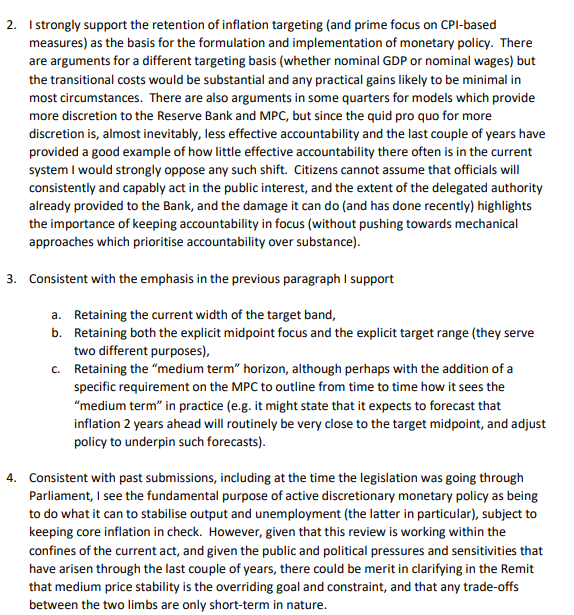

There have been two rounds of consultation. I wrote up and included a link to my submission on the first round here. The second stage of consultation invited submissions by today (although an email from the Bank today says that if you feel inclined they would be happy to receive submissions even on Monday).

It is January and I haven’t been particularly motivated to write about monetary policy. But I do approve in principle of the process of consultation on the Remit – and can only hope that future Governors make a more substantive and research-led fist of it – so thought I should probably make a submission on the second stage. It seems likely that neither the Governor nor the Minister are seeking any very material changes, but there are some longer term issues that need addressing – including dealing structurally with the near-zero effective lower bound on nominal interest rates – and there may be more scope for change on issues around the MPC Charter (which deals with MPC decision-making and communications), on which the Bank was also seeking views. So I got up this morning and spent a couple of hours on a fairly short submission. The full text is here

Comments on second round of Reserve Bank MPC remit review consultation

The first section has nothing that should be terribly controversial

A longer-term concern of mine has been the failure of central banks, here and abroad, to deal effectively with the lower bound, itself existing only because of passive choices by successive generations of governments and central banks. It would be unwise to lower the inflation target without fixing the lower bound issue, but if that constraint was removed there would be little or no good reason not to return to a target centred closer to true zero CPI inflation

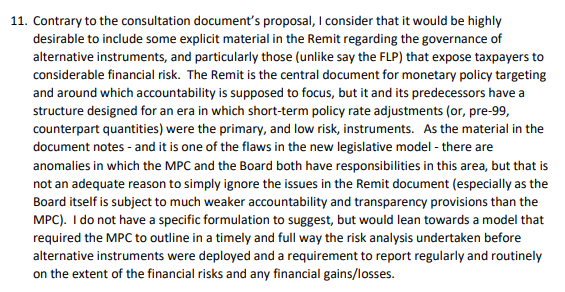

The consultation document addresses the question as to whether there should be text in the Remit around the governance of alternative policy instruments (like the – expensive and ineffective – LSAP). The Bank prefers not, but I reckon there is a pretty strong case, although the issue is complicated by the divided responsibilitities between the Bank’s Board – who know nothing about monetary policy – and the MPC. There is no easy solution, but the Remit is supposed to be the focal document for guiding monetary policy accountability.

On the composition and strcuture of the MPC there are several significant matters that can only be dealt with by amending legislation (I hope National is open to making some fixes) but I took the opportunity to lament again the blackball the Governor, Board and Minister have in place preventing anyone with current expertise in monetary policy or macroeconomic research/analysis from serving as an external MPC member, a decision that among other things cements the Governor’s continued dominance of the system (the Governor himself having only limited depth and authoritative expertise in such matters). But my main comments were about matters that are directly dealt with in the Charter and in the culture that has developed around the operation of the MPC since it was established.

If you felt inclined to make a late submission, the relevant email address is remit-review@rbnz.govt.nz

Reblogged this on Utopia, you are standing in it!.

LikeLiked by 1 person

Thank you for some excellent comment.

Perhaps a mechanical response may have had some merit.You have in other posts noted the quality and perhaps fallibility of the present MPC.

