Over the last couple of weeks we’ve had another round of politicians (so-called “leaders”) doing their utmost to deny any interest in seeing house prices much lower. At 60 per cent below current levels – which would be readily achievable with open and competitive land markets, and a genuinely open and competitive building products sector – we’d be looking at something a lot more reasonable. Real rents would probably then be lower than ever before. But our politicians are terrified of the very idea.

The new Leader of the Opposition made clear his opposition to any suggestion of a sustained fall in house prices (while noting that inevitably there would be some ups and downs). HIs new deputy – and National’s housing spokesperson – did suggest that much lower house price/income ratios might be desirable, with something like flat nominal house prices. And while the Prime Minister at the weekend was quoting as suggesting that she wanted lower house prices – quite a change of tone from her, perhaps just getting ahead of what may already be beginning to happen – she too was at pains to deny any interest in much lower house prices.

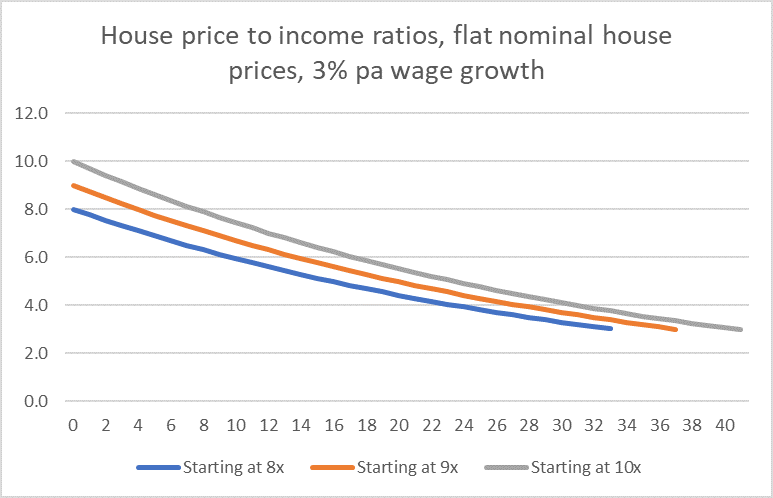

Of course, in principle, house price/income ratios could be steadily whittled away by some combination of flat nominal house prices and rising wage rate. But when one starts from such an unbalanced situation as New Zealand now does it would be the project of decades, even if anyone took it seriously. The great and good seem to rather like the idea of this “painless” whittling away, presumably as it enables them to sound serious, and not scary to the already-indebted.

Here is a chart of three scenarios, in each of which nominal house prices hold flat from here. In each scenario I’ve assumed 3 per cent annual growth in wage rates (basically inflation at target on average and something like 1 per cent per annum productivity growth). What differentiates the three scenarios is the starting point – a range from 8 times income to 10 times income.

At best, it takes 33 years for price/income ratios to get back to three – the sort of ratio seen in large chunks of the US, in cities large and small. At best, it would take almost a quarter of a century to get back to a price/income ratio of four.

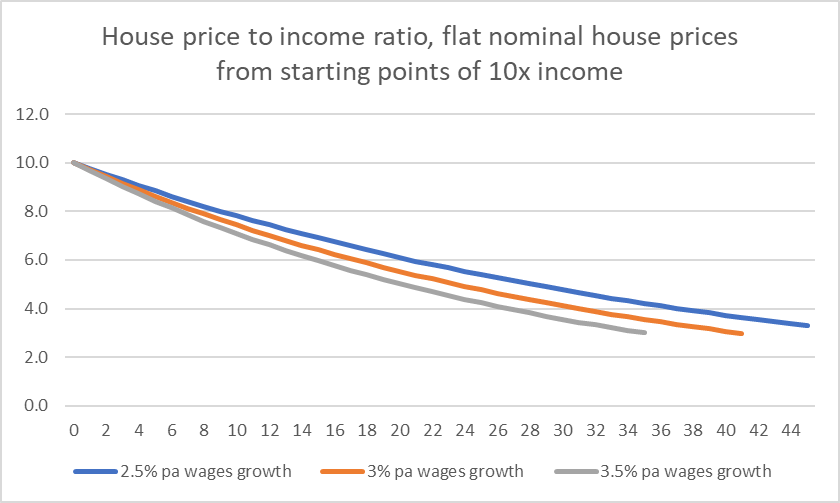

In the next chart I’ve assumed a starting point of 10 times income and shown the implications for a range of wage growth assumptions. On these scenarios, my kids would my age before house price to income ratios were again what they were when I was their age.

