Over the last couple of weeks we’ve had another round of politicians (so-called “leaders”) doing their utmost to deny any interest in seeing house prices much lower. At 60 per cent below current levels – which would be readily achievable with open and competitive land markets, and a genuinely open and competitive building products sector – we’d be looking at something a lot more reasonable. Real rents would probably then be lower than ever before. But our politicians are terrified of the very idea.

The new Leader of the Opposition made clear his opposition to any suggestion of a sustained fall in house prices (while noting that inevitably there would be some ups and downs). HIs new deputy – and National’s housing spokesperson – did suggest that much lower house price/income ratios might be desirable, with something like flat nominal house prices. And while the Prime Minister at the weekend was quoting as suggesting that she wanted lower house prices – quite a change of tone from her, perhaps just getting ahead of what may already be beginning to happen – she too was at pains to deny any interest in much lower house prices.

Of course, in principle, house price/income ratios could be steadily whittled away by some combination of flat nominal house prices and rising wage rate. But when one starts from such an unbalanced situation as New Zealand now does it would be the project of decades, even if anyone took it seriously. The great and good seem to rather like the idea of this “painless” whittling away, presumably as it enables them to sound serious, and not scary to the already-indebted.

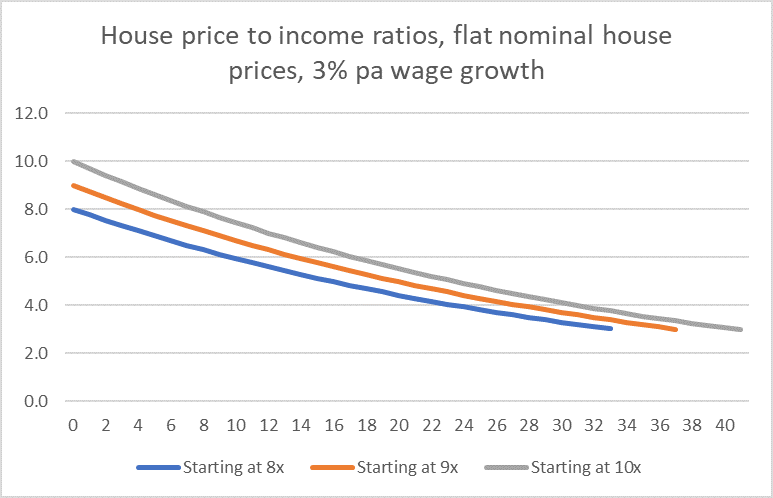

Here is a chart of three scenarios, in each of which nominal house prices hold flat from here. In each scenario I’ve assumed 3 per cent annual growth in wage rates (basically inflation at target on average and something like 1 per cent per annum productivity growth). What differentiates the three scenarios is the starting point – a range from 8 times income to 10 times income.

At best, it takes 33 years for price/income ratios to get back to three – the sort of ratio seen in large chunks of the US, in cities large and small. At best, it would take almost a quarter of a century to get back to a price/income ratio of four.

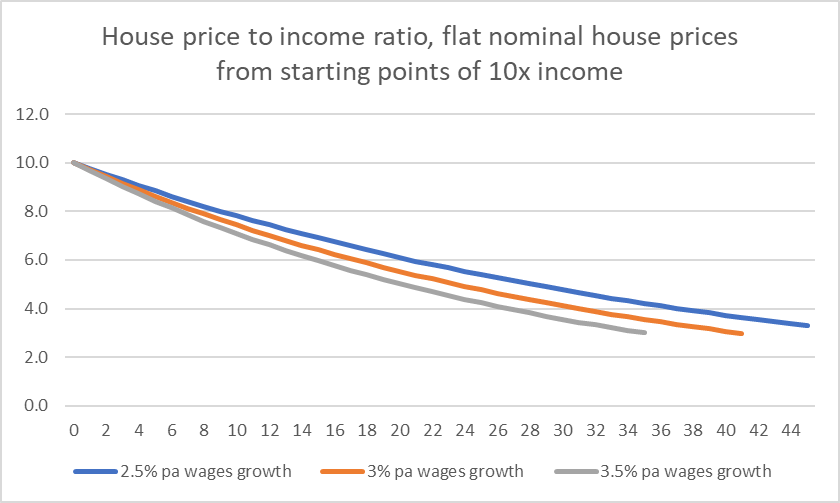

In the next chart I’ve assumed a starting point of 10 times income and shown the implications for a range of wage growth assumptions. On these scenarios, my kids would my age before house price to income ratios were again what they were when I was their age.

