First thing this morning the Reserve Bank fronted up at Parliament’s Finance and Expenditure Committee for their Annual Review hearing.

The Governor kicked off with some introductory remarks that were celebratory (the focus of the hearing was notionally on the last financial year) but superficial. In some cases barely even honest. He was “very proud” of all the Bank had achieved, talked up monetary policy as having been “highly effective in preventing deflation”, claimed (wrongly) to have been one of the first central banks to have raised policy interest rates again, and ended with a paean to “diversity and inclusion” talking of having “many plans” and “much action” on that front. There was no mention, for example, of the $5 billion of taxpayers’ money they had lost, or of the continuing churn at the top of the organisation.

Last evening they had had to announce that two more senior managers were leaving, ousted in yet another of Orr’s restructurings. Orr didn’t deny the claim made by National’s Simon Bridges (and various journalists) that the Bank had hoped to keep these departures secret until after the hearing, and had only announced them late yesterday afternoon after the news had seeped out. It can be hard to keep track of all the departures – in several cases Orr can’t even blame his predecessors as at least two of the senior management departures have been of people who Orr had first promoted before changing tack and pushing them out. I’ll take the departure next year of the Bank’s long-serving CFO (who would be over 65) as a genuine retirement, but mostly the departures seem to have been Orr-initiated, such that of the large senior management group in place when he took office only 3.5 years ago, only two will soon be left.

And the departures aren’t simply in peripheral or support positions. Orr has now ousted two chief economists in succession, and we have no idea who will be filling that vacancy on the MPC, at a time when things are scarcely all quiet on the monetary policy front. On the financial stability side – largest part of the Bank and the growing bit – the gaps are even more obvious. The Deputy Governor (who ran that side of the Bank) is leaving, and now the two senior managers (heads of supervision and head of prudential policy/analysis) are leaving – the latter having already accepted a demotion a couple of years ago. Each of these guys has strengths and weaknesses (although I thought Andy Wood was good value), but all will be gone very shortly – and with them huge amounts of experience. In their place, we have a new Deputy Governor who has no background in banking, supervision or financial regulation, and two vacancies. So far at least, Orr has shown no ability to (or interest in doing so?) attract top-notch talent to the Bank at senior levels. And from 1 July next year, the Bank’s new Board is becoming the key decision-making body on prudential matters including policy. The Minister makes those appointments and so far no one whom one might think of as offering exceptional intellectual or practical leadership in these areas had been appointed. The Bank looks incredibly weak on that side of its business, and one wonders what their capable and experienced APRA counterparts make of it all.

But to return to this morning’s hearing, when Simon Bridges suggested that the volume of churn might almost be described as “reckless”, Orr’s only response was to suggest “or planned”. As Bridges noted the Bank was losing a lot of senior and experienced people, likely to be replaced with more junior less experienced people, perhaps “people who agree with you”. Bridges went on to comment on the number of people who had already got in touch with him to express concern at what was going on at the Bank. Orr offered no comment in response.

David Seymour also chipped in on this issue asking about turnover at senior levels. The Bank’s response seemed to be a mix of cute answers (people who had confirmed they were leaving shortly were nonetheless still there and so hadn’t left), obfuscation (emphasising how many more staff in total the Bank had – as if that too should not be a concern), and a bit of outright denial. Seymour asked Orr if he was “absolutely confident” that there was nothing about his (Orr’s) leadership that had led to conflicts resulting in departures”. Orr’s reply: “Absolutely”. I don’t suppose he was ever going to own up – the main who really hates being challenged or disagreed with – but it wasn’t a confidence-inspiring performance. And who is responsible for the Governor? Well, that would be the current ineffectual Board – whose chair has been carried over to the new and (legally) more powerful Board, and of course the Minister of Finance.

