I don’t have too much to say about yesterday’s HYEFU, but two things caught my eye.

The first was a bit of attention on the $6 billion “operating allowance” the government has given itself to increase spending (or, I suppose, cut taxes) at next year’s Budget. It is a big number, but it doesn’t mean a great deal. In principle, the operating allowance covers things where the government has some discretion (whereas, by legislation, tax revenue tends to rise each year as nominal GDP does, and welfare benefits rise each year as inflation/wages do, and without new legislation the government of the day has no choice in the matter).

But governments tend to care about purchasing/delivering real goods and services, and they need actual people to work for them. And when there is inflation, the dollar cost of purchasing goods, services, and labour tends to rise. Governments don’t have to – and tend not to – compensate agencies/votes for inflation each and every year but when inflation is higher, over time more dollars need to be allocated for increased spending just to keep the real volume as the government intended. And since inflation – in principle – just blows up prices and incomes, making us as a whole neither richer nor poorer, they can do so with no particularly ill effects.

To illustrate, suppose the government spends $100 billion a year in an economy with nominal GDP of $330 billion (so roughly 30 per cent of GDP). Now assume that prices generally suddenly rise by 5 per cent, with nothing else changing. The things the government wants to purchase cost more, but its tax revenue also rises by more. In fact, it will now cost $5 billion more than otherwise to purchase the same volume of goods, services, labour (or real transfers). In practice, as noted above, quite a bit of government spending is indexed by legislation (roughly a third of core Crown spending is on welfare) and so not covered by the operating allowance. But in this scenario a 5 per cent lift in prices might require a $3.3 billion operating allowance, just to keep real government purchases unchanged.

I don’t have the time today or the patience to try to reconcile all the numbers, but to illustrate that inflation is a big part of the picture note that in this year’s Budget Treasury forecast that inflation for the year to June 2021 would be 2.4 per cent, for the year to June 2022 1.7 per cent, and for the year to June 2023 1.8 per cent. In the HYEFU, those numbers (2021 now known) are 3.3 per cent, 5.1 per cent, and 3.1 per cent. The total increase in the price level over those three years was expected to be 6.0 per cent, and is now expected to be 11.9 per cent. So of course the government needs to put more money (quite a lot more) in the operating allowance just to maintain real spending at the levels they intended only a few months ago. A lot of it is simply an inflation illusion. In the same way that a very small operating allowance would reveal nothing about the fiscal stance if inflation was to be unexpectedly low (as it was, say, a decade ago).

Don’t take it from me. Here are The Treasury’s forecasts of core Crown operating expenses as a per cent of GDP, including the government’s fiscal plans (those “big” operating allowances) as communicated to them and published yesterday.

On these plans, core Crown spending as a share of GDP will be around the same share of the economy as it was going into John Key’s final term.

There is plenty to criticise about individual spending items under this government – take $51 million wasted on the aborted, always ludicrous, Auckland walking bridge, let alone $5 billion in Reserve Bank losses – but the bottom line at this stage is one in which total spending ends up much where it was as a share of GDP. One might, of course, worry more about timing. With an overheated economy (on Treasury and Reserve Bank numbers), with high and rising inflation, and with a high terms of trade, the government really should be running a surplus next year (headline surplus consistent with cyclically-adjusted balance. But, in fairness, the forecast deficit for 2022/23 is small.

As noted, there has been – and is expected to be – quite a bit more inflation. Like the Reserve Bank, Treasury now seems to think that even core inflation will move outside the top of the target band the government set for inflation. They expect 3.1 per cent inflation in the year to June 2023 – ages away, and fully within the control of monetary policy now – and won’t be forecasting the sorts of one-off price shocks that often distort near-term headline inflation forecasts.

But, on the Treasury’s numbers it doesn’t seem like anything to worry about because by the end of the forecast period (June 2025) inflation is back to 2.2 per cent, basically the midpoint of the target range.

But how is this being achieved? Sure, they expect the Reserve Bank to raise the OCR, to a peak of 3.2 per cent by June 2023. But raising the OCR above neutral – as the Governor told us they expect to – usually dampens (core) inflation mostly by generating some temporary excess capacity in the economy.