If your idea of political leadership is along the lines of “I must find where the people are going and get out in front of them”, I suppose I understand the apparent political terror at the prospect of much lower house prices, but what a pathetically weak approach, that abdicates any responsibility towards the next generation. These people – “leaders” of our political parties – appear content to get a whole other generation (or two) load up on debt based on house prices they know not to be based on any long-term fundamentals, rather than get to the heart of the issue now.

Of course, some in the media don’t help. I saw last night one journalist suggesting that even getting house prices 25 per cent lower would be reckless, irresponsible, and deeply economically damaging. But politicians put themselves forward, at least notionally, as leaders, people (allegedly) with the best interests of the country at heart. They are supposed to be the communicators, the coalition builders, the persuaders, the people who make things happen…..not those content to sit to the sidelines, idly hoping that well beyond their time in politics things might finally be sorted out.

Take the idea of a 25 per cent fall in house prices. That might take prices back to around where they were at the start of last year. No one who bought before then is put in any particular difficulty. And neither are most of those who bought more recently, as bank lending standards have not been loose, and LVR restrictions have become increasingly onerous. Some would be left temporarily with negative equity, but (a) typically not a large amount, and (b) in a fully-employed economy, modest negative equity isn’t typically a major problem (and to anyone going “easy for you to say”, it was exactly the situation I found myself in a couple of years after buying my first house). But our “leaders” can’t even enthusiastically embrace unwinding the last couple of years’ house price rises.

Of course, the major parties sometimes like to talk about the things they’ve done, up to and including the current amendment to the RMA being rushed through Parliament. But the proof of the pudding is in the prices, and expectations of future prices. Actually, in the political rhetoric as well. Not only have expectations of future house price inflation not gone negative – or even slowed noticeably after the latest “accord” – but the politicians’ own rhetoric reinforces the point: they themselves are scared of embracing lower prices.

Were they actually serious about fixing things, in their own terms of office, some creative thinking (and coalition building) might be required. Big changes in relative prices involve big shifts in wealth. Sharp rises in house prices have skewed the playing field away from the young and the poor. Sharp falls in house prices would skew things sharply away from the very highly-indebted. Of the latter, some don’t (and shouldn’t) command much sympathy at all. If you run a residential rentals business and took on huge amounts of debt to finance your business, well tough. It is a business, in this case built on systematically rigged markets (all that central and local government land-use regulation), and sometimes businesses fail. New entrants will emerge to replace you.

But first home buyers (in particular) command a lot more sympathy, and rightly so in my view. Young families didn’t ask the government to rig the market, or probably even support them doing so. They just want a secure home and backyard to raise their kids, and the only option governments left them for doing so was to pay these absurd price/income ratios, made barely feasible by the sustained decline in neutral interest rates (which in a functioning market should have made purchasing a home easier than ever). For them, some sort of partial compensation scheme might be a fair and necessary path to breaking through the political resistance to much-lower house and land prices. Not a first-best solution perhaps, but a great deal than putting another generation through this quite-unnecessary drama of rigged housing markets. When market prices are miles from the structural fundamentals, there is no merit in trying to foreshadow some very slow and allegedly “painless” adjustment. Better to get the prices (and market regulatory frameworks) sorted out now.

(Oh, and don’t be fooled if prices do fall back a bit over the next 12-18 months. Cyclical fluctuations happen. Falls happen (as over 2008/09). But without fixing the land-use restrictions – and the current RMA amendment does not even come close – the fundamental distortions remain. House prices did fall quite a bit in 2008/09 (even with much lower interest rates), until they rebounded to levels (and price/income ratios) higher than ever.

Only ****s and economists believe in eternal monotonic growth. There will be a crash in property prices.

My personal guess is that the trigger will be the exposure of governmental hubris by the spread of vaccine escape, hyper-transmissible Covid variants (of which Omicron is a foretaste).

LikeLiked by 1 person

Two big drivers of price are human reactions to stimulus and availability of finance, there are early signs of human reaction to Covid Mandates – worldwide protests and disrespecting the Elites and Politicians singing – you can stick your vaccine mandate up you a**e .When rather than if this spreads to other areas especially if a recession arrives the result are unpredictable but unlikely to be kind. Comments on popular blogs have moved through frustration-anger-hate and next is V*******. It seems that liquidity in the Banking sectors is being withdrawn on top of overt restrictions – LVI etc so at best property transactions will fall.