The Green Party’s Chloe Swarbrick also asked a couple of useful questions, and was simply fobbed off by Orr. Was there anything about the policy response over the last couple of years, she asked, that the Governor might have done differently with the benefit of hindsight? It was, she was told, a hypothetical that he wasn’t going to answer, but he then went on to say that he was “very confident” that “exactly the right decisions had been made”. With the benefit of hindsight, does any normal reflective human being make such bold claims? Well, Orr certainly does ($5bn of losses, as just one example, notwithstanding). Swarbrick went on to ask if there would be value in a review of Covid fiscal and monetary policy (a good idea, and a suggestion I’d also made to Treasury at a consultation session last week). Orr claimed that such reviews were ongoing and very transparent. If so, there is no evidence of it, and when someone reviews themself such reviews are often not received with total conviction.

David Seymour followed up, noting that the Governor had said earlier that house prices were above a “sustainable” level, employment was above the maximum sustainable level, and inflation was high and/or rising. Might it not be thought that the degree of monetary stimulus had been a bit overcooked?

Orr’s blustering response was that it was better than an alternative of extremely high unemployment and deflation, repeating his line that the Bank had been one of the first in the world to raise rates. Seymour pushed back and suggested some possibility of a middle ground – that, with hindsight, a bit less monetary stimulus might have been warranted, but Orr simply refused to engage.

There were no questions about the LSAP scheme ($5bn of losses notwithstanding) but National’s Andrew Bayly again asked about the Funding for Lending scheme. Crisis conditions have long passed, the OCR is working fine, and being raised, and yet the Bank keeps on for another year with the emergency facility that all else equal holds interest rates DOWN. The Assistant Governor burbled on about the need to provide certainty to banks – as if anything else about the economic (or virus) environment is certain. It is simply bizarre that emergency facilities are still providing stimulus, even as core inflation heads for top of the target range.

Not all the questions from non-Labour members was really to the point. As Orr noted, the MPC has to take the fiscal stance as given and adjust the OCR as required (having said that, National could point out that on occasion Orr has been an open cheerleader for bigger fiscal deficits), and National seems unable to decide whether it dislikes high inflation or a higher OCR more. Personally, I’m with the Governor on that one: high inflation needs to be brought back into check, and monetary policy is the most effective instrument. In fact, it was good to hear Assistant Governor Hawkesby explicitly note that inflation expectations had risen and that monetary policy was oriented towards getting inflation back to around the midpoint of the target range.

But two final questions are worth noting. A government member asked a patsy about the Bank’s climate change crusade, prompting National Andrew Bayly to note that the Federal Reserve of New York had recently published research suggested that climate change posed little threat to financial stability (he could have cited recent Bundesbank stress tests as well). Bayly asked if the Bank had done any modelling of its own. Orr’s response was an unequivocal “yes”. That was interesting because a quick check of the Bank’s climate change page showed that still the only “research” they listed was a single paper from 2018 which (“preliminary analysis”) also concluded that there wasn’t likely to be much to the climate change financial stability risk issue. You might have supposed that the Bank would be keen to get out in the public domain any research they’d done supporting the Governor’s ideological priors and political preferences. I have today lodged an OIA request for the modelling work the Governor was referring to this morning. On past form, we might see something six months from now.

