Once upon a time the Reserve Bank’s monetary policy was guided by a Policy Targets Agreement reached between the Governor and the Minister of Finance. These days things are different. As one of the more sensible aspects of the 2018 legislative overhaul, the new Monetary Policy Committee now works to a Remit (current one here) determined ultimately solely by the Minister of Finance. That is the way things should be: if officials are free to implement policy, the policy goals should be set by those whom we elect, in this case the Minister of Finance. At times, the Minister may put daft things in the Remit – as the current one did a couple of years back with the house price references – but that is how our system of government works (as it should).

Another sensible aspect of those reforms was a requirement that every five years or so the Reserve Bank should provide advice to the Minister on the form and content of the Remit, and that the Bank should have to undertake public consultation in bringing together that advice. These provisions seem to have been quite influenced by the Canadian model, with the very big difference being that the Bank of Canada has typically generated a large volume of research in support of each quinquennial review whereas for the first review – underway at present – the Reserve Bank of New Zealand has generated none. That is, sadly, consistent with the dramatic decline in the research output, whether on monetary policy or financial stability functions, of the Orr-led Reserve Bank.

There have been two rounds of consultation. I wrote up and included a link to my submission on the first round here. The second stage of consultation invited submissions by today (although an email from the Bank today says that if you feel inclined they would be happy to receive submissions even on Monday).

It is January and I haven’t been particularly motivated to write about monetary policy. But I do approve in principle of the process of consultation on the Remit – and can only hope that future Governors make a more substantive and research-led fist of it – so thought I should probably make a submission on the second stage. It seems likely that neither the Governor nor the Minister are seeking any very material changes, but there are some longer term issues that need addressing – including dealing structurally with the near-zero effective lower bound on nominal interest rates – and there may be more scope for change on issues around the MPC Charter (which deals with MPC decision-making and communications), on which the Bank was also seeking views. So I got up this morning and spent a couple of hours on a fairly short submission. The full text is here

Comments on second round of Reserve Bank MPC remit review consultation

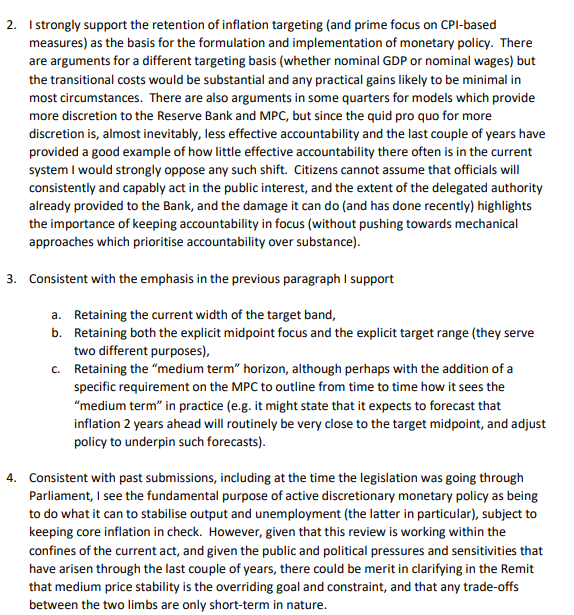

The first section has nothing that should be terribly controversial

A longer-term concern of mine has been the failure of central banks, here and abroad, to deal effectively with the lower bound, itself existing only because of passive choices by successive generations of governments and central banks. It would be unwise to lower the inflation target without fixing the lower bound issue, but if that constraint was removed there would be little or no good reason not to return to a target centred closer to true zero CPI inflation

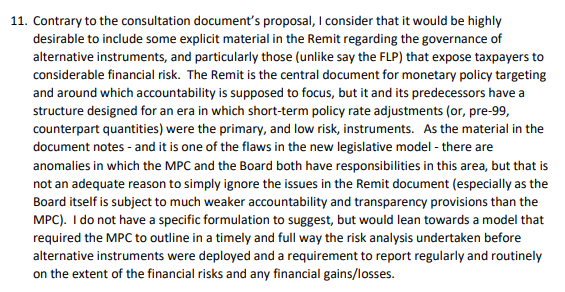

The consultation document addresses the question as to whether there should be text in the Remit around the governance of alternative policy instruments (like the – expensive and ineffective – LSAP). The Bank prefers not, but I reckon there is a pretty strong case, although the issue is complicated by the divided responsibilitities between the Bank’s Board – who know nothing about monetary policy – and the MPC. There is no easy solution, but the Remit is supposed to be the focal document for guiding monetary policy accountability.

On the composition and strcuture of the MPC there are several significant matters that can only be dealt with by amending legislation (I hope National is open to making some fixes) but I took the opportunity to lament again the blackball the Governor, Board and Minister have in place preventing anyone with current expertise in monetary policy or macroeconomic research/analysis from serving as an external MPC member, a decision that among other things cements the Governor’s continued dominance of the system (the Governor himself having only limited depth and authoritative expertise in such matters). But my main comments were about matters that are directly dealt with in the Charter and in the culture that has developed around the operation of the MPC since it was established.

If you felt inclined to make a late submission, the relevant email address is remit-review@rbnz.govt.nz