The CPI for the December quarter was finally released yesterday – even later in the month than that other CPI laggard the ABS. The picture wasn’t pretty, even if at this point not particularly surprising. My focus is on the sectoral factor model measure of core inflation – long the Reserve Bank’s favourite – and if, as my resident economics student says “but Dad, no one else seem to mention it”, well too bad. Of the range of indicators on offer it is the most useful if one is thinking about monetary policy, past and present.

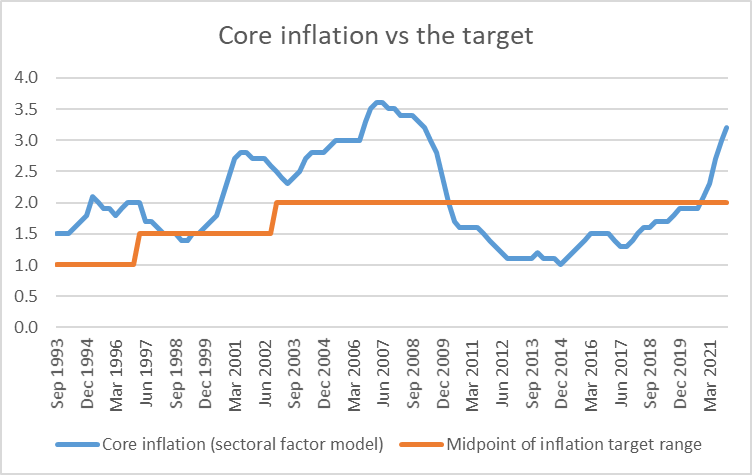

Factor models like this provide imprecise reads (subject to revision) for the most recent periods – that’s what you’d expect, especially when things are moving a lot, as the model is looking to identify something like the underlying trend. The most recent observations were revised up yesterday, and the estimate for core inflation for the year to December 2021 was 3.2 per cent. That is outside the 1-3 per cent target range (itself specified in headline terms, although no one ever expected headline would stay in the range all the time).

It is less than ideal. It is a clear forecasting failure – which would be even more visible if we show on the same chart forecasts from 12-18 months ago.

But…it isn’t unprecedented. In 28 years of data, this is the third really sharp shift in the rate of core inflation – although both were in periods before this particular measure was developed. And, at least on this measure, at present core inflation is still a bit below the 3.6 per cent peak in 2007, or the 3.5 per cent the annual inflation rate averaged for a year or more in 2006 and 2007.

What perhaps does stand out is how little monetary policy has yet done, how slow to the party the Bank has been. Over 1999 to 2001, the OCR was raised 200 basis points. From 2004 to 2007, the OCR was raised 300 points. And as core inflation fell sharply from late 2008, the OCR was cuts by 575 basis points.

So far this time the OCR has been increased by 50 basis points, and is not even back to pre-Covid levels – even though, on this measure, core inflation never actually dipped in 2020. I refuse to criticise the Reserve Bank for misreading 2020 – apart from anything else they were in good company as forecasters – but their passivity in recent months is much harder to defend.

The sectoral factor model measure is itself made up of two components. Here they are

Because the model looks for trends, the big moves in this measure of core tradables inflation have often reflected the big swings in the exchange rate – which affects pretty much all import prices – but this time there has been no such swing. Just a lot more generalised inflation from abroad (as well as the one-offs that this model looks to winnow out). So a lot more (generalised) inflation from abroad – not something to discount – and a lot more arising from domestic developments (demand, capacity pressures, and perhaps some expectations effects too). It is a generalised issue – above target, and probably rising further (both from the momentum in the series, and continued tight labour markets and rising inflation norms).

The headline inflation number gets media and political attention it doesn’t really warrant. Headline inflation is volatile, and even if in principle it might be more controllable than what we see, it usually would not make economic sense to control it more tightly. For that reason, in 30+ years of inflation targeting it has never been the policy focus.