LikeLiked by 2 people

A wise column Michael, many thanks. If we want to really have a look at the inequalities in our society the housing market would be a great place to start. One would think that a socialist government would be dying to get it sorted, yeah right. Unfortunately the John Key government with the capacity to really do things fluffed about for 9 years and really fixed very little as well. Luxon/Seymour?

LikeLiked by 2 people

That is oft stated of Key’s govt, but I don’t think it is correct. House prices did not rise during Key’s first term (they weren’t fiddling while Rome burned) . They then rose sharply from about 2012-2016 and then slowed to a near stop, National didn’t know it was a problem at first, and then couldn’t build up building capacity as quick as was needed to head off the bubble.

What drove it was lack of building capacity post GFC and earthquakes and leaky house regulatory splurge much of the construction workforce left NZ due to GFC – the capacity was gone, and what was left were diverted to earthquake work and encumbered by huge productivity sapping increases in regulatory impost that halved (or worse) their productivity. During Nationals years in office the construction industry steadily ramped up from the very low point post GFC, but you can’t snap your fingers and expect an industry and trained workers to suddenly appear, growing capacity takes many years. For those years immigration far outstripped house building, leaving a supply deficit and prices shot up as a result.

LikeLiked by 2 people

Honestly it seems far too optimistic to assume that prices could go flat now. Ardern was saying earlier this year that prices were rising too quickly, but since then they went up 20% at least. It’s now at the point where I doubt prices could go up by less than 5% in any given year of this decade.

LikeLiked by 1 person

Whatever the trend there will inevitably be “noise” and fluctuations around it. I think falls are already getting underway, but it shldnt distract people from the fact that the underlying structural impediments to genuinely affordable housing haven’t really been addressed.

LikeLiked by 2 people

The only way that nominal prices will go up more than 5% per annum is if inflation is substantially greater than that. This may indeed be want the Ardern government wants (but dare not admit to wanting).

LikeLiked by 1 person

THankyou Michael…will forward far & wide. For the life of me I cannot understand the ‘eyes wide shut’ approach of the pollies, while finally starting to look vaguely concerned, and cannot forgive any of them. But then my peers have been like possums in the headlights too…you just want to scream. Then there’s our 20- something kids, who are a mix of nihilistic and stunned…and I marvel at why they don’t march in the streets. Forgive me lamenting all this again…covid don’t frighten me near as much as this, not new, scandal.

LikeLiked by 2 people

3 big technology trends that might impact the issue (and lead to sharp falls in particularly urban house prices)

1/ Telecommuting. Covid has shown that a big shift can happen, diminishing value of living in over-priced urban centres. We have glimpsed the possibilities, and there will be a likely steady increase in work-at-home due to lower costs and greater convenience, not yet clear how far it can go, but it could be a long way, eviscerating CBD’s and much of the raison d’etre of cities.

2/ Cheap ubiquitous personal air transport’. First technology offerings carrying passengers enter service in next year or two, but in 20 years they will be everywhere and cheap (think transition from 1900 cars to 1920 cars), and can travel 5x as far in the same time. There is no reason for them to be more expensive than cars once millions a year are being built. Living 100km from your workplace will be no problem, so living in overpriced suburbs will no longer be needed (or attractive)

3/ Roboticization/automation of house building, pace of improvement in industrial robots is incredible (and ultimately disruptive AI is inevitable in 1-6 decades, dooming all predictions). Most house building labour will soon be replaced and building cost will plummet. Eg check out what the (Zuru) Mowbrays are doing.

LikeLiked by 1 person

Interesting possibilities. I’m a bit less convinced of the difference 1 and 2 might make, since councils in whatever regions more people chose to settle in will typically have their own land-use restrictions, creating artificial scarcity in those places (think the Wairarapa towns north of Wgtn as examples). Time may tell, but we shouldn’t be waiting in hope or another generation may yet pass with high or higher prices, underpinned by existing land use restrictions.

LikeLiked by 1 person

As usual a nice commentary Michael.

Thank God New Zealand has one economic commentator who isn’t afraid to say it like it is and doesn’t suffer massive conflict of interest.

I did a similar analysis to this back in 2016 and came away with the same conclusion you have; even under some fairly benign assumptions, a period of stability is not only insufficient to restore New Zealand house price-to-income ratio’s back to their historical averages, they aren’t even realistic to restore them to a level where First Home Buyers (FHBs) can work themselves into a home. It will take decades to converge back to the long-term average and FHB serviceability is going to remain a big issue.

