The National Party, in particular, has been seeking to make the rate of inflation a key line of attack on the government. Headline annual CPI inflation was 5.9 per cent in the most recent release, and National has been running a line that government spending is to blame. It is never clear how much they think it is to blame – or even in what sense – but it must be to a considerable extent, assuming (as I do) that they are addressing the issue honestly.

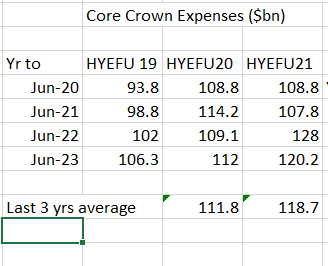

I’ve seen quite a bit of talk that government spending (core Crown expenses) is estimated to have risen by 68 per cent from the June 2017 year (last full year of the previous government) to the June 2022 year – numbers from the HYEFU published last December. That is quite a lot: in the previous five years, this measure of spending rose by only 11 per cent. Of course, what you won’t see mentioned is that government spending is forecast to drop by 6 per cent in the year to June 2023, consistent with the fact that there were large one-off outlays on account of lockdowns (2020 and 2021), not (forecast) to be repeated.

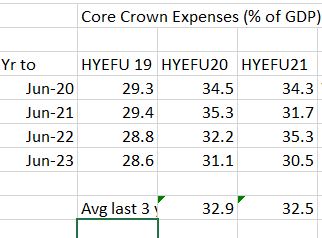

But there is no question but that government spending now accounts for a larger share of the economy than it did. Since inflation was just struggling to get up towards target pre-Covid, and I’m not really into partisan points-scoring, lets focus on the changes from the June 2019 year (last full pre-Covid period). Core Crown expenses were 28 per cent of GDP that year, and are projected to be 35.3 per cent this year, and 30.5 per cent in the year to June 2023 (nominal GDP is growing quite a bit). That isn’t a tiny change, but…..it is quite a lot smaller than the drop in government spending as a share of GDP from 2012 to 2017. I haven’t heard National MPs suggesting their government’s (lack of) spending was responsible for inflation undershooting over much of that decade – and nor should they because (a) fiscal plans are pretty transparent in New Zealand and (b) it is the responsibility of the Reserve Bank to respond to forecast spending (public and private) in a way that keeps inflation near target. The government is responsible for the Bank, of course, but the Bank is responsible for (the persistent bits of) inflation.

The genesis of this post was yesterday morning when my wife came upstairs and told me I was being quoted on Morning Report. The interviewer was pushing back on Luxon’s claim that government spending was to blame for high inflation, suggesting that I – who (words to the effect of) “wasn’t exactly a big fan of the government” – disagreed and believed that monetary policy was responsible. I presume the interviewer had in mind my post from a couple of weeks back, and I then tweeted out this extract

I haven’t taken a strong view on which factors contributed to the demand stimulus, but have been keen to stress the responsibility that falls on monetary policy to manage (core, systematic) inflation pressures, wherever they initially arise from. If there was a (macroeconomic policy) mistake, it rests – almost by definition, by statute – with the forecasting and policy setting of the Reserve Bank’s Monetary Policy Committee.

I haven’t seen any compelling piece of analysis from anyone (but most notably the Bank, whose job it is) unpicking the relative contributions of monetary and fiscal policy in getting us to the point where core inflation was so high and there was a consensus monetary policy adjustment was required. Nor, I think, has there been any really good analysis of why things that were widely expected in 2020 just never came to pass (eg personally I’m still surprised that amid the huge uncertainty around Covid, the border etc, business investment has held up as much as it has). Were the forecasts the government had available to it in 2020 from The Treasury and the Reserve Bank simply incompetently done or the best that could realistically have been done at the time?

Standard analytical indicators often don’t help much. This, for example, is the fiscal impulse measure from the HYEFU, which shows huge year to year fluctuations over the Covid and (assumed) aftermath period. Did fiscal policy go crazy in the year to June 2020? Well, not really, but we had huge wage subsidy outlays in the last few months of that year – despite which (and desirably as a matter of Covid policy at the time) GDP fell sharply. What was happening was income replacement for people unable to work because of the effects of the lockdowns. And no one much – certainly not the National Party – thinks that was a mistake. In the year to June 2021, a big negative fiscal impulse shows, simply because in contrast to the previous year there were no big lockdowns and associated huge outlays. And then we had late 2021’s lockdowns. And for 2022/23 no such events are forecast.