And to the extent that wage inflation fluctuates with price inflation, the relationship is much closer with core inflation (we’ll get new wages data next week, and most likely the annual wage inflation will have risen a bit further).

It is worth noting – for all the headlines – that in every single year of the last 25, wage inflation has run ahead of core (price) inflation. As it has continued to do even over the last year. That is what one would expect – productivity growth and all that – even if the economy were just growing steadily with the labour market near full employment.

It is true that the gap between wage and price (core) inflation is unusually narrow at present

Perhaps the gap will widen again over the coming year – overfull employment and all that – but bear in mind that true economywide productivity growth is probably atrociously (partly unavoidably) low at present, so the sustainable rate of real wage growth is also less than it was.

(None of this means wage earners aren’t now earning less per hour in real terms than they were a year ago, but that drop is, to a very considerable extent, unavoidable. The gap between headline and core inflation is typically about things that have made us poorer, for any given amount of labour supply.)

What does all this mean for policy? First, for all the criticism – often legitimate – of wasteful and undisciplined government spending over the last two years – core inflation is primarily a monetary policy issue, and sustained core inflation above target is a monetary policy failure. The government is ultimately accountable for monetary policy too, but if what we care about is keeping inflation in check, it is the Bank and the MPC that should primarily be in the frame, not fiscal policy. Monetary policymakers have to take fiscal policy – just like private behaviour/preferences – as given.

To me, the recent data confirms again that the Reserve Bank was far to slow to pivot, and far too sluggish when they eventually did. They are behind the game, as was clear even by November before they – like the government, but even longer – went for their long summer holiday in the midst of a fast-developing situation. It is pretty inexcusable that we will go for three months with not a word from the MPC, even as inflation has surged in an overheating economy.

What disconcerts me a bit is the apparent complacency even in parts of the private sector. (If I pick on the ANZ here it is only because they put out a particularly full and clear articulation of their story quite recently). As an example, ANZ had a piece out last week suggesting that the OCR would/should go to 3 per cent by about April next year, but that this would/should be accomplished with a steady series of 25 basis point adjustments. I’m also hesitant about making calls about where the OCR might be any considerable distance into the future (and in fairness they do highlight some of the uncertainties) but if you are going to make a central-view call like that most people might suppose it was consistent with a gradual escalation of capacity pressures, gradually leaned against with policy. But on their own description, the economic growth outlook over the next year doesn’t look spectacular at all – the word “insipid” even appeared – while the pressures (inflation and capacity) seem very real right now, in data that (at best) lags slightly. Core inflation has (unexpectedly) burst out of the target range, the economy is overheated, inflation expectations have risen (even in the last RB survey the two-year ahead measure was 2.96 per cent – up 90 points in six months, when the OCR has risen only 50 points. ANZ’s economists did address the possibility of a 50 basis point increase next month. They seemed to think it unlikely, because no ground has been prepared. They may well be right about that – and that may be what their clients care about – but, as advisers, they seemed unbothered about it. Why not urge the Bank to get out now and prepare the ground for next month’s review? Why not thrown caution to the wind and suggest the world wouldn’t end if the MPC actually took the market by surprise and took actions that increased the changes of keeping inflation in check? Based on what we know now, the economy would be better off if the Bank raised the OCR by 50 basis points next month (and sold some of that money-losing bond stockpile) and suggested it would be prepared to do the same again in April if the data warranted.

What difference does is make? The big risk right now is that people come to think that a normal inflation rate isn’t something near 2 per cent, but something near 3 per cent (or worse). If that happens – and no single survey will tell the story – it will take a lot more monetary policy adjustment (and lost output) at some point to bring things back to earth, all else equal. And whereas we have no real idea what monetary policy should be in the middle of next year, it is quite clear that considerably tighter conditions are warranted now, and that the Bank so far has not even kept up with the slippage in inflation and expectations.