Grant Robertson says buyers need to ‘cut their cloth’ but it is quite clear he doesn’t understand the issue of serviceability (the flipside of affordability). To me, as a former banker, serviceability is what matters. Issues of serviceability almost invariably lead to issues of solvency and while the banking system is robust to even a large drop in prices, FHB’s are horribly exposed. I recently published a note to my clients looking at debt serviceability for FHB’s in Auckland and the results were alarming. Even assuming an income >20% above the average household income, a LVR of 80% and a DTI of 6x, and assuming that FHB’s are on interest-only mortgages, FHB’s face significant serviceability issues at current interest rates, which will likely be exacerbated as interest rates continue to rise. Much of their income is swallowed up by inelastic expenses (tax, kiwisaver, local authority rates, house insurance) or components of spending that are highly inelastic (e.g. food, clothing, transport, utilities) and so the discretionary component of their budget – the part that Grant thinks can be ‘cut’ is absolutely minimal. And that’s on a generous assumption on income and deposit. Someone commented “well, it’s always difficult, check out what it looked like in December 2007” so I did, and the situation isn’t even close to as bad as it is today… night and day.

If house prices stay stable for 10-years as the Government would like, these FHB’s on IO mortgages don’t build any equity and are essentially renting…

LikeLiked by 3 people

What a mess NZ would be in if it takes 30 years to get back to some semblance of affordability. I think the focus should go off house prices and onto rental market regulation. I tested a weekly rent maximum formula approach that would apply universally (i.e., to all rentals) to avoid the unintended consequences seen overseas with rent controls. The formula being:

Weekly rent maxima = (CV/1000) – x%

With the variable ‘x’ set on a city/regional basis such that the lower third of capital values in the area equate to a 30% of median household income in the area. Tested for the Hutt Valley over a 6 week period of rental listings, also noting the date of sale and price paid by the rental property owner. As CVs are three years old in the Hutt at the moment, x = 0% to get to that 30% of weekly median household income in the Hutt for the low end of the market.

Assuming with revaluation, capital values increase say, 30% over the period – the reset weekly rent maxima formula for the Hutt would be:

(CV/1000) – 30%.

The really interesting thing about the sample test is that probably two-thirds of the low end houses charging at that time, on average 50-60% of median household income for the area, were purchased by their owners well over 10 years ago – and you can imagine the whale of a profit (as opposed to yield) being made on those rental properties.

Good thing about regulation of the rental market with a formula such as this is that house prices don’t need to fall as a means to achieve rent affordability – CVs can rise based on the market of sales given the regulation simply adjusts the variable on revaluation to maintain the affordability equation.

One could couple the formula based approach with a maximum rent rise of CPI on an annual basis.

LikeLiked by 1 person

Interesting perspectives as ever Katharine.

LikeLike

Thanks – lol. It took me near on three years suggesting that they should raise the eligibility to purchase tobacco products by one year every year (in my opinion the only way to become smoke-free is not to grow new addicts!). So I’m heartened that someday, someone might listen! Meantime motels fill up, the statehouse waitlist grows and grows, and accommodation supplements do as well. Madness.

LikeLike

PS – once the weekly rent maxima is introduced – accommodation supplements can cease.

LikeLiked by 1 person

The economic and legal problem and its solution seems to be clear – the problem is political and so the interesting question is, what can be done about this, politically? Of the four serious parties, none offer any hope even if they probably all privately wish things weren’t like they are (no one would subscribe any longer to John Key’s argument that house prices are rising astronomically because NZ is doing so well and is popular).

Labour and National appear similar on this with National being slightly more compromised by virtue of its traditional voter demographics (more likely to be home owners or property investors). But in reality Labour isn’t really much different – these are the voters the big parties have to win in order to get a decent share of the vote. And Labour evidently favours market interventions of a (what they perceive to be) Scandanavian flavour – higher density housing and life long renting (and thus dependency on the state to protect a tenant’s “rights”).

The Greens and ACT are the same, just amplified. The disappointment is probably ACT given its stated market liberal values, but it’s recent growth is just down to absorbing ex-NZ First voters, who are only more likely to be pitiless, self satisfied mum and dad property investors who think young people are just too feckless to save for a house deposit.