Fiscal policy is the business of Government ,but it would be nice if these activities are held somewhat to account by a strong and predictable independent monetary policy.

There is already now concern that Governments policies are redistributing wealth in NZ .As Friedman has said “ inflation is a tax”

It occurs to me that there may be certain deliberate predetermined outcome in present management ,Remits appear to give give less certainty than a robust PTA

Thank you for your submissions.

LikeLiked by 1 person

Michael

Have you read “The Price of Time” by Edward Chancellor?

He makes a strong case for Central Banks to be “deactivated” and to be required to be much less concerned about consumer price deflation and much more concerned about real asset values.

Ive not finished it yet, but it’s certainly made me reconsider the benefits/costs of activists monetary policy, the fixation on consumer prices, and very low interest rates.

Tim

LikeLiked by 1 person

Tim

Yes, I read Chancellor’s book last year. To be honest I was a bit disappointed with it (especially the sections on the more recent period). From memory, I don’t think he adequately grappled with questions around why real interest rates have been so low for so long, or what the implications might have been had central banks tried to consistently keep real short-term rates (the only ones they control) higher. Having said that, the last 3 years is a hardly a shining advertisement for discretionary monetary policy. The challenge always though is finding a robust and credible alternative (I’m currently reviewing another recent book, on monetary policy and the rule of law, which is heavily focused on the risk, perils etc of discretionary policy, and the repeated inadequacies of the Fed, but the – very smart – authors still struggle to identify a durable robust alternative).

LikeLike

Michael

Chancellor’s key point is that interest rates are low due to central bank activism

Which is probably correct

He then goes on to postulate all manner of distortions resulting from the enforced low rates

Which is also probably correct

In the context of RBNZ, I’d infer two points (if you accept his views).

1. RBNZ’s management of MP should not just be “stable prices”

2. It would be desirable for RBNZ to have dissenting views on its MP Committee

However, Ive not read the last couple of chapters of the book so cant say exactly what he would have RBNZ target if its not just stable prices

What Im enjoying about the book is that its a coherent criticism of the prevailing central bank narrative of unlimited capacity to do all things for all people.

Tim

LikeLiked by 1 person

I’m less persuaded that central banks, setting only an overnight rate, can have such great influence on long-term rates over a decade or more.

But certainly agree on your point 2. Instead we have a Potemkin village MPC, with external members selected for qualities that emphasise a reluctance to rock the boat, challenge mgmt, or speak openly.

LikeLiked by 1 person

Once upon a time central banks main influence on market interest rates was via the overnight market, then along came forward guidance, purchase/sales of longer bonds including ones not issued by the government, and all the various capital weightings which tend to impact bank investments.

It’s one of Chancellor’s points, that central banks have expanded their remits to enforce more and more control of the yield curve. All of which has led to them also imposing more and more regulation of the banks so as to limit the flow through of all the cheap money to speculative activities (which works until it doesnt)

LikeLiked by 1 person

Yes, it is his argument, but it doesn’t seem very persuasive (and seems to run contra to Occam’s razor – the simplest story remains that natural/neutral/whatever long term real rates have fallen a lot, and central banks have more or less just followed them down. Take NZ (or Aus) for example, where we had no RB bond purchases pre 2020 and a central bank that tended to undershoot its CPI inflation target, reluctant to accept that policy rates needed to be lower. If I recall rightly (and I may be forgetting something) Chancellor never touched on the fact, for example, that real house/land prices had not gone crazy in places that did not have restrictive land use regulation (much of the US). As the asset price that bothers people in NZ most has been house/land prices, fixing that is in the hands of NZ councils….

LikeLike

It strikes me that New Zealand could have the best MPC remit on the planet, but if the Reserve Bank wilfully ignores it, then this remit is of limited use.

I believe that under the current inflation remit the central bank is supposed to keep inflation at about 2%, and yet headline inflation is currently 7.2%.

By my calculations, this means inflation has overshot the Reserve Bank target by 260%.

Personally, if inflation persists at these levels until the October election, then I believe that the new government should look for a new Reserve Governor, rather than any change to the MPC remit.

How long should this continued central bank incompetence and vacillation be allowed to continue?

My patience is being washed away…

LikeLiked by 1 person