If your idea of political leadership is along the lines of “I must find where the people are going and get out in front of them”, I suppose I understand the apparent political terror at the prospect of much lower house prices, but what a pathetically weak approach, that abdicates any responsibility towards the next generation. These people – “leaders” of our political parties – appear content to get a whole other generation (or two) load up on debt based on house prices they know not to be based on any long-term fundamentals, rather than get to the heart of the issue now.

Of course, some in the media don’t help. I saw last night one journalist suggesting that even getting house prices 25 per cent lower would be reckless, irresponsible, and deeply economically damaging. But politicians put themselves forward, at least notionally, as leaders, people (allegedly) with the best interests of the country at heart. They are supposed to be the communicators, the coalition builders, the persuaders, the people who make things happen…..not those content to sit to the sidelines, idly hoping that well beyond their time in politics things might finally be sorted out.

Take the idea of a 25 per cent fall in house prices. That might take prices back to around where they were at the start of last year. No one who bought before then is put in any particular difficulty. And neither are most of those who bought more recently, as bank lending standards have not been loose, and LVR restrictions have become increasingly onerous. Some would be left temporarily with negative equity, but (a) typically not a large amount, and (b) in a fully-employed economy, modest negative equity isn’t typically a major problem (and to anyone going “easy for you to say”, it was exactly the situation I found myself in a couple of years after buying my first house). But our “leaders” can’t even enthusiastically embrace unwinding the last couple of years’ house price rises.

Of course, the major parties sometimes like to talk about the things they’ve done, up to and including the current amendment to the RMA being rushed through Parliament. But the proof of the pudding is in the prices, and expectations of future prices. Actually, in the political rhetoric as well. Not only have expectations of future house price inflation not gone negative – or even slowed noticeably after the latest “accord” – but the politicians’ own rhetoric reinforces the point: they themselves are scared of embracing lower prices.

Were they actually serious about fixing things, in their own terms of office, some creative thinking (and coalition building) might be required. Big changes in relative prices involve big shifts in wealth. Sharp rises in house prices have skewed the playing field away from the young and the poor. Sharp falls in house prices would skew things sharply away from the very highly-indebted. Of the latter, some don’t (and shouldn’t) command much sympathy at all. If you run a residential rentals business and took on huge amounts of debt to finance your business, well tough. It is a business, in this case built on systematically rigged markets (all that central and local government land-use regulation), and sometimes businesses fail. New entrants will emerge to replace you.

But first home buyers (in particular) command a lot more sympathy, and rightly so in my view. Young families didn’t ask the government to rig the market, or probably even support them doing so. They just want a secure home and backyard to raise their kids, and the only option governments left them for doing so was to pay these absurd price/income ratios, made barely feasible by the sustained decline in neutral interest rates (which in a functioning market should have made purchasing a home easier than ever). For them, some sort of partial compensation scheme might be a fair and necessary path to breaking through the political resistance to much-lower house and land prices. Not a first-best solution perhaps, but a great deal than putting another generation through this quite-unnecessary drama of rigged housing markets. When market prices are miles from the structural fundamentals, there is no merit in trying to foreshadow some very slow and allegedly “painless” adjustment. Better to get the prices (and market regulatory frameworks) sorted out now.

(Oh, and don’t be fooled if prices do fall back a bit over the next 12-18 months. Cyclical fluctuations happen. Falls happen (as over 2008/09). But without fixing the land-use restrictions – and the current RMA amendment does not even come close – the fundamental distortions remain. House prices did fall quite a bit in 2008/09 (even with much lower interest rates), until they rebounded to levels (and price/income ratios) higher than ever.