The answer is that NZ desperately needs a special “Reduce Residential Property Prices” party – I think it would be easy to set up (there are no shortage of educated and articulate candidates out there (looking at you Mr Reddell) and would attract a decent amount of support, enough to become king makers in a future government. Perhaps even if it didn’t gain seats in parliament it could exert enough of a gravitational pull in the debate to shift the focus towards parties having to commit to steps to lower prices.

I see some parallels to a party like UKIP in the UK, during the last fifteen or so years leading up to Brexit. Whatever you might think of it, the party as a political campaign was fantastically successful. Only ever won one or two seats (in an FPP environment – its actual support was higher) but achieved what it set out to. Like Brexit, solving NZs property prices can involve a fairly “broad church” of adherents – there are multiple factors driving the prices and not everyone who wants to a return to sane prices will agree on the solution. The policy platform would need to be along the lines of the government committing to some kind of well financed independent investigation aiming to develop a solution to reduce prices to 3x income inside 15 years, with a further commitment to implement whatever recommendations come out of that within 3 months …

LikeLiked by 1 person

Interesting idea. Really needs someone with really good comms skills, backed by some smart policy people. I often cite the role Bob Jones played in the 83/84 campaign and election – really good speaker, with plenty of money to back him, helping ensure the decisive National defeat, while not himself getting elected.

I have pondered standing for the city council next year (altho if I did it would be for a bit of a platform, with no expectation that in one of the most left-liberal parts of the country (hating “sprawl”) I could get more than a few dozen votes.

LikeLike

Please do Michael and also ask for some sense with public transport – use the Snapper data to show where and when buses are actually being used.

Where available buses aren’t being used then get some sort of sponsored Uber service to replace them. More services, more often are largely not the answer to get people out of their cars outside of peak hours – which itself is a misguided aim!

LikeLike

I left NZ a few years ago, partly due to crazy house prices, partly due to marrying a Brit. Sometimes I wistfully hope to return, but I can’t see it happening at these sorts of prices. If I returned, I would have to take on loads more debt, at much higher interest rates, whilst earning a lower salary and being taxed more, with everything being more expensive. Any young person with half a brain must be able to see how they are being cheated out of having a reasonable life – its horrendous.

I think a lot of kiwis end up leaving rather than protesting, which perhaps explains the apparent apathy amongst younger people. The thing with leaving is that it is guaranteed to change your life and situation; protesting is not.

LikeLiked by 1 person

Sobering perspective thanks. Two of my kids have foreign passports and as they approach adulthood I (sadly) encourage them to think about leaving, so dreadful are NZ house prices (and NZ’;s long-tern productivity performance).

LikeLike

Seems hard for house prices to turn. Underwriting standards haven’t weakened (anecdotally – which includes allowance for mortgage rate increases) and debt servicing, on average, doesn’t seem to be an issue given the employment trend. And culturally, a NZer would likely do everything to retain a house before handing over the keys.

If mortgage rates do rise further than expected, maybe there will be a problem but the BIS ‘debt trap’ argument is a hard one to ignore.

On that, is there any reason why the NZ mortage market is dominated by short dated fixed rates vs floating option? Europe seems mainly floating while the US has the 30yr? Is it manly a market history or framework set up? Has the RBNZ ever done research on this?

LikeLike

The US is mostly fixed-rate mortgages because of the historical role of the government-sponsored mortgage agencies (state intervention in the housing finance market). In Denmark, long-term fixed rates are also important. Interesting to wonder why the two models have not converged over time, but (eg) in NZ banks would happily offer longer-term fixed rate mortgages (albeit with significant break penalties) but they have never been many takers for those on offer.

LikeLike

What effect has the decreased mortality seen in New Zealand since the beginning of the pandemic on housing supply and so prices?

The all cause mortality rate has dropped by approximately 11% from the first lockdown in 2020. Not entirely certain why, but presumably a contributor is the virtual absence of seasonal influenza in the winters of 2020 and 2021.

This must have had the effect of a slowing of the rate of homes of the deceased coming on to the market.

It won’t last for ever. Deaths have been delayed, not prevented. Expect a catch up “Boomer Die-off” in a coming winter.

LikeLike

Offset of course by the halt to immigration (indeed, a net outflow from NZ for the last 18 mths)

LikeLike

[…] Reddell’s updated analysis of housing costs in New Zealand, especially in relation to incomes and Price/income ratios, with the key […]

LikeLike

[…] All of contributing to this insanity: […]

LikeLike