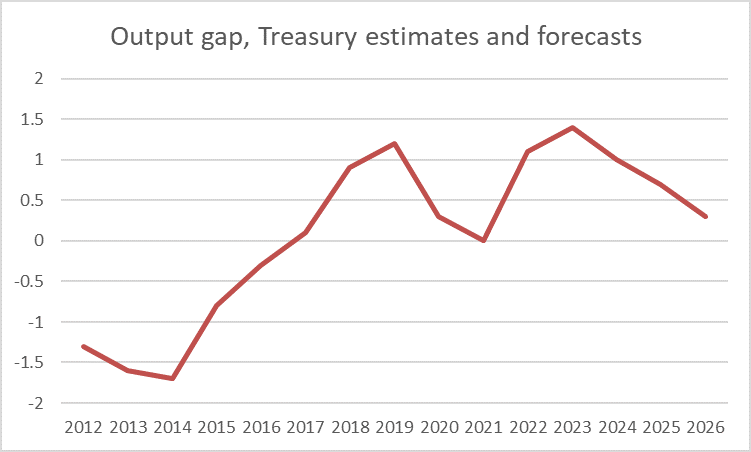

But here is The Treasury’s view on the output gap.

They reckon it was deeply negative a decade ago, when core inflation was low and falling (reaching a trough around the end of 2014), but now they reckon it will be positive – quite materially so for the next couple of years – throughout the forecast horizon. All else equal, that should normally be consistent with core inflation rising further.

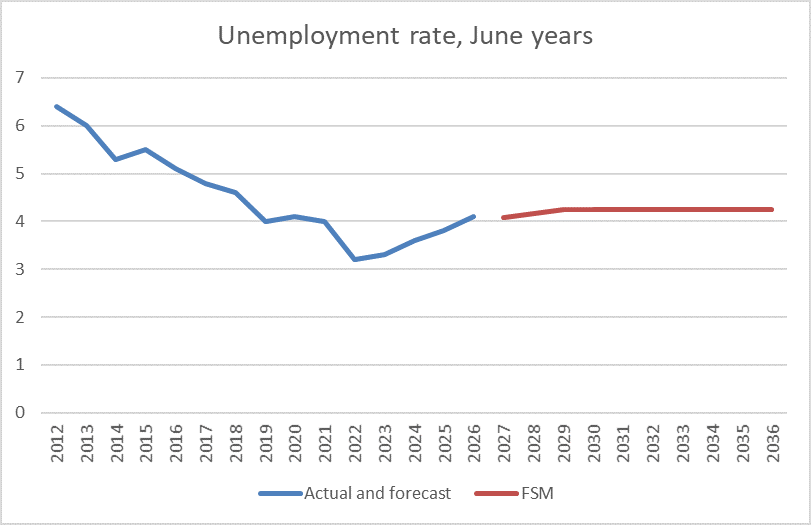

What about the labour market? The Treasury doesn’t publish an “unemployment gap” number, but comparing their unemployment rate forecasts, and the medium-term trend assumptions they use in their Fiscal Strategy Model makes very clear that they expect the unemployment rate to be below sustainable levels over the next few years.

So how is it that they expect (core) inflation to come down?

I can think of two possibilities, neither very convincing. The first is that they are still treating all the current (and forecast over the next 18 months) surge in the inflation rate – including on the core measures – as really just transitory and having nothing to do with excess demand. If so, as (eg) supply chain disruptions dissipate, what now looks like core inflation vanishes like the morning mist. But that certainly doesn’t seem to be the Reserve Bank’s view, just doesn’t square with (eg) forecast positive output gaps, and isn’t really consistent with expecting fairly rapid increases in the OCR.

The second possible story might involve inflation expectations. Perhaps they too stay firmly rooted at 2 per cent and inflation just vanishes, despite the headline pressures, despite the (on Treasury’s own estimates) overheated economy. But it doesn’t make a lot of sense, and isn’t consistent with any of the other swings or slumps we’ve seen in core inflation over the decades.

I don’t know what Treasury thinks the story is. In the end, perhaps it doesn’t matter that much. The Reserve Bank will – we presume – eventually do what needs doing and adjust the OCR to get core inflation credibly heading for the midpoint. But if there is enough inflationary pressure built up that the OCR really needs to be raised more than 200 basis points more from here, it is a little hard to believe that would be consistent with an economy still generating a positive output gap and such low unemployment rates. Medium-term forecasting is a mug’s game – no one is any good at it – so my interest is more in the logic of their model than in what the economic outturns a couple of years hence might be. But if the OCR has to be raised a lot more over the next 18 months, you might normally expect the biggest adverse economic effects (normally needed to get core inflation back down) might well be showing themselves in the second half of 2023. Which might be awkward timing for the government.

But who knows how many shocks – positive, negative, Covid and other – will be along before then.

Reblogged this on Utopia, you are standing in it!.

LikeLike