What about Covid? By 23 February when the MPC descends from the mountain top, it seems likely that we might be nearing the peak of the unfolding Omicron wave. Experience abroad suggests that even when the government doesn’t simply mandate it, a lot of people will be staying at home, a lot of spending won’t be happening. Who knows – and we may hope not – MPC members themselves, or their advisers, may be sick and enfeebled. Tough as those weeks might be, they should not be an excuse for a reluctance to act decisively. MPC went slow last year, and to some extent now pays the price in lost optionality. Delay in August didn’t look costly then. Delay now looks really rather risky.

But who are we to look to for this action. As (core) inflation bursts out of the target band, and expectations of future inflation rise, we already have an enfeebled MPC, even pre Covid.

- We have a Governor who has given few serious speeches in his almost four years in office,

- A Deputy Governor who didn’t greatly impress when responsible for macro, and is now likely to be focused on learning his new job, and finding some subordinates after he and Orr restructured out his experienced senior managers before Christmas,

- We have a Chief Economist who has been restructured out, and on his final meeting. No doubt he’ll give it his best shot but….that wasn’t much over the three years he was in the job, including not a single speech,

- And we have the three externals, appointed more for their compliance than expertise, who’ve given not a single speech between them in three years, and two of them are weeks away from the expiry of their terms (and no news on whether they’ll be reappointed or replaced).

It was pretty uninspiring already, to meet a major policy, analytical and communications challenge. And then yesterday, the dumbing-down of the institution – exemplified in speeches (lack thereof) and the near-complete absence now of published research – continued, with the appointment of Karen Silk as the Assistant Governor (Orr’s deputy) responsible for matters macroeconomic and monetary policy. And this new appointee – who it seems may not be in place for February – seems to have precisely no background in, or experience of, macroeconomics and monetary policy at all (but apparently a degree in marketing) But she seems to be an ideological buddy of the Governor’s, heavily engaged in climate change stuff. Perhaps the superficial customer experience – pretty pictures etc – of the MPS will improve, but it is hard to imagine the substance of policy setting, policy analysis, and policy communications will. It was simply an extraordinary appointment – the sort of person one might expect to see if a bad minister were appointing his or her mates. And if this appointment was Orr’s, Robertson has signed off on it, in agreeing to appoint her to the Monetary Policy Committee. It would be laughably bad, except that it matters. How, for example, is the new Assistant Governor likely to find any seriously credible economist to take up the Chief Economist position even if – and the evidence doesn’t favour the hypothesis at present – she and Orr cared? Coming on top of all the previous senior management churn and low quality appointments it is almost as if Orr is now not vying for the title “Great team, best central bank”, but for worst advanced country bank. (It is hard to think of serious advanced country central bank, not totally under the political thumb – and rarely even then – who would have such a person as the senior deputy responsible for macroeconomic and monetary policy matters: contrast if you will places like the RBA, the ECB, the Bank of Canada, the Bank of England, and numerous others.)

I sat down this morning and filled in the Bank’s latest inflation expectations survey. For the first time – in the 6/7 years I’ve been doing it – I had to stop and think had about the questions about inflation five and ten years hence (I’ve typically just responded with a “2 per cent” answer – long time away, midpoint of the target, 10 years at least beyond Orr’s term). With core inflation high and rising, policy responses sluggish at best so far, and with the downward spiral in the quality of the MPC (and the lack of much serious research and analysis supporting them), how confident could I be about medium-term outcomes. Perhaps it is still most likely that eventually inflation is hauled back, that over time core inflation gets towards 2 per cent, with shocks either side. The rest of the world, after all, will still act as something of a check, no matter how poor our central bank becomes. But the decline and fall of the institution is a recipe for more mistakes, more volatility, more communications failures, and less insight, less analysis, and fewer grounds for confidence that the targets the Minister sets will consistently be delivered at least cost and dislocation. That should concern the Minister, but sadly there is no sign it – or any of the other straws in the wind of institutional decline – does.