One can’t really say – in much of a meaningful way – that fiscal policy swung from being highly inflationary to highly disinflationary, wash and repeat. Instead, some mix of the virus, public reactions to it, and the policy restrictions periodically materially impeded the economy’s capacity to supply (to some unknowable extent even in the lightest restrictions period potential real GDP per capita is probably lower than otherwise too). The government provided partial income replacement, such that incomes fell by less than potential output. As the restrictions came off, the supply restrictions abated – and the government was no longer pumping out income support – but effective demand (itself constrained in the restrictions period) bounced back even more strongly.

Now, not all of the additional government spending has been of that fairly-uncontroversial type. Or even the things – running MIQ, vaccine rollouts – that were integral to the Covid response itself And we can all cite examples of wasteful spending, or things done under a Covid logo that really had nothing whatever to do with Covid responses. But most, in the scheme of things, were relatively small.

This chart shows The Treasury’s latest attempt at a structural balance estimate (the dotted line).

In the scheme of things (a) the deficits are pretty small, and (b) they don’t move around that much. If big and persistent structural deficits were your concern then – if this estimation is even roughly right – the first half of last decade was a much bigger issues. And recall that the persistent increase in government spending wasn’t that large by historical standards, wasn’t badly-telegraphed (to the Bank), and should have been something the Bank was readily able to have handled (keeping core inflation inside the target range).

The bottom line is that there was a forecasting mistake: not by ministers or the Labour Party, but by (a) The Treasury, and (b) the Reserve Bank and its monetary policy committee. Go back and check the macro forecasts in late 2020. The forecasters at the official agencies basically knew what fiscal policy was, even recognised the possibility of future lockdowns (and future income support), and they got the inflation and unemployment outlook quite wrong. They had lots of resources and so should have done better, but their forecasts weren’t extreme outliers (and they didn’t then seem wildly implausible to me). They knew about the supply constraints, they knew about the income support, they even knew that the world economy was going to be grappling with Covid for some time. Consistent with that, for much of 2020 inflation expectations – market prices or surveys – had been falling, even though people knew a fair amount about what monetary and fiscal policy were doing. In real terms, through much of that year, the OCR had barely fallen at all. It was all known, but the experts got things wrong.

Quite why they did still isn’t sufficiently clear. But, and it is only fair to recognise this, the (large) mistake made here seems to have been one repeated in a bunch of other countries, where resource pressures (and core inflation) have become evident much more strongly and quickly than most serious analysts had thought likely (or, looking at market prices, than markets themselves had expected). Some of that mistake was welcome – getting unemployment back down again was a great success, and inflation in too many countries had been below target for too long – so central banks had some buffer. But it has become most unwelcome, and central banks have been too slow to pivot and to reverse themselves.

Not only have the Opposition parties here been trying to blame government spending, but they have been trying to tie it to the 5.9 per cent headline inflation outcome. I suppose I understand the short-term politics of that, and if you are polling as badly as National was, perhaps you need some quick wins, any wins. But it doesn’t make much analytical sense, and actually enables the government to push back more than they really should be able to. Because no serious analyst thinks that either the government or the Reserve Bank is “to blame” for the full 5.9 per cent – the supply chain disruption effects etc are real, and to the extent they raise prices it is pretty basic economics for monetary policy to “look through” such exogenous factors. It seems unlikely those particular factors will be in play when we turn out to vote next year.