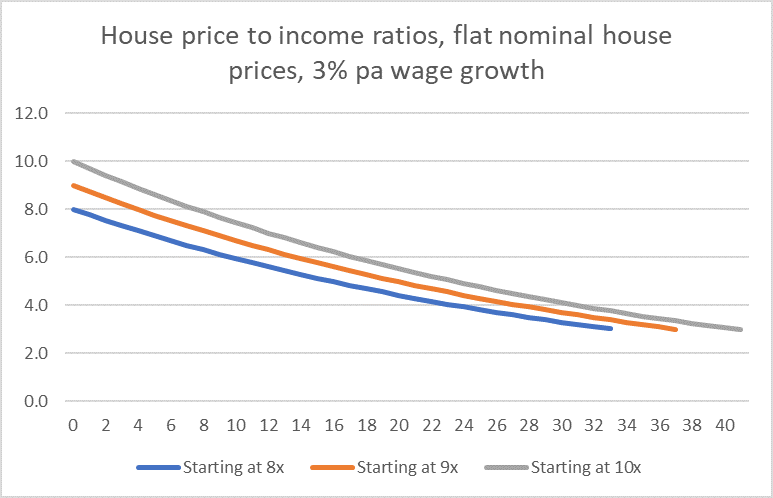

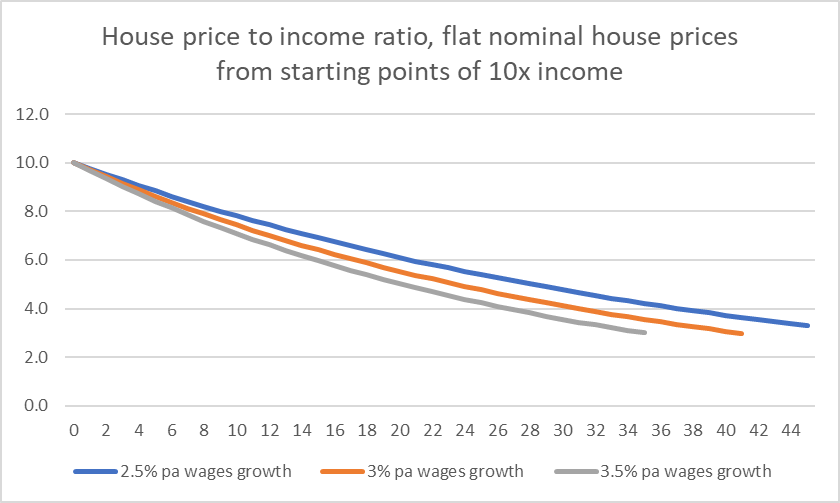

And then Chloe Swarbrick got in one last question. You’ll recall that the Governor had told the Committee that in the Bank’s view house prices were currently higher than “sustainable”. All else equal, Swarbrick asked, how much would house prices need to drop to be considered “sustainable”. Orr’s response was “I don’t have that number” (he had what looked like a dozen staff present in support). It seemed an eminently reasonable question. The Bank has the biggest team of macroeconomists in the country, it has in-house research capability and has claimed – not once but many times – that prices are “unsustainable”. The way places like the Bank work is that there will be a range of model estimates informing the judgement that current prices are unsustainable. It wasn’t that Orr didn’t have a number (or, more likely, a range) it was that he simply refused to answer, and did not suggest he would follow up and get back to the member.

A year ago, one might have said (I would have) that it really wasn’t an issue for the Bank. But the Minister changed the Bank’s Remit, and Orr and the MPC have embraced the change. You may, like me, think that they way they approach “sustainable” is meaningless and often misleading (their concept has nothing at all to do with longer-term fundamental supply characteristics) but…….they are the ones openly opining that prices are “unsustainable”. How much then, even as a range? Orr’s refusal to reply really made a mockery of parliamentary scrutiny.

Overall, it was good to see the Bank and the Governor facing some serious questions. 55 minutes for the whole thing, including government patsys, really wasn’t enough in the circumstances, but what we saw was a weak and unpersuasive central bank. The Reserve Bank is a key economic agency in New Zealand, exercising a great deal of discretionary power, and we (and Parliament) should expect a solid team of really capable and experienced senior people, articulating credible and thoughtful nuanced responses to serious questions and challenges. It wasn’t at all what we saw today. But of course, there is little follow through, and no serious questioning on these issues of either the Bank’s Board or the Minister of Finance. Instead we just see the continued degradation of yet another of New Zealand key public sector institutions. I suppose unserious governments – there is little sign they care much about institutions or medium-term economic performance, let alone getting house prices down – invite increasingly unserious bureaucracies, of which today’s Reserve Bank is one. Perhaps Orr will surprise and he’ll soon announce the appointment of a phalanx really strong capable independent-minded senior managers, who last (perhaps outlast him) but nothing about his tenure to date (or the continued churn) should give us – or Parliament- much confidence.