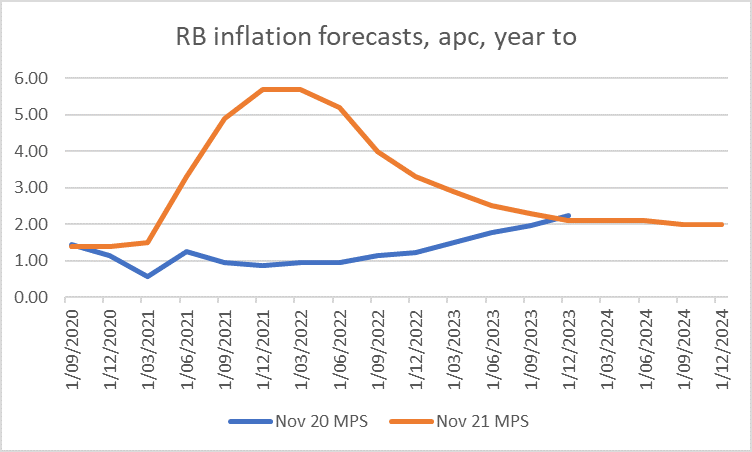

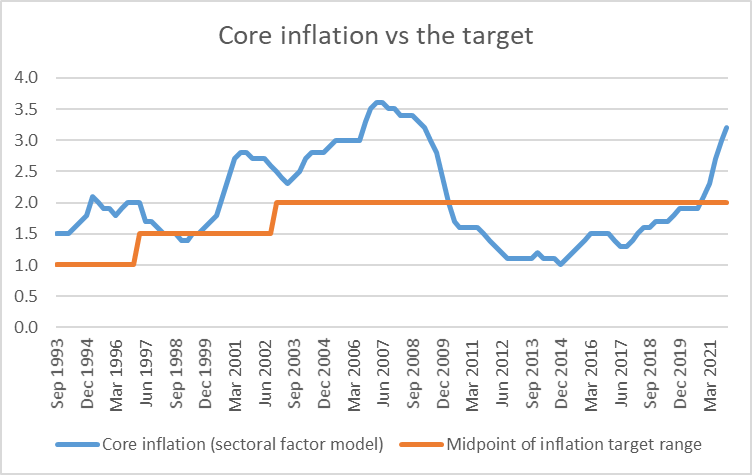

Core inflation not so much – indeed, the Bank’s sectoral core factor model measure is designed to look for the persistent components across the whole range of price increases, filtering out the high profile but idiosyncratic changes. Those measures have also risen strongly and now are above the top of the target range. That inflation is what NZ macro policy can, and should, do something about. But based on those measures – and their forecasts – the Reserve Bank has been too slow to act: the OCR today is still below where it was before Covid struck, even as core inflation and inflation expectations are way higher. Conventional measures of monetary policy stimulus suggest more fuel thrown on the fire now than was the case two years ago.

When I thought about writing this post, I thought about unpicking a series of parliamentary questions and answers from yesterday on inflation. I won’t, but suffice to say neither the Minister of Finance, the Prime Minister, the Leader of the Opposition, or Simon Bridges or David Seymour emerged with much credit – at least for the evident command of the analytical and policy issues. There was simply no mention of monetary policy, of the Reserve Bank, of the Monetary Policy Committee, or (notably) the government’s legal responsibility to ensure that the Bank has been doing its job. It clearly hasn’t (or core inflation would not have gotten away on them to the extent it has). I suppose it is awkward for the politicians – who wants to be seen championing higher interest rates? – and yet that is the route to getting inflation back down, and the sooner action is taken the less the total action required is likely to be. With (core) inflation bursting out the top of the range, perhaps with further to go, the Bank haemorrhaging senior staff, the recent recruitment of a deputy chief executive for macro and monetary policy with no experience, expertise, or credibility in that area, it would seem a pretty open line of attack. Geeky? For sure? But it is where the real responsibility rests – with the Bank, and with the man to whom they are accountable, who appoints the Board and MPC members? There is some real government responsibility here, but it isn’t mainly about fiscal policy (wasteful as some spending items are, inefficient as some tax grabs are), but about institutional decline, and (core) inflation outcomes that have become quite troubling.

Since I started writing this post, an interview by Bloomberg with Luxon has appeared. In that interview Luxon declares that a National government would amend the Act to reinstate a single focus on price stability. I don’t particularly support that proposal – it was a concern of National in 2018 – but it is of no substantive relevance. Even the Governor has gone on record saying that in the environment of the last couple of years – when they forecast both inflation and employment to be very weak – he didn’t think monetary policy was run any differently than it would have been under the old mandate. That too is pretty basic macroeconomics. It is good that the Leader of the Opposition has begun to talk a bit about monetary policy, but he needs to train his fire where it belongs – on the Governor – not, as he did before Christmas, forcing Simon Bridges to walk back a comment casting doubt on whether National would support Orr being reappointed next year. In normal times, you would hope politicians wouldn’t need to comment much on central bankers at all. But the macro outcomes (notably inflation), and Orr’s approach on a whole manner of issues (including the ever-mounting LSAP losses) suggest these are far from normal times. Core inflation could and should be in the target range. It is a failure of the Reserve Bank that it is not, and that – to date – nothing energetic has been done in response.